Produced in partnership with BNY

A boom in private credit in Asia continues to attract asset owners looking for consistent yield in a volatile geopolitical environment. Despite economic upheaval and increased regulatory scrutiny, asset owners see growing investment opportunities in private credit, particularly in the Asia-Pacific region.

Raymond Chan, managing director and head of APAC Credit at CPP Investments, one of the world’s largest investors in private equity, told the Fiduciary Investors Symposium in Singapore in March that the fund increased its commitment to Asian credit in the 2024–25 financial year.

“The interest rate increase is creating a lot of opportunity for credit investors in Asia, as many international funds have shifted focus back toward developed markets,” Chan said.

Allocation trends among funds

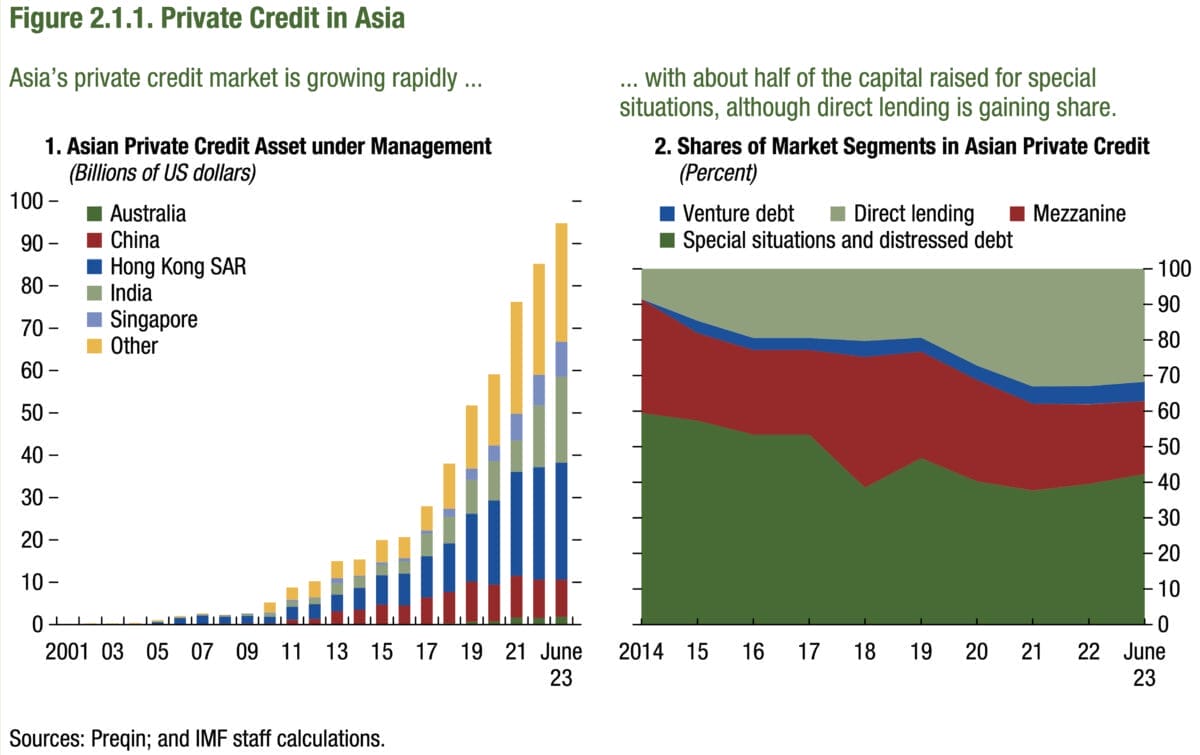

Despite changes to economic policy around the world and the resulting impact on the market climate, the rise of private credit shows no signs of slowing. Global private credit assets under management quadrupled to US$2.1 trillion in the ten years through 2023, according to the International Monetary Fund. The sector boomed in the wake of the 2008 Global Financial Crisis as stricter regulation forced many U.S. banks to abandon some lending markets.

“A number of the larger pension funds across the Asia-Pacific region that are state-owned or government-backed have been actively pushing their regulatory bodies to allow them to increase their allocation to private credit.” – Rob Youkee, BNY.

“It’s in vogue,” says Rob Youkee, director of client executive for asset servicing at BNY. “A number of the larger pension funds across the Asia-Pacific region that are state-owned or government-backed have been actively pushing their regulatory bodies to allow them to increase their allocation to private credit,” said Youkee.

Previously, private credit allocations averaged about 4 to 5 per cent of the roughly 10 per cent typically reserved for unlisted assets. Over the past 18 months, those allocations have climbed to 7 to 10 per cent.

Australian super funds also continue to back this asset class. Just over a quarter (27 per cent) of asset owners surveyed at the recent Fiduciary Investors Symposium said they planned to increase their allocations to private credit. Only 3 per cent said they planned to decrease their allocations (though many planned to maintain or rotate their mix).

Market dynamics and competition

The $330 billion Australian Retirement Trust (ART) is one fund that intends to decrease its private credit allocation, in its high-growth default investment option. It had boosted its allocation to this asset class in recent years, but recently announced plans to trim its exposure by 50 basis points to 2.5 per cent as part of its default high-growth strategy, as competition for assets grows.

Andrew Fisher, ART general manager of total portfolio management and resilience, told the FIS event that the move is “partly a rotation to where we want to be, and partly because we’re also being crowded out”.

“We think of things through the lens of capital competition, where mid-risk assets increasingly vie for attention,” he said

“To an extent, it’s been crowded out a little by infrastructure and real estate cyclically becoming more attractive. So, if you think back to when private credit looked really, really attractive a few years ago, rates were low and yields were really attractive. [It was] the golden age of private credit, but that’s in the rearview mirror now, and the opportunity set for us at least looks a little more attractive in real assets.”

North America still accounts for about three-quarters of the market, although private credit markets in China, India, and Indonesia are emerging, and South Korea has grown steadily. Private credit funds across Asia tend to focus on acquisition financing, asset-light businesses, and distressed debt, providing financing to the high-yield segment.

Innovation and regulatory scrutiny

The private credit sector’s continued growth has attracted more regulatory scrutiny around the world. Last year, the International Monetary Fund (IMF) raised concerns about the sector’s opaque nature, infrequent valuations, difficult-to-assess credit quality and overall systemic risk.

However, the sector’s growth is also spurring innovation that may enhance liquidity, efficiency and transparency.

“I’m seeing trials involving distributed ledger technology within private credit that isn’t there on real estate because that’s physical property, or private equity because of the maturity of that market and its transaction life cycle. It increases risk because you’re more reliant on technology, but these developments inherently make the asset class more transparent,” says Youkee

“We are seeing an uptick in the use of smart contracts, which improve the efficiency of trading in the asset class, effectively promoting the dematerialisation process. In this context, it’s no different from the transformation of fixed income more than 20 years ago, when paper-driven processes gave way to digital trading.

“The upside for private markets and private credit, in particular, is digitisation, which helps reduce transaction costs, potentially passing savings back to investors as higher returns, and increase transparency through near real-time settlement” – Rob Youkee, BNY.

“The upside for private markets and private credit, in particular, is digitisation, which helps reduce transaction costs, potentially passing savings back to investors as higher returns, and increase transparency through near real-time settlement. Shared ledgers are one of the technologies currently being explored.”

S&P recently estimated that about US$500 million in private credit assets are currently tokenised. While this is a very small sub-sector, it’s growing fast. Improved transparency and data about underlying private credit holdings remain essential for investors.

The role of platforms and data

To meet these transparency demands, Youkee says firms such as BNY are developing comprehensive platform solutions. Anchored by integrated administration, custody, accounting, and analytics capabilities, these platforms deliver deeper visibility into private credit performance and holdings, giving asset owners the data they need for better-informed decision-making.

“Leveraging BNY’s advanced technology platform and data analytics expertise, we empower asset owners with actionable insights and robust analytics, enabling more informed decision-making and optimised portfolio management,” Youkee says.

“Integrated solutions are designed to support clients throughout the investment lifecycle, driving greater operational efficiency, risk mitigation, and real-time performance returns – a roll-forward net asset value using a public equity benchmark or the investor’s own benchmark.”

As private credit in Asia matures, asset owners face both significant opportunities and heightened risks. The asset class continues to attract capital, but competition, regulatory oversight, and the need for greater transparency will shape its next phase. With digitisation, smarter allocation strategies, and robust data platforms, investors can navigate this evolving landscape more effectively.

Click here to learn more about BNY’s integrated private credit solutions.

Leave a Comment

You must be logged in to post a comment.