Asset owners head into 2024 facing an emboldened oil and gas sector even less inclined to waste much time and energy on tedious matters such as their climate transition plans.

The sector is still celebrating the success of its COP28 lobbying efforts. The text of the global stocktake agreed at COP 28 only “calls on parties to contribute…in a nationally determined manner” to “transitioning away from fossil fuels in energy systems”.

There are no targets or progress milestones to meet between now and 2050.

The text also calls for “accelerating” the development of “removal technologies such as carbon capture and utilization and storage (CCUS)”. These are sweet words for gas companies in particular, as they can continue to argue gas has an important role in the transition to net zero emissions (NZE), allowing them to roll out more big projects on the dubious premise that their greenhouse gas emissions (GHG) emissions will be captured.

Before COP28 the International Energy Agency (IEA) said oil and gas producers had to “choose between contributing to a deepening climate crisis or becoming part of the solution by embracing the shift to clean energy”. The IEA said the oil and gas companies had to let go of “the illusion that implausibly large amounts of carbon capture are the solution”.

Unfortunately, the oil and gas companies will view the COP28 outcome as giving them another choice – that is, continuing to seek approval to develop new projects, claiming incorporating CCUS into these projects represents a credible transition plan.

So when asset owners ask to see an oil and gas company’s ‘climate transition plan’ what they will probably be handed is something that could instead be called an ‘acclimatisation plan’ showing how they intend to adjust and adapt to operate as close to business-as-usual (BAU) for as long as they can.

IEA transition scenarios

The IEA says the oil and gas sector “has been a marginal force at best” in transitioning to a clean energy system. Oil and gas companies currently account for just 1 per cent of clean energy investment globally. Less than 10 per cent of current global petroleum production comes from companies that have announced a target to diversify their activities into renewable power.

However, in a pathway to reaching net zero emissions by 2050 – which is necessary to keep the goal of limiting global warming to 1.5 °C within reach – oil and gas use would need to drop more than 75 per cent by 2050.

The IEA’s recent The Oil and Gas Industry in Net Zero Transitions report provides illustrative examples of what today’s major oil and gas companies might look if they did choose to scale up clean energy activities and evolve their portfolios to be more aligned with the NZE Scenario

The seven oil and gas majors, for example, currently each produce on average 1.5 million barrels of oil per day and 65 billion cubic metres of gas per year.

One transition option would be to continue producing this amount of oil and gas every year but to rapidly expand the use of CCUS and carbon removal to avoid the associated emissions.

However, given the vast cost of doing this (around USD$25 billion every year to 2050) the IEA says this approach is “likely an option only in theory”. So asset owners should be very wary if this is the basis of an investee company’s transition plan.

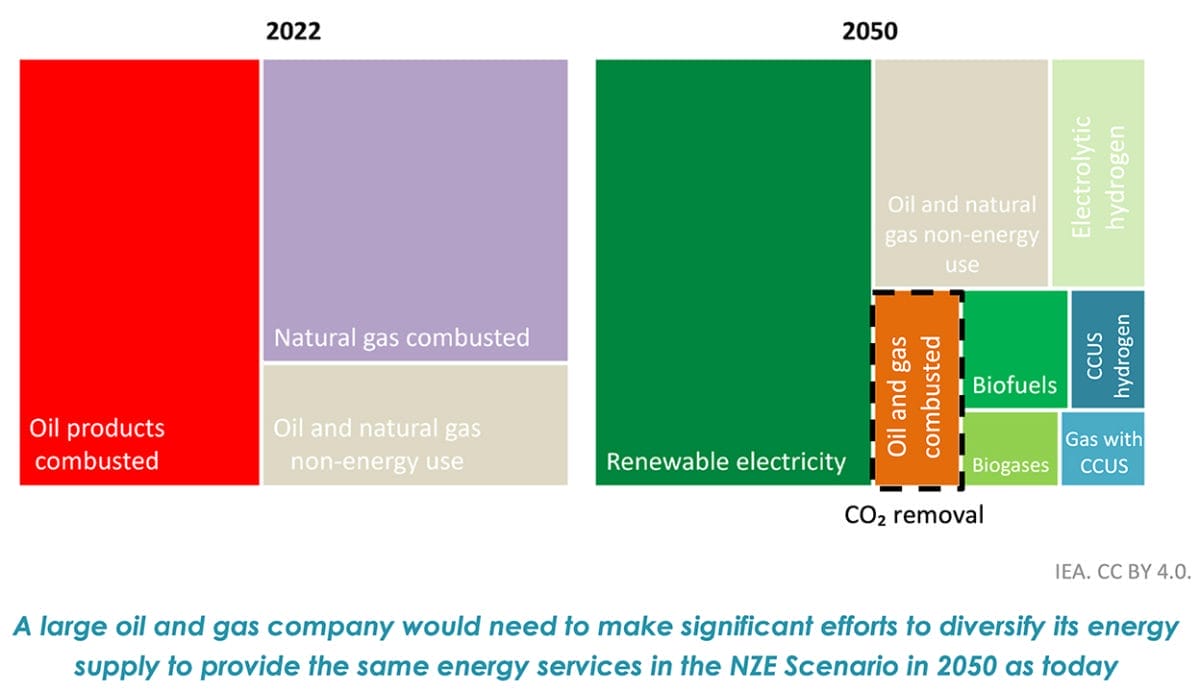

A genuine transition plan would see a large portion (say, 50 per cent) of the company’s energy portfolio in 2050 consist of renewables. In the IEA example below more than 300 gigawatts (GW) of renewables would be needed to replace some of the energy services currently met by oil and gas.

The IEA assumes oil and gas are still used in sectors where the fuels are not combusted and in some industrial facilities equipped with CCUS.

A major’s energy production portfolio in 2050 aligned with NZE Scenario

Few companies look like they are taking this sort of path, though. The IEA acknowledges there are some challenges here for oil and gas companies. Their activities are typically associated with a high level of risk and reward and accompanied by a high degree of volatility in returns.

However, clean energy technologies “often have more tightly controlled or regulated returns and so, while they may have a similar overall level of return on capital invested as oil and gas, they do not display such large year-on-year fluctuations and thus have fewer opportunities for windfall profits,” the IEA says.

There is also the issue that the big cut in oil and gas profitability assumed under the NZE Scenario would make it harder for the sector to raise the capital needed to diversify into clean energy.

The IEA notes an alternative approach that would also be fully aligned with the NZE Scenario “would be simply to wind down oil and gas operations in line with the overarching declines in oil and gas demand”. This would involve share buybacks and/or returns of capital.

However, most oil and gas boards would not see this as a ‘transition plan’ but more as an ‘extinction plan’ that would put them out of a job.

Worrisome Woodside

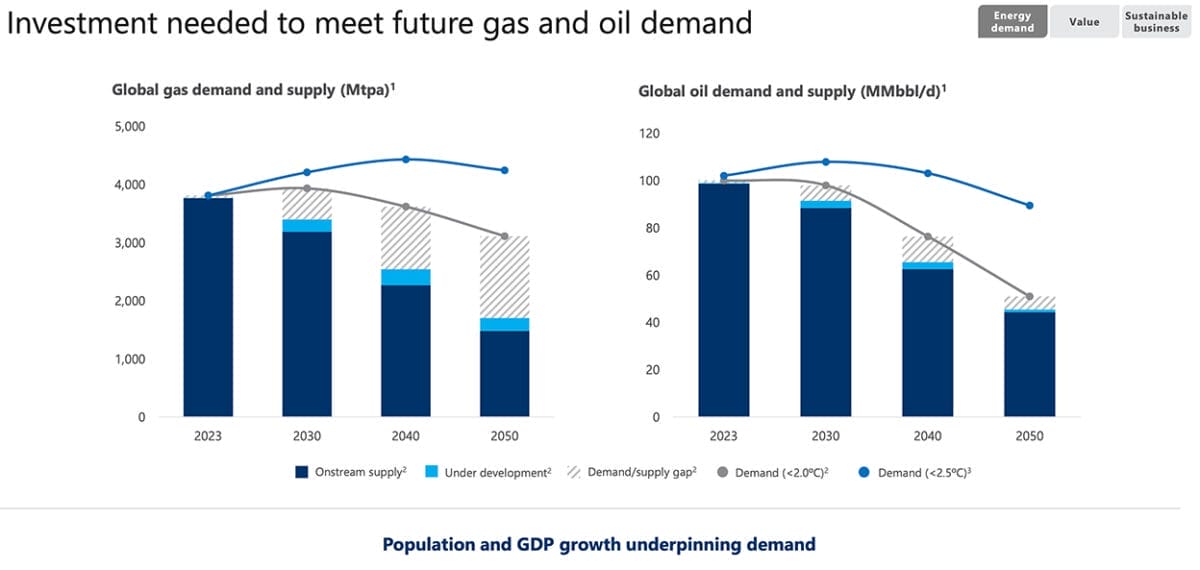

Woodside CEO Meg O’Neill recently told investors it was “clear, that under current forecasts, supply from gas and oil projects that are operational today and under development, will not meet future demand. And additional investment in gas and oil is required”.

Woodside investor presentation charts

1. Wood Mackenzie 2023 Energy Transition Outlook, September 2023. This slide presents a demand outlook based on two of many possible scenarios. For further detail refer to Woodside’s Climate Report 2022.

2. Wood Mackenzie pledges scenario, assumes global temperatures rise to around 2.0°C compared to pre-industrial levels.

3. Wood Mackenzie base case scenario, assumes global temperatures rise less than 2.5°C compared to pre-industrial levels.

Interestingly, the charts (above) in O’Neill’s presentation assume global temperatures rise <2.0 – <2.5°C – and they don’t include the more ambitious 1.5°C goal.

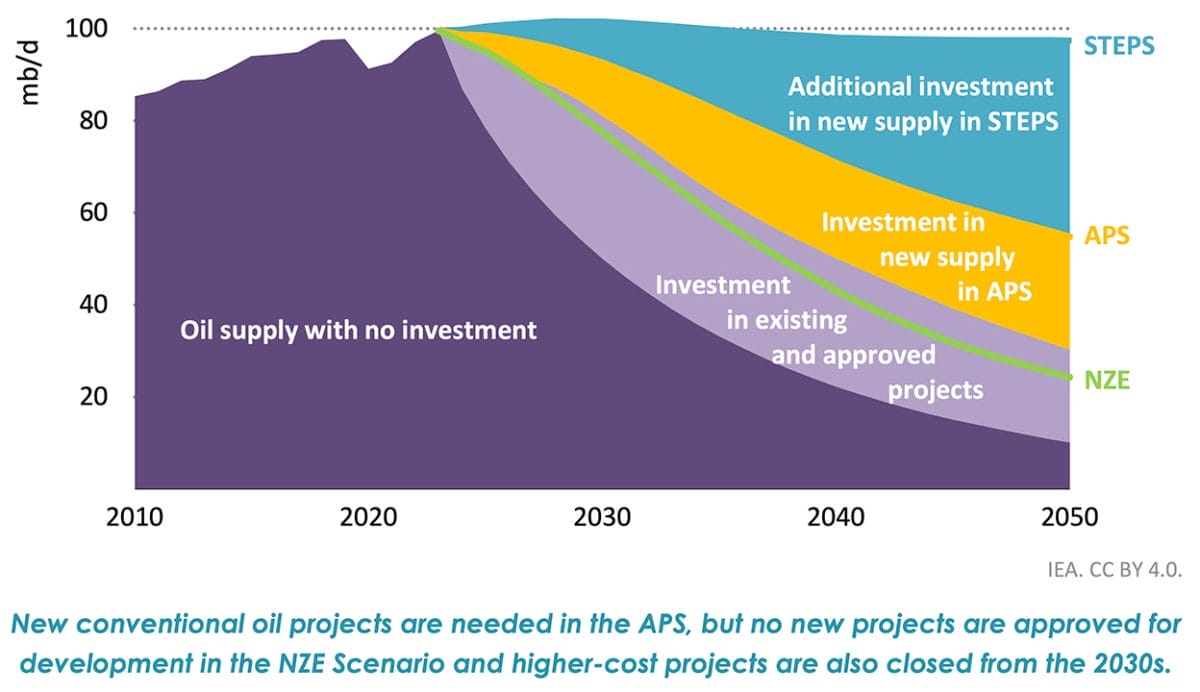

This is probably because under the NZE Scenario, falling demand can be met without any new long lead-time upstream conventional projects (see diagram below).

“Companies aligned with the results of the NZE Scenario would not invest in new exploration or approve new projects,” the IEA says.

Oil and gas becomes less profitable and a riskier business as net zero transitions accelerate. This means those companies who choose not to support the energy transition are betting that the transition falters.

Natural gas supply by scenario

Last ones standing

Advocacy groups such as The Australasian Centre for Corporate Responsibility (ACCR) argue that companies like Woodside and Santos would better serve their investors – and the planet – by winding down rather than ramping up their business.

ACCR argues that at Woodside “returning capital to shareholders presents greater upside than pursuing its risky growth portfolio” and “may well appease the significant block of Woodside shareholders that remain aghast at the board’s responsiveness to their climate concerns”.

However, the recent revelation that Woodside is discussing a possible merger with Santos suggests it is more focussed on being a proactive participant in the current industry consolidation that has seen a number of mega mergers and acquisitions.

The IEA, meanwhile, warns “not all producers can be the last ones standing”.

“Many producers say they will be the ones to keep producing throughout transitions and beyond,” it says. “They cannot all be right.”

Make up your mind

Asset owners should be braver in admitting when their oil and gas engagement activities have failed or are unlikely to produce the desired results, especially when a company has clearly chosen not to be part of the climate solution.

While asset owners may not be able to diversify away from climate-related impacts, that is no reason to continue owning shares in companies with no credible transition plans and with stated strategies that could continue to contribute to the climate crisis for decades.

There is also a bolder alternative. If the mind of a company board cannot be changed, a coalition of like-minded asset owners could use their combined voting power to seek to change the board.

Leave a Comment

You must be logged in to post a comment.