How high is your portfolio’s exposure to potential stranded carbon assets? According to Generation Asset Management, stranded assets are those with a value that would change dramatically, either positively or negatively, under certain scenarios such as a reasonable price on carbon or water. The soon-to-be-introduced Clean Energy Plan will put a price on carbon emissions for the world’s highest emitter per capita, but the impact on investors is not yet well understood. For Australian companies and their shareholders, it represents a new risk factor, and the way it is managed will increasingly influence economic winners and losers.

Extreme losses for shareholders as a result of such stranded assets appear unlikely, at least in the short and medium terms, but the new Australian legislation can be seen as the latest indication that the global economy has entered a sustained period of transition to a low-carbon model.

Many experts believe that such a transition requires internalising negative environmental externalities through appropriate pricing, which presents significant opportunities and material risks for investment portfolios.

The opportunities result from the potential in emerging economic sectors such as energy efficiency, water technologies, and renewable and alternative energy. The risks posed to portfolios of potentially dramatic asset re-pricing will command a historic shift in conceptual, strategic and tactical- investment decision-making.

A vanguard of institutional investors, including many Australian superannuation funds, is already working to exploit the opportunities and manage the risks posed by climate change.

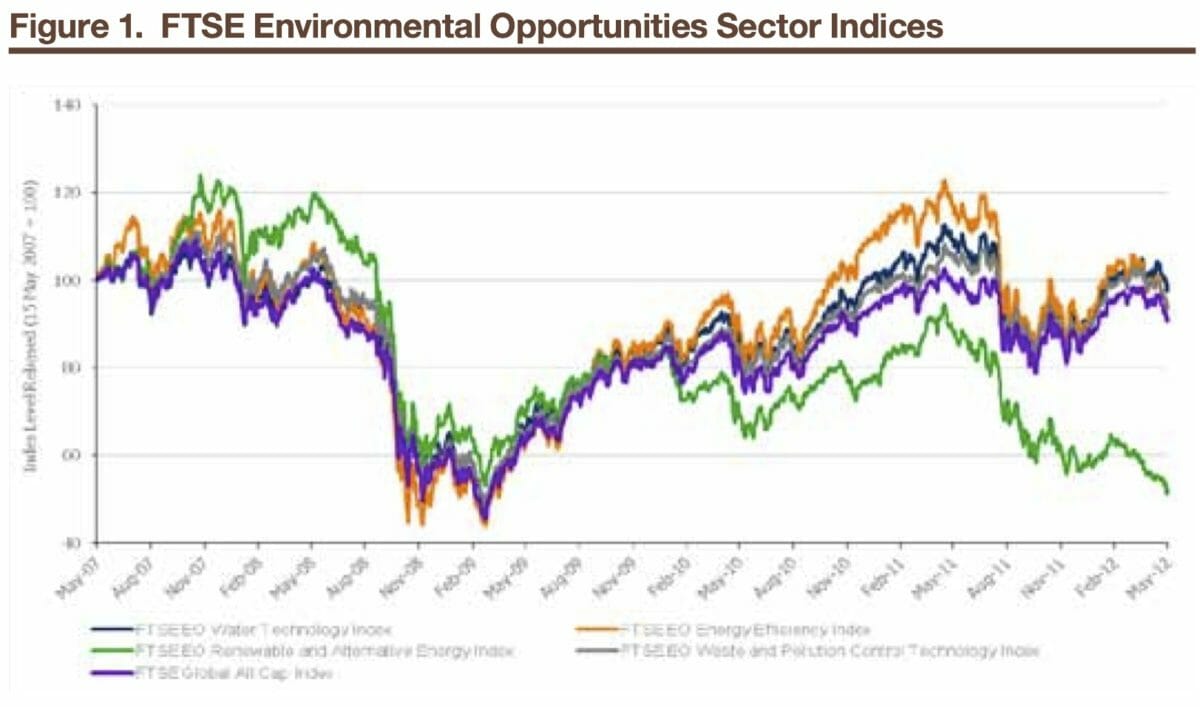

Much of the activity can be characterised as opportunity seeking: for example, the creation of satellite portfolios designed to enhance exposure to environmental sectors in an effort to generate alpha. Although the poor performance of renewable-energy stocks tends to cloud perceptions, the opportunities in environmental markets beyond renewable, in areas such as energy efficiency, water technology, and waste and pollution control, are more apparent.

The FTSE Environmental Opportunities benchmarks highlight the outperformance for these sectors relative to global equity markets over the last five years. See Figure 1.

The impact of carbon pricing

An area of considerable concern that is less well understood is how to identify and integrate carbon risk factors into existing portfolios and strategies. The exposure of superannuation funds to Australian listed companies can take many forms, such as through passive (index-tracking) portfolios.

What will the impact on the value of these portfolios of a price on carbon emissions be? The picture is not entirely clear – even ignoring the ongoing debate about the future of the carbon-price legislation under a different government, the lack of sufficient investment-grade data published by companies presents a challenge to those looking to factor carbon risk into investment analysis.

What is mostly clear is that in the immediate term, the impact on company valuations and portfolio performance will not be significant. However, the impact in the medium term is likely to be more meaningful as the price of emissions rises and, in the long term, there is potential for dramatic re-pricing of assets.

On a global scale, what would happen if the world’s governments decided to forcefully enact policies meant to cap the rise in global temperature at 2° Celsius? That would require strict limits on the burning of fossil fuels, in other words a “global carbon budget” linked to the projected rise in temperature.

According to analysis by Carbon Tracker, a system that calculates carbon dioxide uptake and release at the Earth’s surface over time, the burning of only about 20 per cent of all known fossil-fuel reserves by listed companies in the next 40 years would fill such a carbon budget, leaving 80 per cent of the reserves unexploited. The impact on the valuations of the companies whose reserves would go untapped would create a carbon- asset bubble, the results of which would dwarf subprime. And this scenario only includes listed-company reserves, which actually represent a smaller proportion of known global reserves compared to those of state-owned firms.

The track record of the negotiations on the UN Framework Convention on Climate Change suggests that such a policy scenario is practically unimaginable. However, the lack of global political consensus actually makes the risks even harder for businesses and investors to manage because it increases the likelihood of sudden policy shifts and patchwork approaches. But just thinking through the potential implications of serious attempts to limit carbon emissions should underline to asset owners the size of the potential risks they face.

Lower emissions, higher profits

The question of what to do about these issues is addressed by a growing set of analytical techniques and investment tools designed to support the integration of carbon risks. In particular there is a shifting awareness that so-called carbon footprinting – looking at historic emissions data as a measure of carbon efficiency – is a blunt method of risk analysis. Forward-looking analysis is required in order to measure risk exposure in carbon regulated markets.

Looking at the impact of the incoming Australian regulations on utilities illustrates this point. The carbon intensity of power generation will affect the ability of utilities to pass on the full costs of paying for emissions to consumers. The less efficient, highly intensive emitters will see their profit margins shrink. According to information from ENDS Carbon, a provider of carbon-performance benchmarking, the emissions-intensity inflection point for Australian utilities is currently estimated at 0.86 t CO2/ MWh. For companies that are more efficient than this, the new carbon costs will be outweighed by higher energy prices. For the less efficient, increased customer payments will not compensate for costly carbon-emission charges.

In this scenario, from 2012 to 2022 the average cost of carbon for a largely coal-fired utility, such as International Power, will represent a much higher proportion of projected profits than for companies such as Infigen and Origin, which have generation portfolios that utilise various renewable and alternative energy sources.

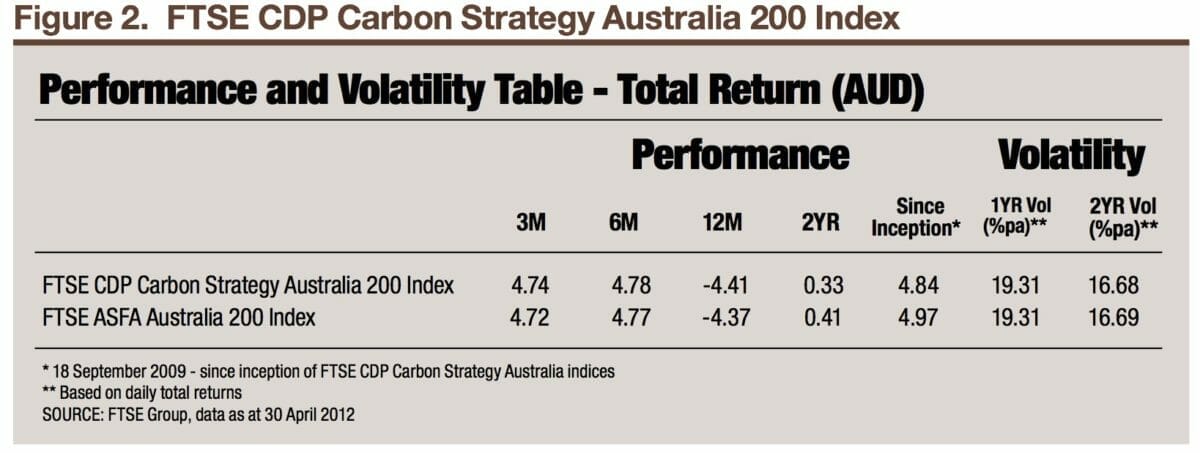

As carbon-risk analysis becomes more sophisticated, so too are the tools that allow investors to incorporate these factors. A new generation of carbon-risk-adjusted indexes allow investors to increase exposure to companies that best manage carbon risk and reduce exposure to those that manage it poorly, while retaining similar performance and risk/return characteristics of the conventional benchmark. The performance and volatility of the FTSE CDP Carbon Strategy Australia 200 Index compared to the FTSE ASFA Australia 200 index demonstrates the affect of this approach (see Figure 2).

In fact, the performance is so close as to be virtually undistinguishable. This underlines the fact that, at least initially, the carbon-risk adjustments in carbon strategy indexes will not be significant enough to drive significantly different performance. However, as the carbon price begins to increase, and as companies improve disclosure of key carbon-related metrics to meet new regulatory requirements, it can be expected that the “carbon-tilts” in the index will become more defined and lead to a greater divergence in performance from the standard benchmark.

The precise impact on investors of a price on carbon in Australia will only emerge over time. However, increasingly sophisticated methods of carbon risk analysis and the incorporation of these methods into investment tools such as indexes will support the capital mobilisation that is needed to achieve an efficient low-carbon economic system.

water technologies, renewable energy, alternative energy, institutional investors, Clean Energy Plan, Generation Asset Management, Australian superannuation funds, FTSE Environmental Opportunities benchmarks, carbon risk factors, stranded carbon assets, energy efficiency

Leave a Comment

You must be logged in to post a comment.