This article originally appeared in the print edition of Retirement Magazine Vol 2.

After an overnight flight from Phuket followed by a much-delayed Qantas flight from Sydney to Canberra – because, of all things, the pilot found his seat to be uncomfortable – I found myself jammed in with the rest of the friends of Conexus at the back of Members Dining Room 2 in Old Parliament House for the Retirement Leaders Summit.

I was delighted to be there, partly because it was a conference where I didn’t have to talk, so there wasn’t 10 hours of preparation, so I could just listen – and I wanted to hear what people had to say.

If I am known for anything in superannuation, it’s standing for the idea the whole purpose of the system is to give Australians the best possible retirement – the third and arguably unfinished pillar of Australia’s mostly magnificent system. That’s it. That’s the explicit promise it makes, and this promise is pretty unevenly delivered.

Delivering that promise means the system must be run cost-effectively; that investment returns must be market leading; and then members’ retirement must be the best it can possibly be.

I don’t say the promise is to make members rich or happy. That’s not what super does. It can’t be. It can, however, help them do the best with what they have.

The chart which explains this best is from the Conexus/CoreData Best Possible Retirement Research, which looks at how Australians feel in the decade before they retire, and in the decade after.

This research uses member data to create a hierarchy of member outcomes and experiences, and it means many funds are forced for the first time to confront the fact of how they rank relative to everyone else.

There’s are all sorts of messages in this data. Many funds, despite three years of focus, haven’t improved their members’ retirement experiences, while others quite clearly have. Close enough to one in five (17 per cent) members are considering changing fund at retirement. The lump sums being withdrawn at retirement are increasingly being gambled (invested in crypto and gold). Service experiences continue to show massive variance. Australians are really worried about inflation but super funds, by and large, aren’t reflecting this concern.

From pretty good to really pretty bad

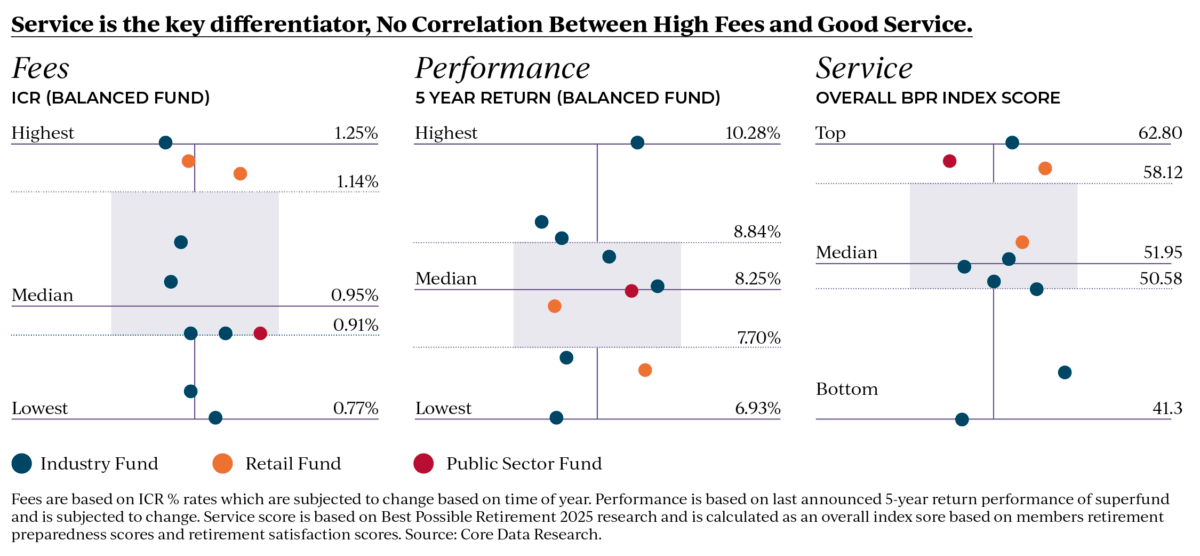

It’s pretty easy to see that competition and the government have ensured that the costs of superannuation fall in a very narrow range, and that the introduction of the Your Future Your Super performance test means returns also fall in a very narrow range. But the retirement experience data shows us the confidence, satisfaction and service indicators remain very wide, ranging from pretty good to really pretty bad.

You might expect the funds with the poorest service scores would also be the cheapest or the smallest funds – that service would be, in effect, a function of price. It turns out not to be true: price has no correlation with service, while size is inversely correlated.

In other words, smaller funds are simply better at delivering a good retirement experience. While they don’t form part of the survey, because their independent member cohort is too small, the best member experience year-on-year is NESS, the electrical contractors super scheme.

At just over $1 billion in assets and just under 13,000 members, NESS is technically tiny, and it has only just launched an app. Before that it solved all its member communication issues by in-person site visits, good phone service and clear messaging. It’s going to be interesting to see if an app shifts the dial for them, because it’s clear that what the members value the most is expert service on the phone and good workplace engagement.

You might argue that a fund that size should be rolled up, shuffled into a similar fund like Equip or Cbus, but why? If performance is good, insurance is good and service is good, it’s hard to argue that increased scale will result in better member service and outcomes.

So there I was at the Retirement Leaders Summit, jammed into the cheap seats and listening to ASIC and APRA. They were as usual, measured and intelligent and thoughtful; and, for the third year in a row, also clear: get retirement right; we are watching and we are looking for improvement. Funds responded: we are taking this seriously; we are leaning into it. And service providers said the same thing: this is the first thing on our minds.

A thumbnail dipped in tar

I started to do some maths to figure out, in a thumbnail-dipped-in-tar kind of way, the size of the retirement problem, just in case anyone asked. On a simple, five-year view, between now and this time in 2030 there will be around 1300 working days. The Australian Bureau of Statistics suggests that between 700,000 and one million Australians will retire. The data also suggests that the average age of retirement is close enough to 65, and that the modal age of death for men is 85 and for women 91, which gives us 20-odd years of retirement. And retirement will range from easy to complex.

So: 1300 days of seven effective working hours gives us 9100 working hours; and a mid-range estimate of 900,000 people retiring. This gives us 98 people retiring from work every hour of every working day for the next five years.

Play with those numbers any way you like – model out people working longer, or fewer people retiring – but whichever way you cut it, the numbers are daunting.

Daunting, too, is the fact that retirement is complicated beyond measure for most. Our research shows that only about 20 per cent of people retire at the time and in the way they choose, and therefore with confidence.

The trustees of every fund should be explicitly asking themselves and their executives: are we as a fund ready for this? Have we have built the services? Do we have the models that allow us to predict what our members’ experiences will be? Do we have a system of advice or soft compulsion to make this simple? And can we do it at scale?

If the answer to any or all of those things is no, then the size of the problem and the scale of the disappointment is easy to calculate – and really, really sobering.

Andrew Inwood is the founder and global chief executive officer of CoreData Group.

Leave a Comment

You must be logged in to post a comment.