This article originally appeared in the print edition of Retirement Magazine Vol. 2

Australia has developed a comprehensive and well-respected superannuation system with a mandatory contribution rate of 12 per cent and good long-term investment returns. This system has the potential to deliver adequate and sustainable retirement incomes, together with the means-tested Age Pension, to millions of Australian retirees for decades to come.

But the system is not yet delivering that outcome. One of the reasons is our traditional love for the lump sum benefit, which began with favourable tax rates many decades ago.

Let’s recall that the legislated objective of superannuation is “to preserve savings to deliver income for a dignified retirement, alongside government support, in an equitable and sustainable way.

Note that the primary purpose of superannuation is the provision of income during the retirement years. It is not there to build a nest egg or for estate planning. It is to provide money for retirees to spend during their later years. The retirement phase can work much better than it is.

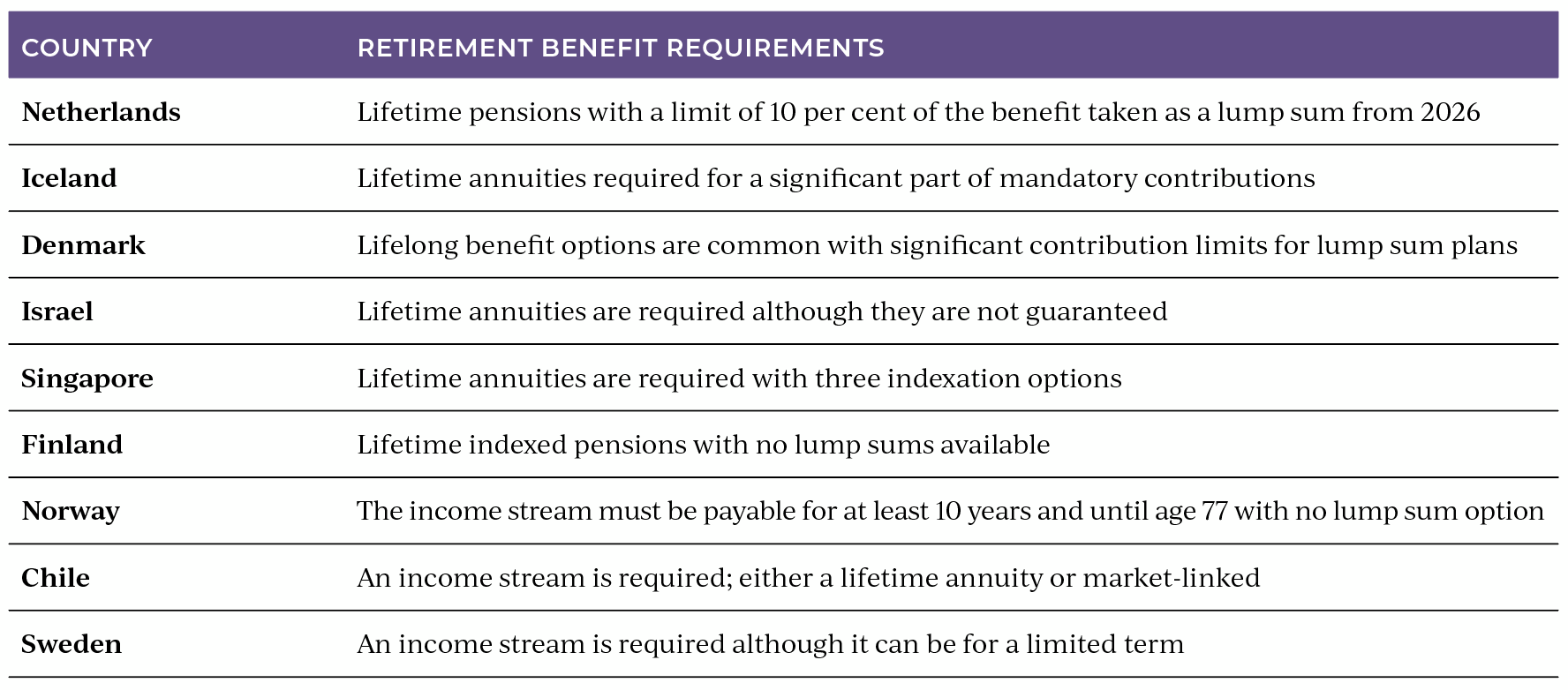

An international comparison

The 2024 Mercer CFA Institute Global Pension Index compared and ranked 48 pension systems around the world by considering the adequacy of the benefits provided, the long-term sustainability and the overall integrity of each system. Australia ranked seventh – a creditable outcome, but with room for improvement. The accompanying table shows the requirements in each of the other top 10 systems (in order of their ranking) in respect of the benefits that are required to be provided at retirement.

The comparison with the Australian system is stark. We have no requirements at all. Australian retirees can take all their superannuation money out at retirement and spend it immediately, pay off debt, give it away (perhaps operating as the Bank of Mum and Dad) or invest it elsewhere. Alternatively, they can leave it in their superannuation accumulation account, where it will be subject to a higher tax rate than in a tax-exempt pension account, but with no drawdown or income requirements.

It is also worth noting that many retired Australians make no decisions at all, due to several factors including inertia, lack of understanding, communication and language difficulties and the overall complexity of moving into a pension product. It can become even more complicated if the individual returns to the workforce or wishes to make a downsizer contribution.

The accumulation phase of our superannuation system is very simple for those who don’t want to make a decision. The MySuper default arrangements work well and do not require individuals to engage with their super fund. It just happens.

However, that does not happen at retirement. Indeed, as of March 2025, there are more than 840,000 MySuper accounts for Australians aged 65 and over with an average balance of $111,000. Some of these individuals may still be in the workforce but most of them have retired.

Many of these MySuper members will have had very little, if any, engagement with their superannuation. It has all happened automatically and that is a good outcome. However, at retirement, that automatic process stops and individuals must take action. The result is that many retirees are not a receiving an income from their superannuation account which could make a significant difference to their standard of living and help provide them with a dignified retirement.

Australia has a very good accumulation system for retirement, but we do not have a retirement income system. We must do better.

Three recommendations for change

- Introducing a soft default

Most retirees need help moving from the accumulation phase to the pension phase. This particularly applies to many MySuper members. Let’s make it easy for them with a nudge, offering them a default pension product on an opt-out basis.

Initially, this nudge would only be available to MySuper members aged 65 and over (thereby meeting one of the conditions of release) and where there have been no contributions received for the last three or six months. In other words, it is very likely that the individual has retired.

The suggested default product would be an account-based pension with a similar investment strategy to the MySuper product, although it would now be tax exempt. Unlike the existing account-based pension application forms, the individual would not be asked to select a drawdown approach. The default would use the minimum drawdown rates.

Of course, bank account details would be required and the ATO would check if the retiree has breached their transfer balance cap. However, this process would be much simpler than relying on the individual to transfer their superannuation into a new pension product.

I am recommending that we begin introducing this default pension product to MySuper members as there is a higher level of disengagement here. If it is successful, this approach could be broadened to Choice members.

The design of a default pension product can be debated, but to begin this important policy development I am suggesting the use of an account-based pension, as it does not restrict future decisions that the retiree may wish to make. This is unlike a longevity product which may limit future options.

As this development would not affect current retirees but would require some information from each new pensioner, there is no reason why it could not be introduced immediately, with appropriate legislative support.

- Compulsory income streams

A more significant change would be to require future retirees to transfer at least half their retirement benefit into an income stream product. Such a requirement would not be as restrictive as the other leading pension systems around the world as half the benefit could still be taken as a lump sum, either at retirement or gradually drawn down during the retirement years.

Of course, the big question is the definition of an “approved” income stream. It is suggested that the following products should be approved:

- A lifetime annuity from a life insurance company.

- A pension from a defined benefit scheme.

- A pooled longevity product.

- An annuity for a fixed term where the term is at least 15 years, guaranteed or market linked.

- A “restricted” account-based pension where the annual drawdown is between the current minimum rates and double these rates.

As this reform would be significant, it is suggested that the commencing date should be three to five years after the initial announcement. This would enable individuals approaching retirement to adjust their retirement plans as may be necessary. As it would only affect future retirees, current retirees would not be affected.

The long-term impact of this development is likely to change Australians’ view of superannuation. That is, superannuation will deliver a future income stream, consistent with its legislated objective. It is not a just a nest egg!

One variation that is worthy of consideration is to exclude an amount (say $50,000) from this income requirement and permit retirees to keep this component as a financial buffer in their superannuation fund which will in turn provide them with greater confidence to spend the income they are receiving.

- Income must start from age 75

As noted earlier, the Australian superannuation system does not have any requirement to withdraw funds following one’s retirement. The existing transfer balance cap of $2 million encourages individuals to transfer their accumulated funds below this figure into a tax-exempt pension product. However, balances above this amount remain subject to tax in the accumulation account, although they can be drawn down at the request of the individual. In many cases this does not occur, as the funds remain in a concessionally taxed environment.

“It is therefore recommended that, from age 75, individuals must withdraw funds from the accumulation account using at least the minimum drawdown rates that apply to account-based pensions.”

It is therefore recommended that, from age 75, individuals must withdraw funds from the accumulation account using at least the minimum drawdown rates that apply to account-based pensions.

Such a requirement is common around the world. For example, in the US, there are required minimum distributions from age 73 in retirement plan accounts (such as those in 401(k) plans and IRAs). This approach means that the accumulated funds are used to provide retirement income and would also limit the growth of superannuation balances during retirement.

Fundamental need for change

There is much to be proud of in the Australian superannuation system. However, we have not developed appropriate policies that deliver sustainable retirement income to future retirees. There is a fundamental need to develop a stronger income-focused framework so that the Australian community, as well as the government and the super industry, appreciate that the primary purpose of superannuation is to provide regular and sustainable retirement income.

These three recommendations would, over time, change our society’s perspective of superannuation and highlight its fundamental purpose. It is likely this income focus would lead to further developments, including more flexible income products, recognising that some retirees return to the workforce in a different role and the possibility of a single superannuation product that includes both the accumulation and pension phases.

However, these innovations can wait. The most important step is to strengthen our focus on retirement income.

Dr David Knox was a senior partner at Mercer and national leader for research and policy until retiring in 2025. He was lead author of the Mercer CFA Institute Global Pension Index for 16 years. David was an APRA board member (1998–2003), president of the Actuaries Institute in 2000, and was appointed a Member of the Order of Australia in 2023.

Leave a Comment

You must be logged in to post a comment.