The Future Fund has its highest cash weighting since the first years of its existence, but claims it is not highly defensive as the allocation has been made to offset the risk in other areas as part of its one-portfolio strategy.

David Neal, chief executive of the Future Fund, said the increase in the cash balance highly overstated the level of defence in the portfolio, as the fund has been investing in some riskier opportunities in private markets – primarily in equities where they thought they could add value.

“Our private market portfolio is at the higher end of riskiness of what might be expected, and the same with our debt. To some degree that higher cash weighting is offsetting the slightly higher risk in other sectors,” Neal said.

“There is also a defensive motive in there of raising our cash levels.”

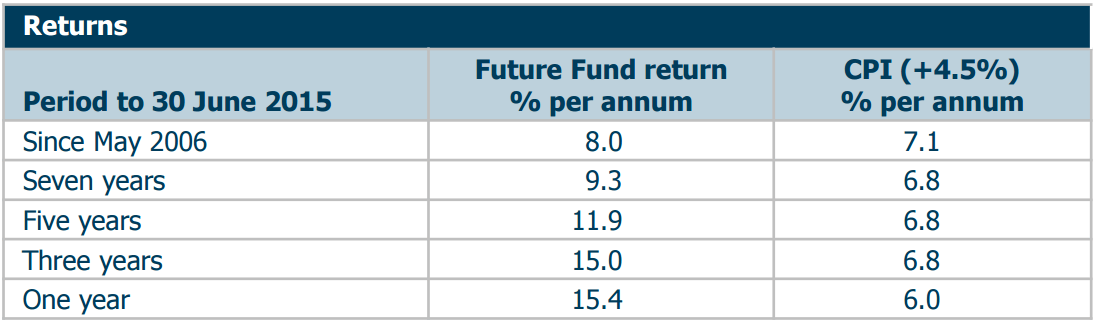

The result is the total portfolio risk is a little lower than average.

He added that he didn’t see any reason why the portfolio would change unless the environment around it changed, but qualified if they found good opportunities representing very strong risk adjusted returns, even given the perceived conditions, they would deploy the capital.

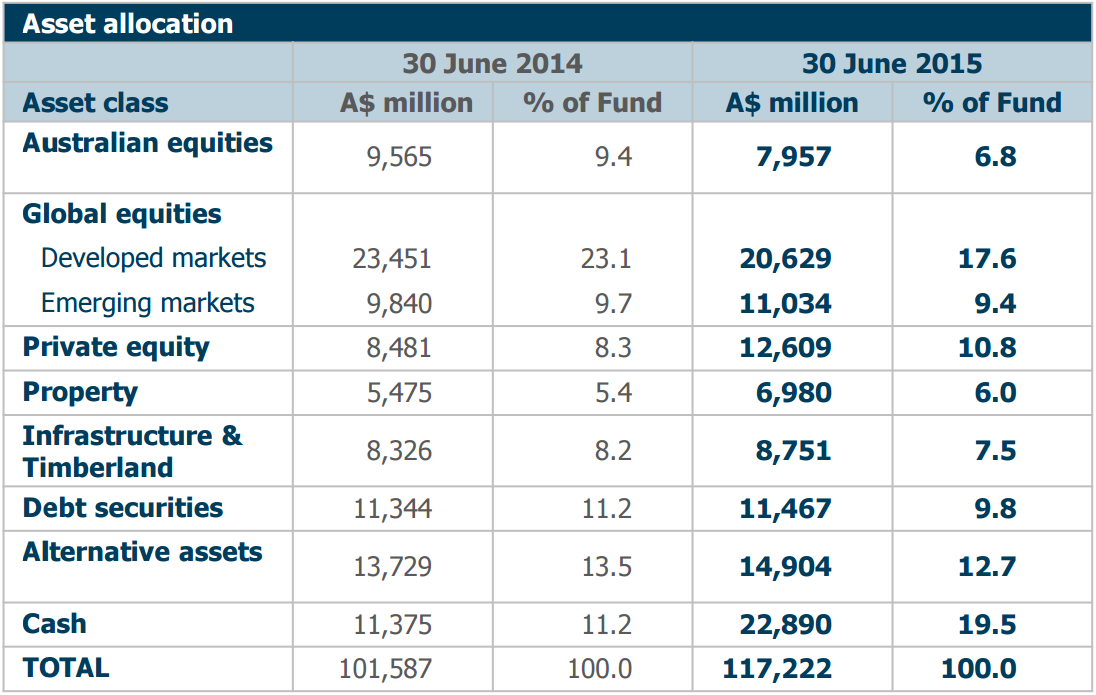

According to Neal the increase in private equity – an increase from 8.3 per cent to 10.8 per cent – has primarily been fuelled by currency moves. Most of the private equity portfolio is US dollar based, with some of it also being euro based. This exposure and the declining Aussie dollar has automatically increased the weighting in the fund’s portfolio.

Neal also touched on the limits of strong monetary policy in a number of markets counter-acting the deflationary pressures from very high debt levels from across much of the world.

“One thing I would highlight is we are concerned the monetary policy has been in place for such a long time now … it’s difficult to see that’s there is much fuel left in the global monetary policy tank. That does concern us a little – the ability for the global policy is a little less than we’d like.”

The latest figures show a 19.5 per cent cash allocation as of June 30, 2015, up from an 11.2 per cent allocation in June 20, 2014. The majority of the move to cash has happened since Christmas. In December 2014 the allocation was 12.8 per cent rising to a five year high in March at 15.2 per cent.

The only time the cash holding has been higher was the first years of its existence as it moved away from 100 per cent cash to a more diversified portfolio.

Leave a Comment

You must be logged in to post a comment.