Late last month, Australia’s major profit-to-member super funds released a ‘policy blueprint’ designed to accelerate significant superannuation investment in Australia’s energy transition.

The Super-powering the energy transition report nominated sustainable aviation fuels (SAF) as an area where government policy reform could significantly scale up development and help create a local SAF industry.

To this end, AustralianSuper, ART, CareSuper, Cbus, HESTA, Hostplus, Rest Super, UniSuper and industry super-owned IFM Investors recommended introducing a production tax credit, establishing a SAF certification framework, and developing a market for credits to be recognised and traded.

The world’s airlines are eagerly promoting SAF as the best route to aviation industry emission reductions and are lobbying governments – who hope SAF offers a quick-fix solution – to fund and incentivise its global scale-up.

The Australian Government’s recently released Aviation Green Paper: Towards 2050 noted stakeholder calls to introduce blending mandates, draft low-carbon fuel standards or set public targets for future SAF consumption to provide a clear ‘demand signal’ to the market.

With Australia’s industry funds also now booking their tickets on the SAF journey, time will tell whether SAF will take off, or whether they will be left stranded on the runway.

There are two big issues with SAF – the huge quantities that are need to be produced to meet the hard-to-abate aviation industry’s emission goals, and the extent to which SAFs live up to their ‘sustainable’ label.

Hope or hype?

The London-based Aviation Environment Federation (AEF) says the term ‘SAF’ – which has been coined by the aviation industry and widely adopted in political and public debate to describe all non-kerosene liquid fuels for aviation – is “unhelpful”. AEF’s recent report Sustainable Aviation Fuels: hope or hype? says the “sustainability of alternative fuels needs to be assessed, not assumed”.

In other words, it is not good enough to claim aviation fuel made from, say, used cooking oil is ‘sustainable’ by simply applying the widely-used carbon accounting convention that the carbon dioxide (CO2) emitted when an aircraft burns the fuel is equal to (and, therefore, negated by) the CO2 that was absorbed by the canola plants grown to produce the cooking oil.

“We need a better-quality conversation about how alternative fuels work as a tool of climate mitigation, based on the understanding that they deliver no CO2 reduction at the tailpipe.

“CO2 emissions from aircraft are not reduced at all as a result of switching from kerosene to an alternative hydrocarbon. Any carbon reduction being claimed cashes in on CO2 that has been captured at some point in the past, according to the report.

AEF says “at the moment there is a risk of greenwash in public discussion, and of goal-setting at a political level that isn’t based on the right information”.

Life cycle analysis

This is where Life Cycle Analysis (LCA) comes in. LCA is the default approach for assessing fuel sustainability, but the LCA score of a fuel can vary wildly depending on the assumptions fed in.

For example, a recent academic study (Moretti et al) used both attributional and consequential LCA models to assess an innovative bio-jet fuel produced from potato by-products in the Netherlands. The attributional LCA showed that biojet fuel could offer about 60 per cent in GHG emissions reductions compared to conventional jet fuel.

However, the consequential LCA estimated a much lower climate change benefit (5-40 per cent) if the potato by-products taken from the animal feed market had to be replaced with European animal feed. Further consequential LCA also showed a 70 per cent in GHG emissions if imported soybean meals were used to replace the feed.

The Aviation Green Paper also acknowledges the problem. “Biofuels can emit more GHGs than some fossil fuels on an energy-equivalent basis, depending on production process and time horizon of analysis. Crop-based feedstocks may also compete with food production, potentially increasing the cost of essential grains and cooking oils,” it says.

“Robust certification arrangements, which provide assurance of SAF environmental credentials will be required to support confidence in SAF integrity,” according to the Green Paper.

The hurdle to be an eligible SAF under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) is not a high one. The fuel only needs to “achieve net GHG reductions of “at least 10 per cent compared to the baseline life cycle emissions values for aviation fuel on a life cycle basis”.

However, the International Air Transport Association (IATA) generally prefers to talk about how SAF “reduces CO2 emissions by up to 80 per cent”.

If the super funds are planning to pick SAF winners, they should remember not all SAFs are created equal and that some may, at best, offer only marginal emission reductions.

Different trajectories

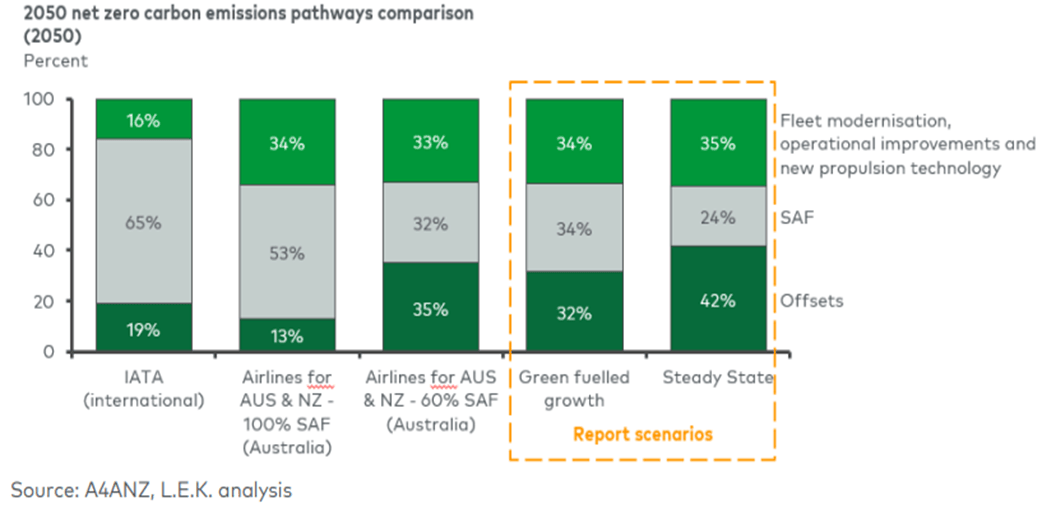

Globally, IATA estimates SAF could (theoretically) contribute around 65 per cent of the reduction in emissions needed by aviation to reach net-zero in 2050 (assuming the complete replacement of existing kerosene fuel with SAF).

The Airlines for Australia & New Zealand (A4ANZ) industry group – whose members include Qantas, Virgin Australia, Regional Express (Rex), Jetstar, and Air New Zealand – estimates 100 per cent SAF could provide them with 53 per cent of the emission reductions they require.

At 60 per cent blend, the LEK chart above shows that SAF provides less than a third (32 per cent) of the emission reductions needed. In LEK’s ‘green fuelled growth’ scenario, this rises to only 34 per cent (with LEK also assuming ‘second-generation’ SAFs will need to be developed).

While SAF is regarded as “drop-in” replacement for conventional jet fuel (because aircraft engines and existing airport fuelling systems do not have to be modified to use it) airlines are currently only permitted a maximum 50 per cent SAF in their fuel mix.

Empty tank

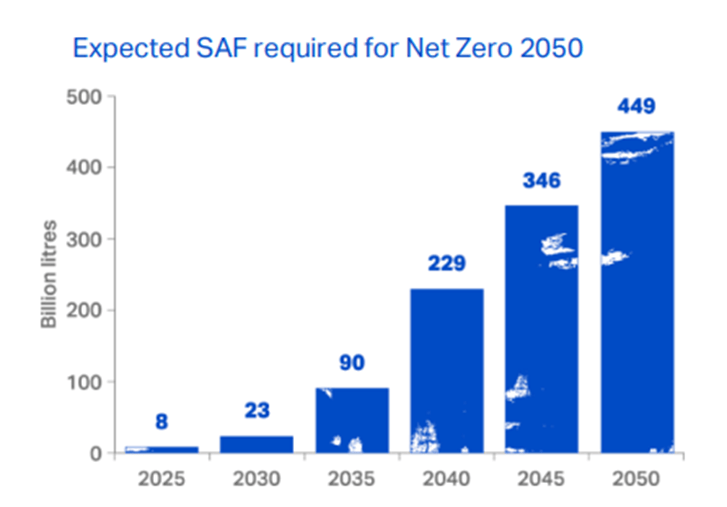

SAF is the only proven solution to replace traditional aircraft kerosene, but “virtually no SAF is available to our industry today,” according to IATA’s senior vice president sustainability and chief economist Marie Owens Thomsen.

Speaking at the recent Third Conference on Aviation Alternative Fuels (CAAF/3) in Dubai, Thomsen said “merely 0.1 per cent of airlines’ fuel demand (or just 300 million litres) was met by SAF in 2022 and we estimate that this will rise to 0.2 per cent in 2023”.

Thomsen said “the SAF market is in its infancy, and energy producers are slow to seize what should be a golden opportunity, especially considering that the price of SAF is 2 to 4 times higher than that of kerosene”.

As an indicator of how desperate the industry is, IATA says airlines “have entered into forward purchase agreements for SAF worth around a total of US$45 billion, well in excess of today’s SAF availability”.

Meanwhile, the aviation industry’s CO2 emissions are soaring again, with global passenger movements having almost climbed back to pre-COVID levels.

IFM Investors certainly has a big vested interest in SAF given its significant ownership stakes in nearly every major airport in Australia and its growing investments in UK and European airports.

IFM laments that Australia does not have the refining capabilities to produce SAF domestically – which means feedstock is being exported, refined overseas and then imported back as a renewable fuel.

In its most recent SAF initiative, IFM announced an MOU with GrainCorp for feasibility studies on producing fuel using domestic feedstock such as waste, residues, and crop-based oils.

The 17 Australian industry super funds that collectively own the global infrastructure investor will no doubt keenly track the progress of its SAF waste-to-wing journey.

Leave a Comment

You must be logged in to post a comment.