Decarbonisation of fixed income portfolios is a more complicated conversation than in equities for asset owners – and even more so for Australian super funds which, despite having a bigger appetite for responsible investments, cannot afford too much tracking errors thanks to the stringent guidelines of the Your Future Your Super performance test.

However, Robeco’s Netherlands-based head of fixed income, Erik van Leeuwen, argued at the Fiduciary Investors Symposium that it is quite feasible to design government and corporate bond portfolios that target a material carbon reduction without excessive impact on risk and return. The trick – like everything else in investing – is that asset owners need to be smart about it.

On sovereign risks, van Leeuwen said Robeco prefers measuring production-based emissions as it “has the least time lag and is the most precise”. But investors need to avoid “naive decarbonisation” where, for example, they merely reduce the weighting of heavy-emitting countries and increase that of the greener countries relative to a global index.

“It’s [production-based emission] obviously a metric where resource-intense countries like Australia, Canada, and US are scoring less compared to, for instance, countries like Sweden,” van Leeuwen told the symposium in Healesville.

“The simplest way [to decarbonise] would be reducing the weight in the US and increasing weight in some of the greener European countries.

“That said, you also have to look at other risk measures.”

Van Leeuwen added that the country differences could lead to longer duration, lower yield and lower credit ratings.

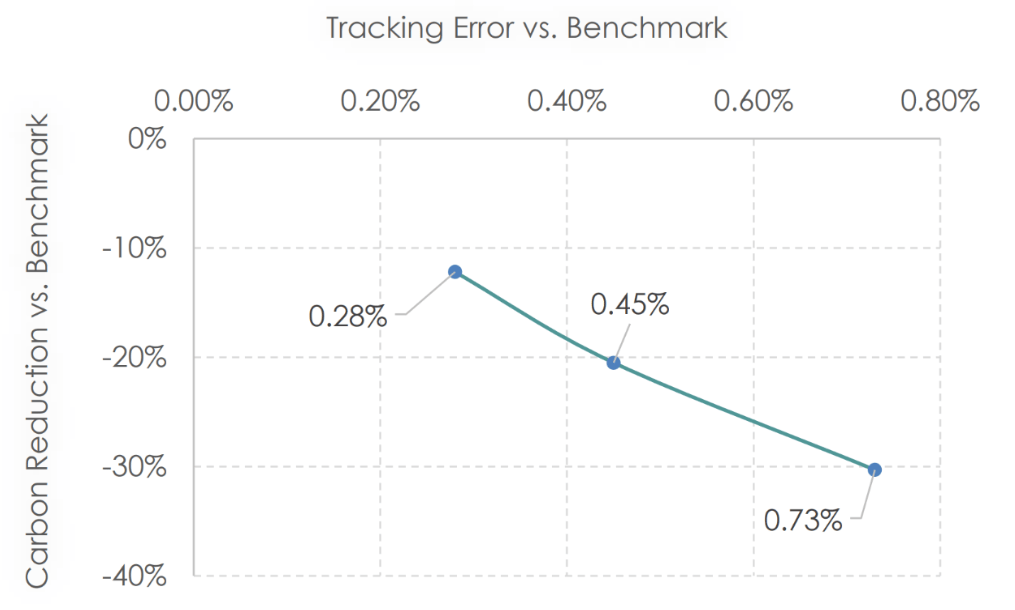

But by controlling spread risk, concentration and duration, van Leeuwen said Robeco research into an internal global index portfolio showed that a 20 per cent decarbonisation on the sovereign risk side led to a 45 basis points tracking error, over an almost 25-year period.

“If you would really go further and move to 30 or 40 per cent decarbonisation in a sovereign portfolio, then the tracking error would be really substantial,” he said.

“But 10 to 20 per cent decarbonisation in a global sovereign portfolio will still give you a good yield equal to the index with a relatively low tracking error.”

Predictions

On the corporate bond side, van Leeuwen said it has the advantage of having better data sources: there are heavy reporting duties to eventually account for scope 1, 2 and 3 emissions, and at least the former two already have somewhat standardised quality. Robeco also relies on scope 3 upstream data, which includes emissions in the supply chain of products and is believed to be more uniform than downstream data, which is emissions from the use of products.

Van Leeuwen said the asset manager has also started using forward-looking climate tools to meet some clients’ interest in investing in companies which are currently high-emitting but have a “credible” decarbonisation path.

“[We are] basically looking at sector decarbonisation pathways, which have been uniformly defined by TPI – Transition Pathway Initiative,” he said.

“It gives the guidance to all of the companies in a certain sector…and you can also identify the stronger-aligned versus the less-aligned companies in that space.”

Another area where fixed income diverges from equities on decarbonisation is the ability for investors to engage with companies. One asset owner at the symposium said it believes it has significantly more influence on portfolio companies as an equity rather than debt owner, which is why its decarbonisation efforts on the fixed income side are more of an “information gathering exercise”.

Van Leeuwen acknowledged that engagement could be complicated, especially from a sovereign angle. The asset manager started engaging with governments in Brazil and Indonesia five years ago, and is currently in talks with Australian policymakers about decarbonisation.

“It’s not something that is very effective if you do this on your own,” he said.

But on the corporate side, while fixed income investors don’t vote, van Leeuwen said they could still have some meaningful interactions with portfolio companies via credit analysis, on metrics like capex needs.

“If you’re looking at what companies are seriously making an attempt on a forward-looking basis to decarbonise, a lot of these sectors have a lot of capex needed,” he said.

“So actually, most of the debate we see between our climate strategies when they make the assessment on [whether] X is a leading or lagging company, what is the capex prediction projections they’re making, and what do they expect they need for to make that transition.

“That’s something a credit analyst will likely and with great pleasure, take along in his assessment on that [company’s] credit.”

Leave a Comment

You must be logged in to post a comment.