As COP28 kicks off in Dubai, Australia’s second largest oil and gas producer Santos is at the vanguard of the petroleum industry’s efforts to promote carbon capture and storage (CCS) as a genuine contributor to a net zero economy.

Santos says it has just “strengthened its position as a regional CCS leader” through a collaboration agreement with the Abu Dhabi National Oil Company (ADNOC) to “explore the potential for establishing a platform” offering decarbonisation services.

ADNOC’s CEO is COP28’s president Sultan Ahmed Al Jaber, who is also the Minister of Industry and Advanced Technology of the United Arab Emirates (UAE), the COP28 host nation that relies on oil and gas for 37.5 per cent of its GDP.

Santos’ Moomba CCS project in the Cooper Basin should begin carbon dioxide (CO2) injection in 2024 and the company also has an MOU with APA Group to develop infrastructure linking heavy CO2 emitters in eastern Australia to its Moomba storage site.

Santos CEO Kevin Gallagher recently told the WA Energy Club that “the climate enemy is emissions, not fossil fuels”; that shutting down the oil and gas industry would “slow the pace of the energy transition”; and that CCS “could be an exciting new industry for Australia in Asia”.

Asking too much

But should asset owners and managers be setting much store by what Santos and other petroleum producers are saying about CCS?

CCS is the capture, transport and permanent storage of CO2 into deep geological formations such as depleted oil and gas reservoirs or saline aquifers.

Projections of how much CO2 must be geologically stored to achieve net zero emissions vary considerably depending upon the assumptions of the scenario or model used. The major scenarios and models currently assume CCS will be providing 8-11 per cent of the reductions needed.

The Global CCS Institute says the world needs to store more 100 gigatonnes (Gt) between 2020 and 2050, requiring annual storage rates of approximately 1 Gtpa by 2030, growing to around 10 Gtpa by 2050. In its Global Status of CCS 2023 report, the GCCSI asks itself “is this level of scale-up feasible?”

The volume of CO2 captured varies widely across the many scenarios that have been produced but the most widely used – such as those prepared by the IPCC and the International Energy Agency (IEA) – now assume between 6 and 8.5 Gt need to be captured by 2050.

The GCCSI is probably sticking with its higher figure given its raison d’etre – since being established (with noble intentions) in 2009 by then Australian Prime Minister Kevin Rudd – is promoting CCS technologies.

An order of magnitude

The GCCSI report says if all the CCS facilities in the development pipeline commenced operations on time and operated at full capacity, they could, theoretically, store a total of 12 Gt of CO2 between now and 2050.

The gap between this geological storage capacity under development and the capacity required to meet climate targets “is an order of magnitude,” the GCCSI admits.

Currently just under 50 Mtpa of CO2 is being stored globally. However, the vast majority of this represents Enhanced Oil Recovery (EOR) – where CO2 is injected into near-empty oil reservoirs to extract more oil. EOR is commonly operated without the level of monitoring normally associated with CCS to confirm that the CO2 has been permanently stored.

The only significant dedicated geological storage project that is operating is Western Australia’s Chevron Gorgon Project. Gorgon has a 4 Mtpa CO2 storage capacity but due to its well-documented delays and technical problems it is s only managing to store 1.7 Mpta.

So, this means probably only 10 Mtpa (or 0.01 Gtpa) is being geologically stored compared to the 10 Gtpa the GCCSI says is needed by 2050. This is certainly an order of magnitude.

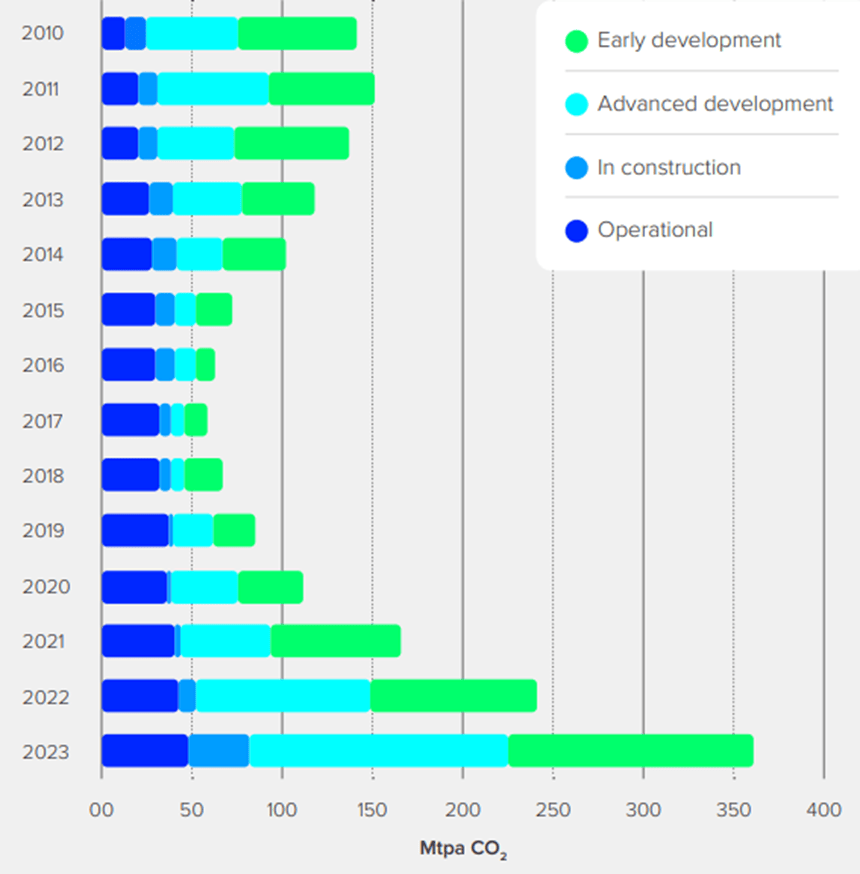

Little progress

The chart above highlights how little actual progress has been made over the last 13 years. While there has been a recent big jump in the number of advanced and early stage developments this may another false dawn for CCS.

The increased project activity is largely a response to the huge stimulus provided to CCS (and other technologies) by the United States’ Inflation Reduction Act (IRA), which the GCCSI hopes “could increase CCS deployment in the US by 200 to 250 Mtpa of CO2 by 2030”.

However, some of these CO2 transport and storage hub projects – mainly located in the Midwest – are already collapsing or being delayed due to fierce opposition by environmental, community and landowner groups.

Navigator Resources has cancelled its Heartland Greenway project citing “the unpredictable nature of the regulatory and government processes involved”. The US$4.5 billion Midwest Carbon Express pipeline project is also now on a slower track with its start date pushed out to 2026.

A distraction

According to the latest Climate Action Tracker report “CCS is nowhere near the scale and commercial viability needed to deliver on emissions reductions at scale, in large part due to technological and cost challenges”.

The report Countdown to COP28 describes CCS as a “distraction” that should be “ limited to industrial applications where it is proven there are no other options to reduce process emissions”.

Climate Tracker is concerned too many countries are focused on “CCS, hydrogen and ammonia co-firing and e-fuels as a means of prolonging fossil fuel infrastructure and production”.

Australia is one of those countries, with the oil and gas lobby vigorously promoting blue hydrogen – or what it calls ‘low carbon hydrogen’ – projects where gas is used to produce hydrogen on the premise/promise the resultant CO2 will be geologically stored.

“These counterproductive activities not only risk prolonged dependencies on fossils, they also require money and time that should be spent on the scale up of sustainable long-term solutions,” the report says.

Even the IEA believes there is “excessive expectations and reliance” on CCS. In its The Oil and Gas Industry in Net Zero Transitions report, the IEA says that while CCS has a role in achieving net zero emissions in certain sectors and circumstances, “it is not a way to retain the status quo”.

The report says “if oil and natural gas consumption were to evolve as projected under today’s policy settings, this would require an inconceivable 32 billion tonnes of carbon captured for utilisation or storage by 2050” to limit the temperature rise to 1.5 °C”.

Budget has been blown

The Production Gap Report 2023 also argues that given the risks and uncertainties of CCS “countries should aim for a near total phase-out of coal production and use by 2040 and a combined reduction in oil and gas production and use by three-quarters by 2050 from 2020 levels, at a minimum”.

The report – lead authored by the Stockholm Environment Institute – is concerned institutional, technical, and financial barriers will see CCS deployment rates “continue to fall below expectations and remain far below those modelled in integrated assessment models (IAMs).

The report says “if fossil-CCS fails to scale to the levels envisaged by these scenarios, reductions in fossil fuel production and use need to be even faster”.

Sparsely populated

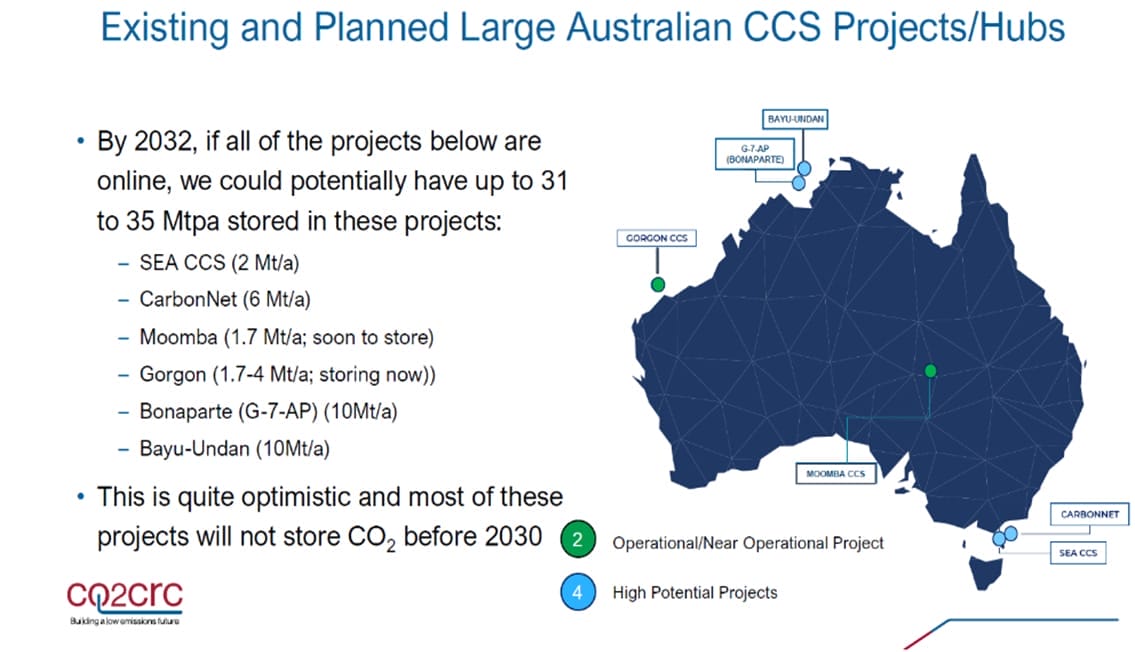

Australia’s CCS project map is rather sparsely populated and most of the planned projects (see map below) will not be storing CO2 before 2030. On the map is the Bayu-Undan CCS project where Santos wants to bury CO2 emissions from its controversial Barossa Gas Project into depleted gas fields in the Timor Sea.

The WA Government, meanwhile, says it is developing a CCUS Action Plan that envisages the Pilbara and Perth-Kwinana regions becoming carbon capture, utilisation and storage (CCUS) hubs supporting blue hydrogen, ammonia and fertiliser projects.

However the WA CCUS Hubs Study suggests this is all dependent on heavy government support to incentivise investment in CCUS. The study warns “if WA waits until CCUS projects are economic for developers and customers, there likely won’t be enough time to get the projects operational before 2050”.

The IPCC’s AR6 Synthesis Report says CCS faces “technological, economic, institutional, ecological-environmental and socio-cultural barriers” and “global rates of CCS deployment are far below those in modelled pathways limiting global warming to 1.5°C to 2°C”.

Perhaps the day of reckoning is close at hand for the oil and gas industry. If the modellers attending COP 28 realise they need to dramatically downgrade their inputted assumptions about CCS’ contribution to net zero this would also mean slashing assumptions about how much fossil fuel production can be allowed.

Disclosure: The author attended COP15 in Copenhagen to promote Australia’s CCS capabilities.

Leave a Comment

You must be logged in to post a comment.