This article originally appeared in the print edition of Retirement Magazine Vol. 2.

We see a sizeable chance that it might take 10 years after the introduction of the Retirement Income Covenant (RIC) for the vast majority of super funds to put in place high-quality retirement income strategies (RIS).

Avoiding such an outcome requires ongoing focus by all parts of the retirement system, including the industry, policymakers and regulators. In this article, we outline what progress has been made, and explore what could spur the industry on.

We start by viewing the current state through the lens of three parts of the retirement ecosystem: industry, policymakers and regulators.

Through the industry lens

While many funds have advanced their RIS, progress has been patchy, with some funds leading and others lagging. Overall, there remains much to be done. These views are shared by the regulators. APRA deputy chair Margaret Cole observed that “a substantial gap remains between where the industry is today and where it needs to be”. Meanwhile ASIC Commissioner Simone Constant acknowledged that “while we are seeing some green shoots, it’s clear there are leaders and laggards”. Constant’s urgency reflects our own concerns: We can’t wait years to get this right. Each year, more than 100,000 Australians retire.

There have been some exciting product initiatives, such as innovative lifetime income streams offered in the accumulation phase, and provision of persona-based solutions. Positive developments are also taking place in advice and guidance, particularly in the area of hybrid offerings with a digital foundation.

However, few funds offer integrated retirement solutions combining investments, lifetime income streams and a drawdown plan tailored for a range of member needs. And no fund can offer integrated solutions plus straight-through implementation. Some leading funds are hopeful of doing so soon, but others have said that this remains a distant aspiration.

A few hurdles seem to be preventing large parts of the industry moving forward, including the state of operational infrastructure and lack of regulatory clarity coupled with heightened regulatory risk aversion by some funds. Some funds appear to be lacking strong business incentives to really embrace retirement.

Through the policymaker lens

Since the RIC was introduced, two areas of policy focus by government stand out. The first is retirement policy, which has steadily developed in a coordinated fashion. The Retirement phase of superannuation (note 1) consultation of December 2023 led into the initiation of four retirement reforms in November 2024 (note 2):

- Revamp the existing innovative income stream regulations

- Expand resources on the Moneysmart website

- Introduce a set of voluntary best practice principles (BPP) to work in conjunction with the RIC

- Implement a new transparency framework, named the Retirement Reporting Framework (RRF), to commence from 2027

The BPP is shaping up to be a positive driver to uplift the retirement offerings by super funds. Although voluntary, we are hopeful that it will be embraced as a de facto industry standard. The RRF has potential to reinforce the BPP through measuring and publicly reporting progress. We feel the RRF could become more effective by basing the reporting requirements on data that funds should be collecting to monitor their RIS progress rather than what is currently available.

Advancements in financial advice reform have moved more slowly.

The stated aims of Tranche 2 of the DBFO (Note 3) reforms have not yet been achieved, with the government running into issues around complexity, resourcing and time constraints (the federal election). The draft legislation of March 2025 (note 4) covers advice through super and targeted superannuation prompts but has not been tabled. The “new class of adviser” (NCA) remains a significant gap to address and appears to be in a holding pattern.

We view the advice through super provisions as very constructive. They set out the scope of advice that super fund trustees may provide on retirement, restricting that advice to the member’s interest in the fund while accounting for the key personal information required to recommend retirement solutions that are likely to be suitable.

The targeted prompt provisions detail a framework for “activity nudges”, but their effectiveness may be limited by the prohibition on referring to specific products, which may leave members at sea and rules out nudging members through “first offers” or soft defaults.

Through the regulator lens

A highlight of the regulatory focus on retirement has been the close collaboration between APRA and ASIC, having undertaken together a Joint Thematic Review (note 5) and a “pulse check” on RIC implementation (note 6) with another iteration forthcoming. These initiatives involve surveying funds and presenting examples of better practice back to the industry. The regulators are supporting the principles-based RIC while restraining from directing funds in what they need to do. They have been vocal in calling out what they consider to be “not good enough”, but reluctant to specify what good looks like.

APRA implemented updates to Superannuation Prudential Standard SPS 515: Strategic Planning and Member Outcomes that incorporated the requirement to support the implementation of the RIC, which took effect from 1 July 2025. ASIC has flagged its forthcoming first retirement report focusing on communications by trustees to members on the topic of retirement.

Can we be confident or bearish over avoiding the 10-year scenario?

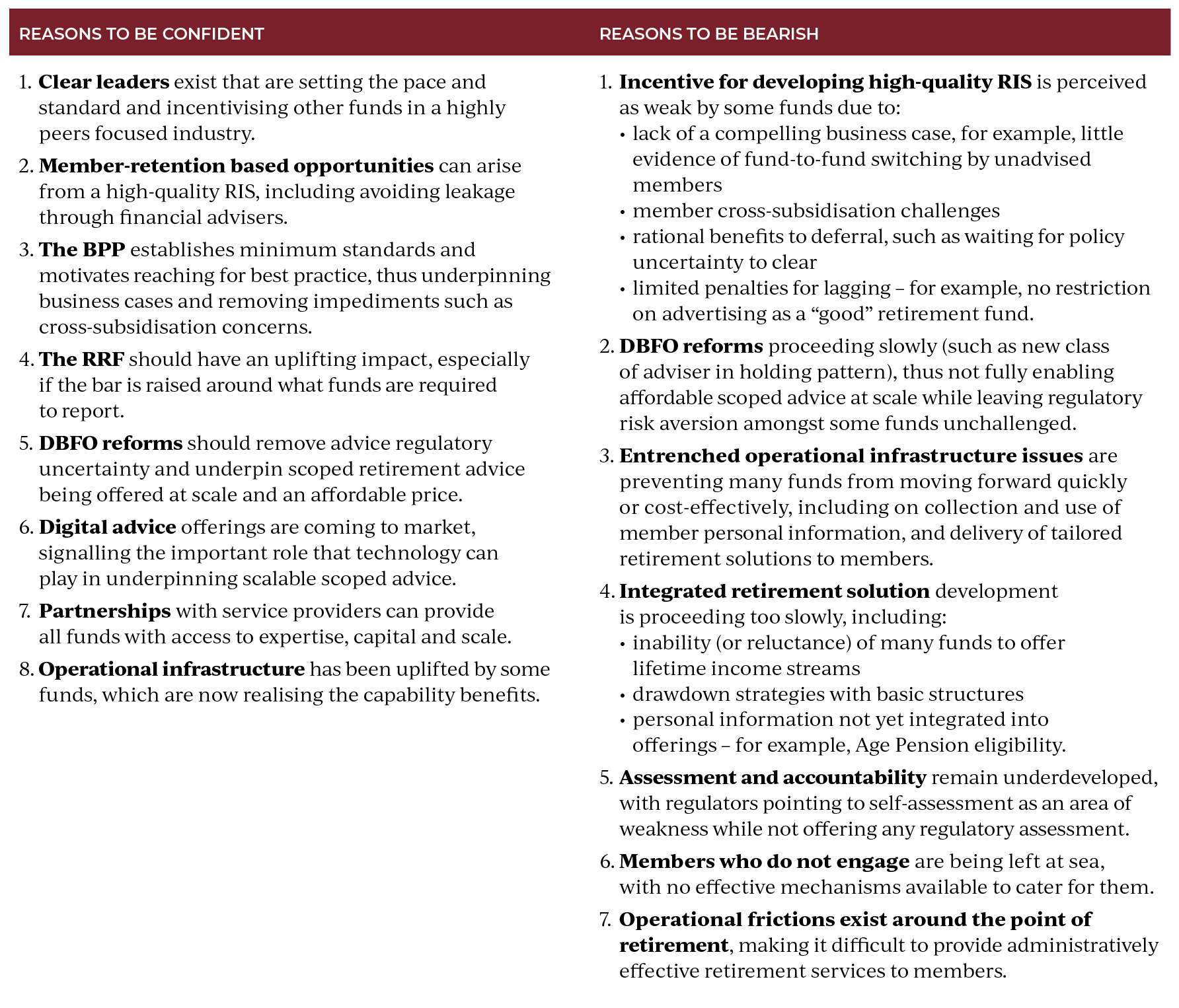

Reasons to be confident or bearish over avoiding a scenario where it takes 10 years to deliver quality RIS are listed in the table below. The reasons to be bearish seem weightier, but a case could be made either way.

Spurring the industry forward

Four developments offer the potential to move the industry forward at faster pace, thus tilting the balance towards the “confident” case:

- Clarity around what “good” looks like – The principles-based RIC requires trustees to have in place an RIS but issues no guidance around what constitutes a satisfactory let alone high-quality RIS. The BPP is a good start, but the need remains to connect principles to practice. Further guidance around the capabilities (note 7) required to deliver a quality RIS, perhaps written into regulatory standards or guidance or as the basis of assessment, would help clarify what “good” looks like. Doing so would establish baseline standards, provide an indication of good practice, inform business planning and ultimately spur funds to get moving.

- Assessment and consequences – An assessment regime coupled with consequences for falling short would be a strong motivator for development of acceptable RIS across the industry. We do not believe either competition, regulatory jawboning or voluntary principles can be relied upon. Laggard funds need stronger incentives and their members need protecting. Development of regulatory assessment and associated consequences is a task for policymakers and regulators.

- Further financial advice reforms – The stated objectives of DBFO need to be implemented to remove regulatory uncertainty from the more risk-averse funds while enabling cost-effective implementation of scalable affordable scoped retirement advice offerings. DBFO Tranche 2 provisions on advice through super need to be legislated and the framework for NCAs resolved. Ideally targeted prompts might be reframed to enable product nudges or “soft defaults”.

- Super funds need to prioritise delivering on retirement – Many funds do not appear to have made a priority of delivering a high-quality RIS as soon as practical. Retirement needs to be a top-two priority at board level and be afforded resources and senior executive ownership. Some of the leaders are starting to demonstrate what can be achieved once this becomes the case. The industry at large needs to get on board.

All system participants have a role to play

We feel the retirement system is at an important inflection point. It may reach a good level in good time. Or it may not.

We are all accountable if we ultimately find the system fails to deliver quality retirement outcomes for members 10 years after the RIC came into effect. There is an important role for each part of the system.

Our list of “tasks to do” appears here. Our plea to all participants is to put your shoulder to the wheel and help avoid the retirement system taking 10 years to reach where it needs to be. Members deserve no less.

‘Tasks to do’ to ensure delivery of quality RIS doesn’t take 10 years

Tasks for policymakers

- Maximise potential of BPP (within sight) and RRF (bar needs to be raised)

- Accelerate DBFO through legislating Tranche 2 and addressing NCA

- Explore ideas such as soft defaults (i.e. restrictions under targeted prompts and anti-hawking) and contributory pension accounts

- Explore a ‘plan B’ for moving the industry forward, potentially including:

- Stronger incentives

- Assessment frameworks and consequences

- Licensing regime

- Government-led solutions and services as a fallback if the industry continues to lag

Tasks for regulators

- Develop regulatory assessment with consequence to address laggards and raise standards

- Uplift regulatory standards to better incorporate retirement

- Consider how to resolve situations where a fund’s RIS only serves limited member types, e.g. equivalent mechanism to the DDO; funds moving on members they cannot serve

- Provide strident regulatory feedback or action where appropriate, e.g. funds whose three-year plan won’t see them meeting Treasury’s BPP

Tasks for super funds

- Commit by making retirement a top two priority, backed by adequate resources and ownership at the most senior executive level

- Break down any regulatory risk aversion around advice provision (be braver!)

- Focus on the two “i’s” of integration and implementation as guiding aspirations

- Simplify for members wherever possible, thinking at an industry level and collaborating

- Engage with policymakers, making consistent and coherent requests: ‘soft defaults’ and contributory retirement accounts may make good test cases

- Improve self-assessment practices

- Some funds could uplift their understanding of the benefits of LIS for members.

Dr David Bell is executive director of the Conexus Institute.

Dr Geoff Warren is Research Fellow at the Conexus Institute.

The Conexus Institute is a not-for-profit think-tank philanthropically founded by Conexus Financial, publisher of Retirement Magazine.

Notes:

1. Treasury consultation, “Superannuation in Retirement” – https://treasury.gov.au/consultation/c2023-441613

2. Treasurer Jim Chalmers media release, “Improving the retirement phase of superannuation”, media release – https://ministers.treasury.gov.au/ministers/jim-chalmers-2022/media-releases/improving-retirement-phase-superannuation

3. Treasury, “Ensuring access to quality and affordable financial advice” – https://treasury.gov.au/sites/default/files/2024-12/p2024-607305.pdf

4. Treasury, “Improving access to affordable and quality financial advice”, consultation – https://treasury.gov.au/consultation/c2025-637814

5. APRA, ASIC: “Information report: Implementation of the retirement income covenant: Findings from the APRA and ASIC thematic review, July 2023 – https://www.apra.gov.au/sites/default/files/2023-07/Information%20report%20-%20Implementation%20of%20the%20retirement%20income%20covenant-Findings%20from%20the%20APRA%20and%20ASIC%20thematic%20review%20July%202023_0.pdf

6. APRA, “Industry update – Pulse check on retirement income covenant implementation”, July 2024 – https://www.apra.gov.au/industry-update-pulse-check-on-retirement-income-covenant-implementation

7. We discuss capabilities assessment in “Evaluating Retirement Income Strategies through a capability-based framework”, 11 August 2025 – https://theconexusinstitute.org.au/wp-content/uploads/2025/08/Conexus-Institute_RIS-capabilities_August-2025.pdf

Leave a Comment

You must be logged in to post a comment.