Asset owners will be on a steep learning curve working out how their investment portfolios interact with – and impact – nature. In meeting the reporting challenges presented by the final recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD), they will be hoping to draw as much as they can upon what they have been asked to do on climate.

There are, however, a couple of big differences between the TNFD and the Taskforce on Climate-related Disclosures (TCND) frameworks. The identification, assessment and management of nature-related issues will be more complex. Unlike climate’s carbon dioxide equivalent (CO2e), there is no single metric of measurement for nature change, or any universally agreed global architecture like the Greenhouse Gas Protocol.

Asset owners will need to start reading up on biodiversity footprint and index metrics like mean species abundance (MSA), potentially disappeared fraction (PDF), the biodiversity intactness index (BII) and the ecosystem integrity index (EII).

Climate change is a global process within one shared atmosphere that lends itself to global policies and responses. But as the TNFD notes “nature-related impacts and dependencies, by contrast, are location specific, and therefore require local, context-specific assessment and responses”. Understanding exactly where portfolio interactions with nature occur is vital.

The Trail Guide

The atmosphere is one of nature’s four realms (along with land, freshwater and ocean) and because of the global warming crisis it became our initial focus for the economy’s interaction with nature. The frameworks, tools and governance approaches created for climate change will be helpful in dealing with the rest of nature, according to advisory firm Pollination.

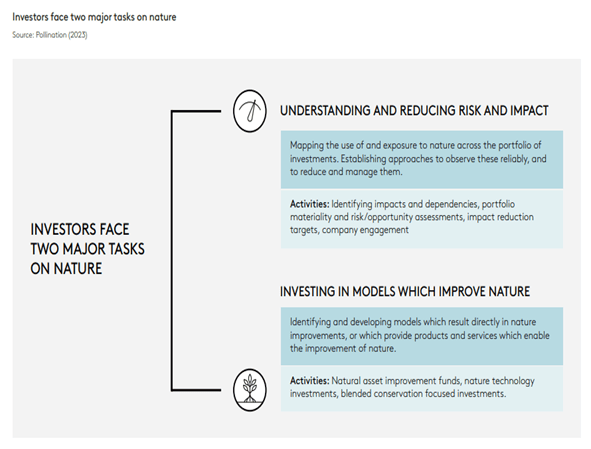

In its Tracking Global Trends in Nature Investment report, Pollination says the TNFD sets two main tasks for asset owners and other investors.

- Understanding the exposure and impact of their current portfolios and working to improve them. This requires investors to build knowledge of the foundations nature currently provides for the companies or assets in their portfolios, and the effects that portfolios have on nature now. These are what the TNFD framework refers to as dependencies and impacts.

- Investing in enabling opportunities and in nature improvement. This means investing in specific companies and assets which enable the improvement and recovery of natural assets. This will include providing capital to specific initiatives by companies to improve their nature footprint; investments in new products and services that help companies manage their relationship with nature; and direct investment in natural assets themselves.

Taking the LEAP

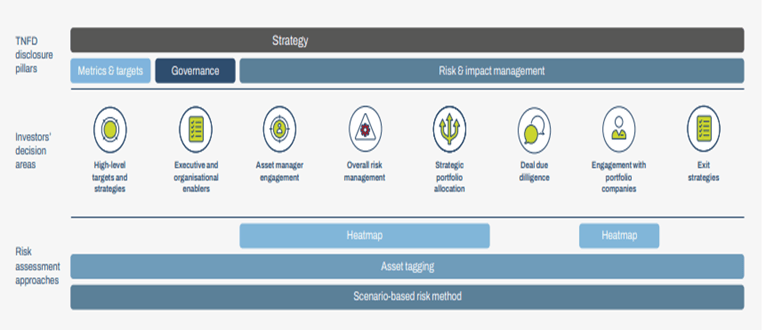

The TNFD has published extensive guidance, including “Guidance on the identification and assessment of nature-related issues”, The TNFD LEAP approach and its “Additional guidance for financial institutions”, which is aimed at assisting asset owners.

The TNFD’s LEAP framework (Locate, Evaluate, Assess, Prepare) is an approach for identifying and analysing the impacts and dependencies of the companies/activities in an asset owner or manager’s portfolio. LEAP has been designed to build on, and be consistent with, existing assessment frameworks including the Natural Capital Protocol and the target-setting methods of the Science Based Targets Network (SBTN).

Without going too far into the weeds, LEAP typically involves creating a heatmap to show an investor’s portfolio exposure to a range of nature-related dependencies and impacts across industry sectors. Asset tagging can deepen the heatmap using location-based metrics and data specific to financial or corporate assets to assesses the degree of exposure – and to identify individual portfolio companies or assets with high nature impacts or dependencies. Various scenario-based risk assessment methods can then build upon the heatmapping and asset tagging, to translate exposure to nature-related risks into financial implications for organisations.

While all this sounds good in theory, things may prove to be a little harder in practice. The World Business Council for Sustainable Development’s (WBCSD) recent “Lessons from TNFD piloting with 23 global businesses” report observed that “it may not always be possible for financial institutions (FIs) to follow the LEAP approach.

“For example, it was difficult to obtain location-specific data, which is a prioritization criteria for the ‘Locate’ stage of LEAP. This stage was deemed to be too granular for some FIs, and therefore the majority started the LEAP approach with either the ‘Evaluate’ or ‘Assess’ stage following the initial scoping”.

The TNFD also recognises that asset owners and managers depend upon their investees for data and when gathering data on portfolio exposures will also often turn to external data providers, or to proxy and/or modelled data. TNFD hopes “as investees start to assess and disclose aligned with the TNFD recommendations, it can be expected that more and better quality data and analytics will become available directly from companies over time”.

Asset owners will be hoping so. This month the World Benchmarking Alliance (WBA) released the 2023 iteration of its Nature Benchmark that assessed 350 major companies from across the food and agriculture value chain, looking at their contributions to halt and reverse nature loss.

The WBA report found that although food and agriculture companies “bear an enormous responsibility for two of the biggest drivers of environmental degradation: land use change and the exploitation of nature” only 2 per cent of the biggest 350 currently disclose their environmental impacts. And despite being heavily nature-dependent industries, zero per cent “holistically address their dependencies on nature”.

While some companies have begun assessing their impacts and dependencies, “they often only cover a fraction of their operations or don’t publish the results,” WBA says. Unsurprisingly, WBA suggests that “to bridge this gap” they should adopt a framework like the TNFD.

Following the Heatmap

The TNFD says risk assessments can help asset owners prioritise and engage with asset managers on nature-related topics. Asset owners can then start conversations with asset managers to encourage the development of nature-related risk management processes and emphasise the importance of producing nature-related disclosures.

The asset tagging and scenario-based risk assessment approaches can help prioritise portfolio companies to engage with on the management of nature-related risks and opportunities and also help prioritise specific dependencies and impacts for active engagement.

Risk assessments also help asset owners to adjust their risk management structures and procedures. They could inform the development of exclusionary policies for certain sectors, activities or geographies as well as define metrics against which to track progress.

The TNFD guidance says this could also guide strategic portfolio allocation “that could entail divestment or diversification from sectors and geographies identified to be high risk or directing capital to new sectors or businesses identified to be making a positive contribution to nature”.

Metrics maze

The TNFD asks asset owners to disclose the absolute amount or percentage of invested or owned assets in sectors considered to have material nature-related dependencies, and in companies with activities in sensitive locations.

They will need to disclose, for example, their portfolio share of investments in investees “that engage in activities that cause land degradation, desertification or soil sealing”; or “with sites/operations located in or near to biodiversity-sensitive areas where activities of those investee companies negatively affect those areas”.

Asset owners will be hoping they don’t get lost in the metrics maze.

Leave a Comment

You must be logged in to post a comment.