It may take some years before the US consumer becomes the driver of growth and we may see a series of recessions beforehand, but I am not betting against the US in the longer term. As Winston Churchill put it: “You can always count on Americans to do the right thing – after they’ve tried everything else”.

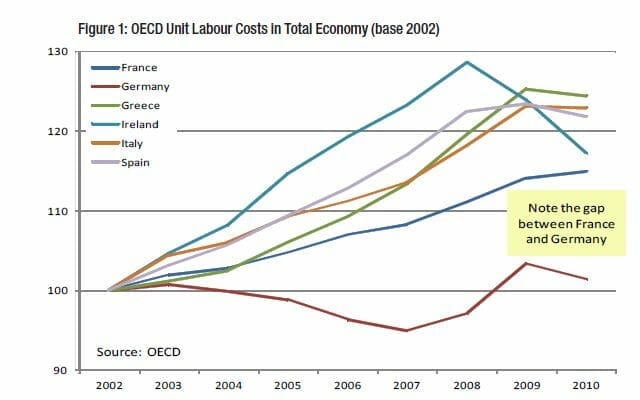

On the other hand, I find it difficult to see how many countries of the eurozone can rebound while the constraints of a single currency remain in force. The politics of the euro are so strong that it will probably be around for a while. At best, this just means that it will take that much longer before those nations are able to recover, but we could well see a more violent form of solution as citizens of PIIGS reject the austerity and loss of sovereignty that comes with staying in the euro.

China and Australia

China is one of the most significant drivers of economic prosperity for Australia. The issue with China is not its own process of deleveraging, but its reliance on exports to countries that are. Europe is China’s biggest export market. This will be a problem for China if Europe’s fortunes turn soggy.

Some people think that in a rapidly developing economy such as China’s, the key enabler is the mobilisation of capital and labour. The impact of inefficient allocation of capital (such as empty apartments) can be quickly cleared. Others believe that China will be able to engineer a soft landing as inflation is easing and looser monetary policy can be pursued.

Australia is leveraged to China’s fortunes and our own housing market continues to defy the gravity experienced by most other developed countries. These two risks are not independent and I suggest that too much Australian home-country bias may not be wise. At least the Australian dollar can act as a safety valve to make our exports more competitive and attractive.

The way forward for investors

Even if the eurozone manages to stave off default and dismemberment for a year or so, the effect would still be a downturn, although risky assets may rally with relief. In my view, this just puts off reform and adjustment.

Just because the awful is unthinkable does not make it less likely. A messy disintegration of the eurozone will see deep depressions in some countries and massive economic and social disruption that will have worldwide effects. This would be very difficult for risky assets.

Leave a Comment

You must be logged in to post a comment.