After playing a major part in establishing AUST(Q) Superannuation, he became chairman and head of the investment committees of SPEC and ESI Super and continued in the combined role when the funds merged to form Energy Super on January 28, 2011.

Investment strategy

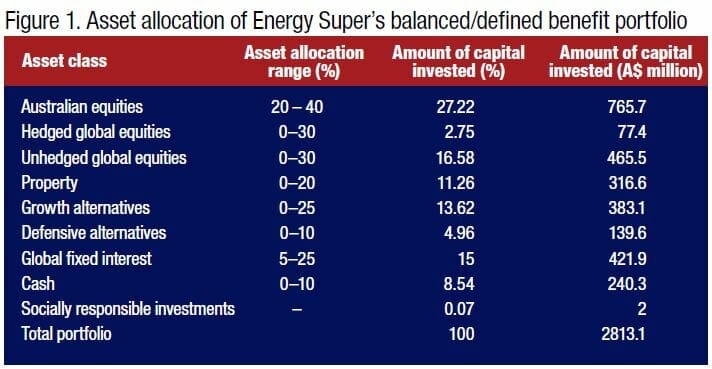

The best investments held by SPEC and ESI were chosen for the Energy Super portfolio.

“We basically picked the eyes out,” Henricks says. The fund’s 2011 annual report shows that it invests more than its benchmark does in unhedged international equities, property investments and “enhanced” cash, which blends discount securities, floating rate notes and mortgages with cash investments.

The fund aims to invest between 65 per cent and 80 per cent of its portfolio in “growth assets”, such as equities, even though just 12,000 of its 45,000 members are less than 30 years of age. Funds often advise younger members to invest more in equities because they can weather market volatility in pursuit of higher returns.

The fund “relies heavily” on its investment consultant, JANA Investment Advisers, for advice about investment strategy and selecting funds managers, Henricks says. It draws on actuaries within Sunsuper, the $19 billion Brisbane-based superannuation fund, to determine how much employers need to contribute to support DB payments. Guided by these advisers, the committee sets investment strategy and chooses managers.

It also seeks investments in good assets being sold cheaply. The committee has the autonomy to invest up to 3 per cent of the fund’s capital, or about $114 million, without board approval. But JANA and fund executives must be involved in these so-called opportunistic investments.

This enabled the committee to invest about $40 million with a global real estate funds manager aiming to raise capital from preferred investors at a recent meeting. Their deadline was the following day.

Small but attractive deals in markets with no clear direction can improve investment returns, Henricks says. “These days, the little fish are sweet.”

Direct investing

Some industry funds, such as the $29.8 billion UniSuper and the $4.4 billion Equipsuper, employ in-house investment staff to manage listed equity and fixed income assets.

Henricks does not believe EnergySuper should take this path. Investment managers provide a broader range of views than an investment team within a fund, he says.

“Massive funds can do it. They might have 100 people doing it,” he says, referring to the large internal teams staffed by overseas funds such as the Ontario Teachers’ Pension Plan. “But there will still be, in my opinion, a bias towards certain views.”

Leave a Comment

You must be logged in to post a comment.