Produced in partnership with MetLife.

Whenever we talk about member service, we also need to talk about insurance engagement because that is often when members are at their most vulnerable. We’re asking them to make decisions about their future, their families and sometimes about events they don’t want to think about like illness, injury or death. That’s why, when we think about engagement, we also need to think about how we remove some of that complexity.

We all have an opportunity and a responsibility to remove complexity so that when a member comes to make an insurance claim, their level of education is better, they understand what’s in an often-complex policy, and they understand a little bit more about the role of the trustee and the insurer. This aligns with ASIC Report 760, which highlights the need to simplify communications and use research to help members make informed decisions and improve engagement.

When super fund members know insurance premiums are being deducted from their super accounts, they want to know that what they’re paying for is suitable and it’s going to add value to their life. They want guidance. And they want to know that their fund is going to be there in the moments that actually matter to them.

Many members aren’t aware that they have insurance, and then when they do know they have insurance, they don’t fully understand what it covers them for. This leads to complexity and anxiety when it comes to claim time, because at that moment they’re not at the best point in their life.

Good starting position

Super funds are already in a good starting position to deliver guidance and information to their members. MetLife surveys show that 82 per cent of members trust their super fund to give them some guidance. When they are considering insurance, they’re going to look to their fund to help them. That’s a great basis for super funds to engage with members.

To engage with them effectively, however, we need to understand why and when they reach the points in their lives when they want to make changes or need to make decisions.

MetLife research shows that when members increase their insurance, it’s often because they’ve changed jobs, they’ve got a pay rise, they’ve had an adviser tell them they should look at their insurance. Or there’s been a big life event: they’ve had a child; they’ve bought a house; they’ve got married and they’re at that next stage in their life; they’ve purchased new property; or they’ve made an active decision to change their fund.

The main reason people reduced their cover was a lack of perceived value – they weren’t sure how it contributed to their financial wellbeing or fit with their needs. When we see things like that, it means we’ve failed. We have not articulated clearly to them the value of having life insurance and how it protects them.

These are all valuable insights into how and why people make changes to their life insurance and they in turn help us identify the best times to engage them. Effective engagement is all about getting the right message to them, at the right time.

MetLife’s research identified the right moments to engage with members, those moments when they’re starting to think that they need to be more financially secure. It’s one thing to be able to send out a message, whatever channel you use, you’ve also got to get somebody to open it. You’ve got to get them to act, and it’s got to be personalised to them.

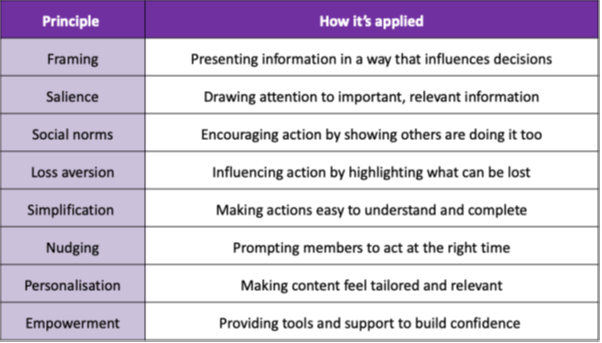

These are some of the behavioural science principles that Metlife applies to design personalised, timely communications that nudge members towards better decisions.

Framing: What is the influence of the information we present on decisions the member makes? What are we actually trying to say? What’s the key message we’re trying to get through in that in that communication?

Salience: How relevant is the information to that person, at that point in time? If we truly understand our members and we understand where they’re at in their life, how do we tailor our message so they’re likely to open it?

Social norms: How do we talk about what others are doing? As society we like to know that somebody like us is already doing something. It gives us a sense of, ‘Well, I must be on the right track’. How do we do that for them?

Loss aversion: How do we focus on what could be lost, how do we build a sense of connection and help members understand what’s at risk?

Nudging: How do we give them a little bit of a nudge to act?

Personalisation: How do we personalise it? No one likes getting emails that obviously don’t know who we are – they get deleted straight away. How do we tell members that we know who you are, and we truly care about you, and this is why we’re sending you this email?

Empowerment: How do we create tools and support to help build members’ confidence to make better decisions?

It pays off

There is a very good reason we go to all the trouble of personalising our communications, why we look for trigger points and why we care about where members are in their lives: it pays off.

We know members who engage or who have modified their insurance are more likely to stay with their super fund. All funds face the challenge of retaining existing members and attracting new ones. But someone who’s made an informed decision is more likely to stay. They’re more invested. They’ll also be more engaged with their fund.

Our research shows they’ll actually know their account balance. They will recommend their super fund to others – which is amazing – and then, ultimately, they will stay with the fund.

These are all reasons why super funds need to understand where their members are in their lives, so they can send personalised messages that are relevant and applicable.

When you behaviourally optimise your communications, you get a member who stays, who’s loyal to their fund, and actually talks about it.

We know financial security is important. What is becoming more and more important is a focus on living a longer and happier life. People now really want to be happier, and they want to be healthier for longer, and they want support from the super funds to do that. They increasingly expect you to not only look after their financial security, but they also expect you to look after their wellbeing.

This presents another opportunity for funds to engage: six in 10 employees told us that they’d be open to receiving some external advice on health and wellbeing programs. Employers are telling us they want to offer more of that to their employees. But at the moment, only about 13 per cent of members are aware of any wellness services being offered through their super fund.

Build awareness

There’s a real opportunity to improve how funds communicate and to build the awareness that this is a service that’s available. Almost two-thirds (64 per cent) of members say having access to wellness services such as mental health coaching and lifestyle programs through their super fund would make them more loyal. At MetLife, we see this as a powerful way to help funds drive loyalty and long-term engagement.

Health and wellness are untapped opportunities. We know members are placing more value on them and they are looking for somebody to reach out to them. There is an opportunity to look at how you improve member engagement by adding value through lifestyle and wellbeing services. It’s another touch point with a member to remind them why it’s great to be with you as a fund, but it needs to be targeted. It’s not a one-size-fits-all proposition. Once again, it’s about understanding your members, understanding how you can behaviourally optimise the communications you send them and thinking about what message you actually want them to walk away with.

And finally, make sure your activity leads to a desired outcome. Understand what you’re trying to achieve when you send out any communication or any engagement to your members. It’s on us to create personalised content and to win the attention of members. It’s not their job to try to decipher what we’re trying to tell them.

We need to help members confidently and actively decide what is right for them and their loved ones. We need to make the journey easy and simple. We need to remove the complexity and make it simple enough so that somebody doesn’t have to come back to us multiple times because they don’t understand.

When we think about engaging members, we need to think about it in the context of other communication and experiences they have in their lives. We’re not just engaging them as their super fund; we’re competing with everything else they get from every other service provider they have. We all joke about Netflix or Amazon, but that’s exactly what we’re being compared to.

This article is adapted from a presentation by Lina Saliba to the Investment Magazine Insurance In Super Summit in Sydney on 22 July.

Leave a Comment

You must be logged in to post a comment.