It’s time for the super sector to bust the myth that higher investment fees necessarily mean lower returns for members, the Fiduciary Investors Symposium has heard.

With RG97 and the Your Future Your Super performance test pushing a strong narrative of bringing down fees at all costs, members may actually be missing out on attractive net returns from more expensive to manage asset classes, said Chant West general manager Ian Fryer.

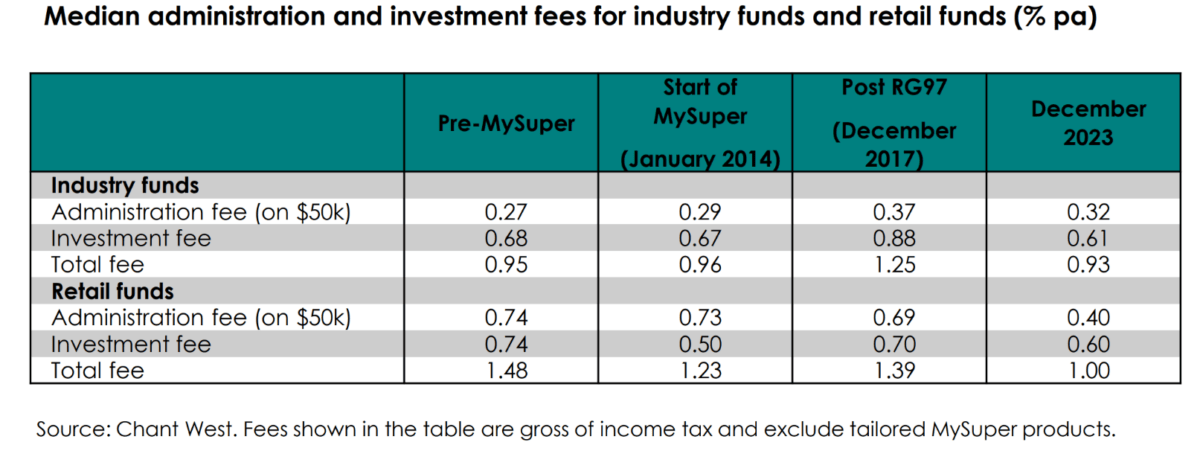

The research house says regulation has put effective pressure on funds to cut fees, with the median total fee for retail funds falling by 48 basis points in the decade since MySuper was introduced, while the median industry fund fee dropped 2 basis points.

But this means that when it comes to fees, industry funds and retail funds now have relatively little differences.

But this means that when it comes to fees, industry funds and retail funds now have relatively little differences.

Fryer told the symposium that some funds are finding new ways to make themselves look cheaper to members.

“The fee that everyone’s interested in is…the fee on $50,000 [account balance]. But a number of funds now have a much higher average balance,” he said.

“If you’ve got a much higher average balance, but everything depends on how your fee [looks] at $50,000, what you can do is actually have a higher percentage-based fee, because at $50,000 that doesn’t look like a lot, but on your average balance, it’s actually a lot more.

“So we’re seeing some funds rejigging their split between dollar-based fees and percentage-based fees.

“It’s a way that you can look cheap but still get more revenue into your fund.”

Administration and investment fees make up the bulk of the total, but Fryer warned against reducing investment fees just for the sake of it.

“At the end of the day, what puts food on the table of retirees is not low investment fees, but higher returns net of those investment fees,” he said.

“Sure, do things like co-investments and negotiate with your managers – those things are no brainers. But let’s not move away from some asset classes or some investments, which could do really well on a net-return basis but [say] we can’t touch them because they’re too expensive.”

Portfolio thinking

Nevertheless, Fryer acknowledged that it’s easier said than done for funds to combat the ‘higher the fee, lower the return’ narrative in practice. As funds feel the need to become increasingly cost-disciplined, their perspectives around portfolio construction are also changing.

Retail fund AMP Super has been going through a simplification process which saw it halve its number of fund options and external asset managers in the last four years. Head of portfolio management Stuart Eliot said the move has helped reduce some fees and costs.

Eliot said AMP Super held two asset classes that are prominently “expensive in all three ways” – that is high fees, high tracking error and considerable illiquidity – in hedge funds and private equity.

However, while AMP Super’s hedge fund exposure is on a path to zero, it is planning to hold onto the private equity exposures.

“The thing we like about private equity is it does have two to three times the expected Sharpe ratio of listed markets, so that’s a risk that we’re happy to carry given the expected benefit over the long run,” he said.

“To balance the short-term active risks from private equity, we’re in the process of increasing the allocation to what we call diversified credit. That includes everybody’s favourite of private debt, but also high-yield, securitised loans, emerging market debt – all of those kinds of things.”

Overall, Eliot said the rejigging is AMP Super relying less on skill-based sources and more on structural and fundamental return drivers. The fund is doubling the weight of index and enhanced within public equities and reserving active risks and fees for things like emerging markets and credit.

“Not only is it [more index investment] cheaper in terms of fees and active risk, but it also gives us a material pool of assets that can be directed towards securities lending, which is itself a structural return driver,” he said.

Value for member

From an industry fund perspective, REST general manager of product Scott Tully said the fund’s overarching philosophy when it comes to setting fees is whether they can be justified against the value delivered to members.

“We want to be competitive…and we do benchmark ourselves against other funds to make sure that that it’s the appropriate cost to a member,” he said.

“But as one of our board members said, it’s not about it’s not value relative to others, it’s what’s the actual value you’re giving to your members.”

REST members also have the special trait of being younger, Tully said. The fund and hospitality industry fund Hostplus together service close to half of all first-time tax file number applicants.

“Members with $50,000 worth of balance – that’s actually not representative of our fund. But it’s also not representative of other funds,” he said.

“These sort of simplistic [fee] measures – simplistic in the sense that they’re common and uniform across the industry – are okay, but you’ve also got to consider the case of some 18-year-old who joined Rest with a couple of thousand [dollars] in their super.

“What’s the value they are getting? And do the members actually perceive value in the fees they’re paying? That’s our position.”

Leave a Comment

You must be logged in to post a comment.