Parts of the superannuation industry are pushing for “retirement defaults” to be placed on the policy agenda. This raises the question of what “default” might mean in a retirement context, and relatedly, which version the industry may be angling for. We address these issues in a new report. We also argue that there is a meaningful group of retirees who could benefit from enabling fund trustees to suggest to them what might be described as a “default retirement solution”.

The word “default” is used to describe different things in a retirement context. It may refer to true (“hard”) defaults where a member is assigned to a solution without taking action through to “pre-set” solutions that are made available to members via various channels. Also, “default” is sometimes used as a noun, that is, a “default” solution; and (less frequently) as a verb, that is, the action of “defaulting” a member into a solution.

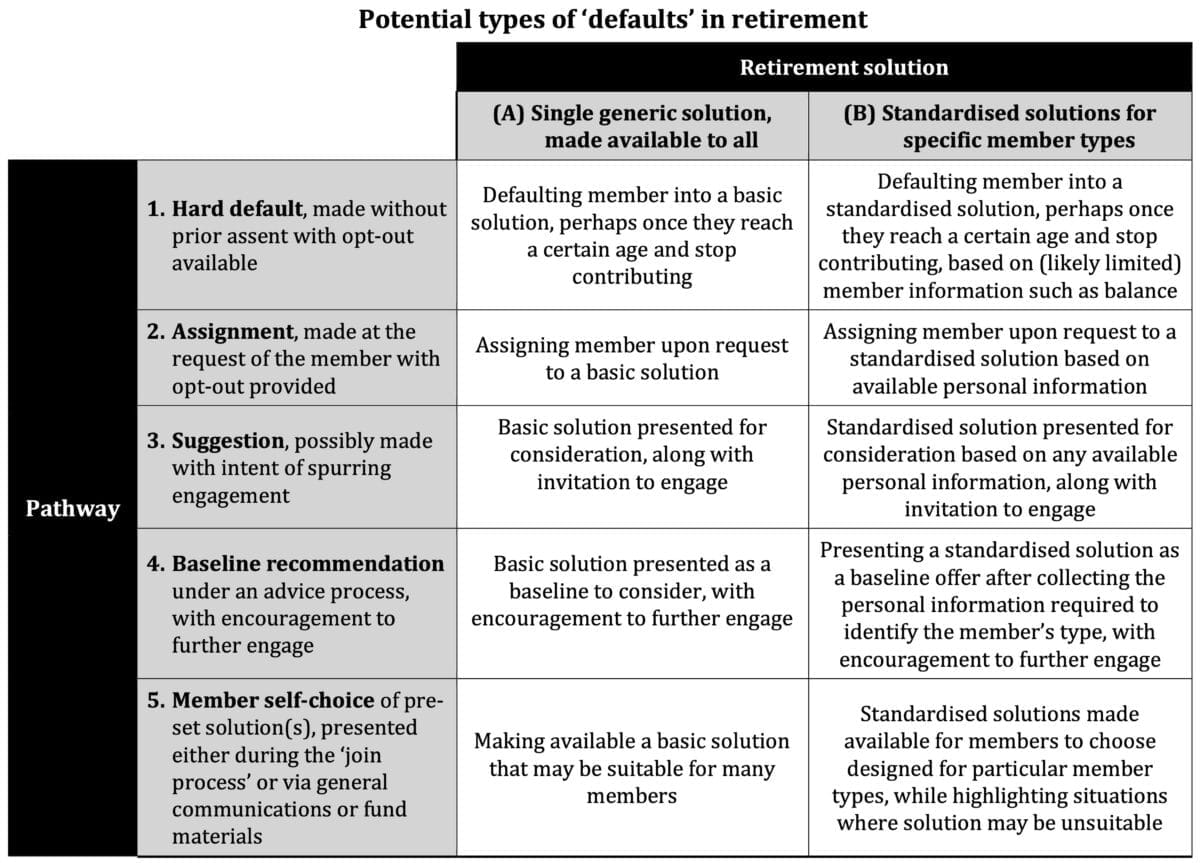

To provide some structure, we offer the framework summarised in the figure below to describe mechanisms that might be called a “default” across two dimensions. The first is the type of retirement solution that is made available as a default, which could be either a single, generic solution or a set of standardised solutions designed for specific member types.

The second dimension is the pathway through which members may end up in those solutions. We identify five pathways, including hard default without assent, assigning the member upon their request, suggesting a solution to the member, providing a (baseline) recommendation through a financial advice process, and the member choosing a default solution for themselves from a menu of options.

Along the retirement solution dimension, it is open to super funds to make available any type of solution they can design. However, the pathways dimension is constrained under the current policy framework. Specifically, hard defaults, assignment and suggestions are unavailable.

Meanwhile, super funds conceptually have scope to recommend a default retirement solution under an advice process, which in turn may be further enabled under the Advice through Superannuation component of the Delivering Better Financial Outcomes (DBFO) Tranche 2 reforms. It is also open for super funds to make available default retirement solutions that members may choose for themselves.

The issue is that both of these available pathways rely on members to engage with the decision process. The risk is that many members may fail to do so.

Problem that needs to be solved

Many members either take no action or accept the most obvious option upon entering retirement, which may leave them well short of making best use of their retirement savings. More disengaged members may inadvertently remain in an accumulation account despite being retired. And those transferring into the retirement phase often end up investing through an account-based pension (ABP) using the default investment strategy and drawing at the minimum rate, with insufficient regard for suitability.

The challenge is to assist these members towards a retirement solution that is more appropriate for their needs, when some are either unlikely to take action or have difficulty engaging effectively with available help, guidance and advice services. Introducing “retirement defaults” in some form offers potential to help these members through presenting them with a ready-made solution and making their decision easy.

Enabling ‘suggestions’ as the key policy action

The key policy action would be enabling super funds trustees to suggest a potential retirement solution to members as a type of nudge or a call to action (that is, Pathway 3). This is our interpretation of what some in the super industry are calling for, sometimes under the heading of “soft default” or “first offer”.

Enabling trustees to suggest retirement solutions to members outside of a financial advice process would require addressing the current constraints stemming from the anti-hawking regulations and the proposed limitation on referring to financial products under the targeted superannuation prompts component of the DBFO Tranche 2 reforms.

There are various issues with allowing trustees to suggest a solution. Nevertheless, we consider the benefit of moving many retirees into more appropriate solutions than otherwise significantly outweighs the risk of a few retirees ending up in less suitable solutions, especially if policy design considers appropriate member protections.

Other important elements

We see three elements as fundamental to delivering retirement defaults in an effective manner:

- Defaults should be “smarter” rather than basic – The industry should be aspiring to deliver “smarter” defaults that cater for differing member needs, for instance a suite of solutions designed for specific member types. Super funds can do better than single generic defaults. In particular, presenting an ABP with minimum drawdowns as the default would provide little uplift from the current state.

- Implementing for members – Super funds need to establish the capacity to deliver integrated default solutions, and then only require members to push a proverbial “big green button” to have a solution implemented for them. Currently the industry at large is not in the position to do so, which raises the spectre of implementation losses that dilute the benefit from defaults if not addressed.

- Provide member protections – Default retirement solutions and the manner in which they are offered should be carefully designed and framed to limit the risk of members ending up in a solution that is unsuitable for their needs. We suggest some procedures in our report.

Policymakers should give the matter close consideration

Current industry settings place too much reliance on members taking the initiative. A significant group will not, and end up either stuck in accumulation or allocating to a quite sub-optional retirement solution.

We need to make it as easy as possible for members who have difficulty engaging to move into an acceptable (even if not optimal) retirement solution. Enabling trustees to suggest what might be called a default retirement solution, if done well, can help this happen.

David Bell is executive director of The Conexus Institute.

Geoff Warren is research fellow at The Conexus Institute.

The Conexus Institute is a not-for-profit think-tank philanthropically funded by Conexus Financial, publisher of Retirement Magazine.

Leave a Comment

You must be logged in to post a comment.