[vc_column]

The start of US President Trump’s second term has provided markets with an unexpectedly volatile backdrop. Investors entered the year with hopes for business-friendly deregulation and tax cuts that would lead to an uptick in deal flow. As a result, credit spreads were pushed ever lower heading into inauguration day in January 2025.

[vc_separator css=””][vc_column_text css=””]

However, these euphoric conditions quickly gave way when a blitz of executive orders and an emphasis on trade imbalances resulted in a renewed focus on tariffs. Further, the Fed paused its rate-cutting cycle, resulting in base rates remaining elevated, keeping deal flow at bay. Although the Trump administration subsequently curtailed its initial “Liberation Day” tariff projections of April 2, and after a court ruling in late May deemed them unconstitutional, headline risk nonetheless persists as market participants continue to reevaluate the effect that the ever-changing tariff saga may have on the macroeconomic environment.

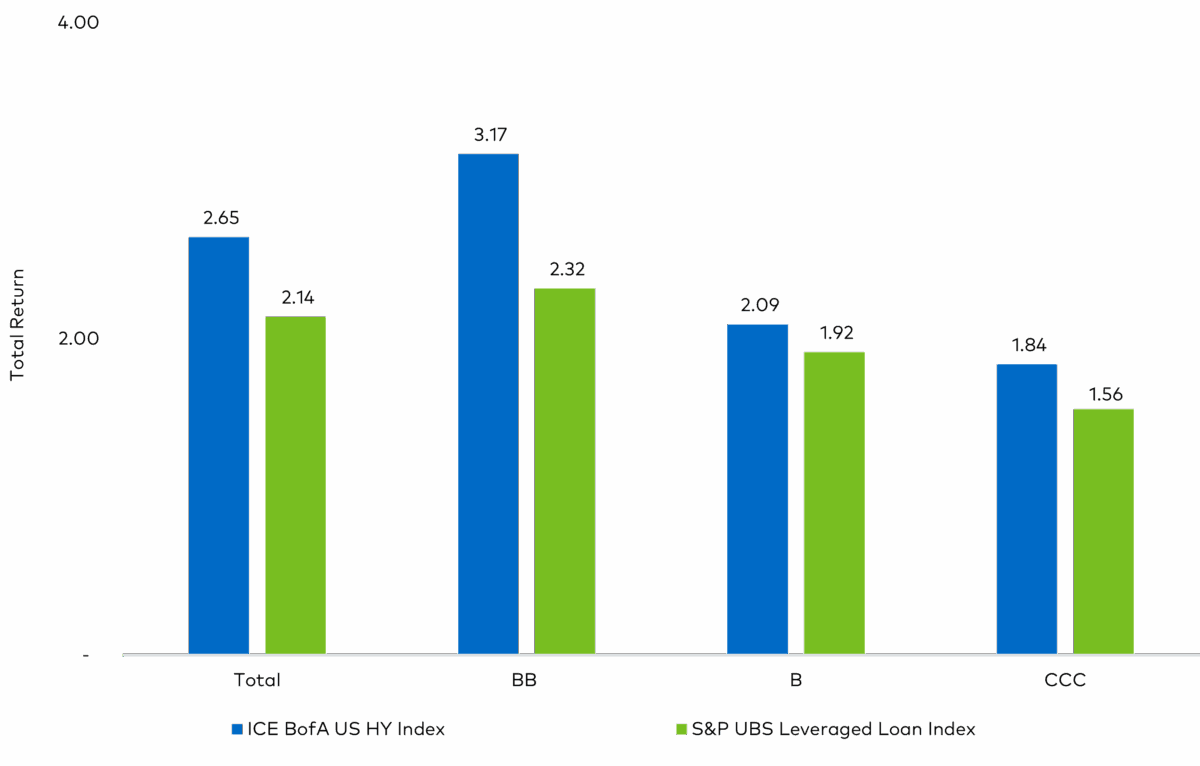

Based on the performance of the leveraged credit markets shown in Figure 1 below, if you fell asleep on New Year’s Eve and woke up on May 31, 2025, you might assume that the first five months of the year were uneventful. Without any context, Figure 1 might hint that rates have fallen further as longer-duration, BB-rated bonds are leading the way. Similarly, although returns for lower-rated credits are lagging, they do not suggest that economic activity is under significant pressure. Rather, after two years of strong returns from CCCs, one could perhaps conclude that that cohort of credits is just taking a breather while deal flow accelerates.

Figure 1. US Leveraged Credit Market, 2025 YTD Performance – High Yield Bonds and Leveraged Loans, Total Returns

Source: ICE and S&P UBS as of May 31, 2025

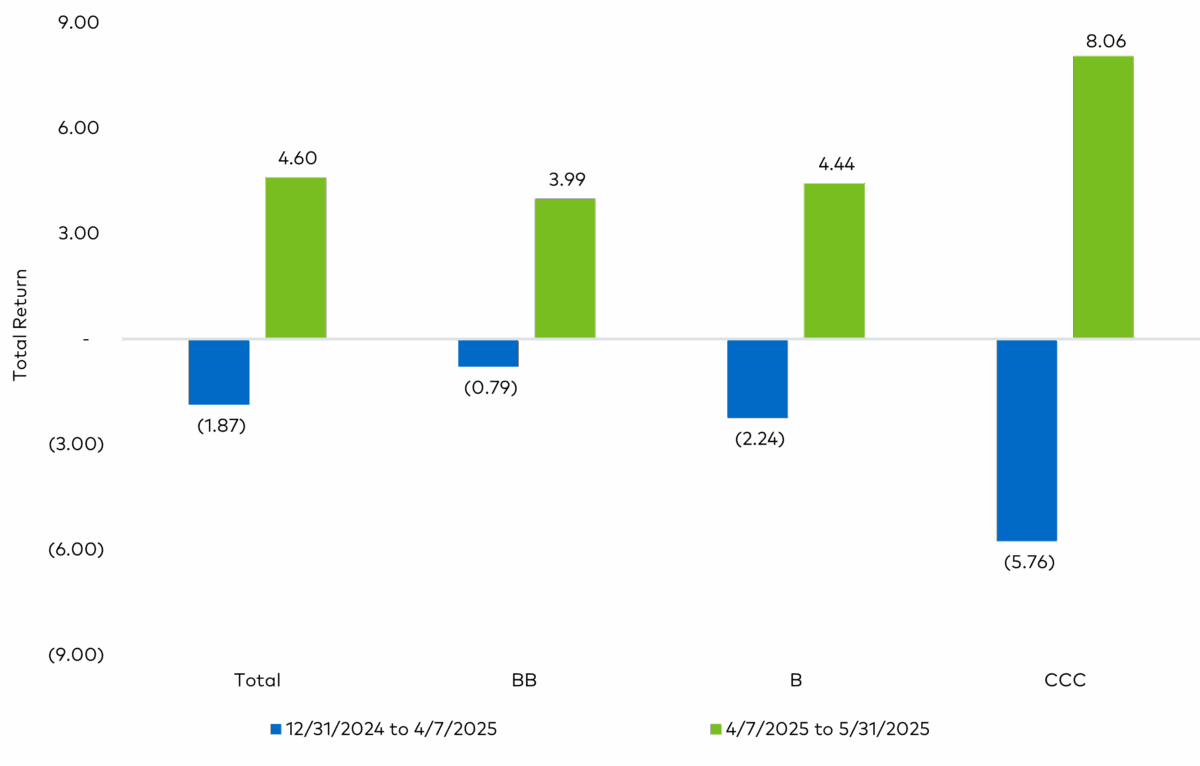

However, as we sit here today, we know that this particular fact pattern did not play out. Deal flow has been muted, and performance in the leveraged credit markets was anything but uneventful. As Figure 2 below shows, during the height of tariff turmoil, high yield bonds produced negative returns, with CCCs in particular coming under significant pressure. Moreover, those sectors most susceptible to both tariffs and a slowdown in economic activity, such as the Energy, Transportation, and Retail sectors, were hit hard by the uncertainty created by the tariff announcements. However, since that time, even those most challenged sectors were able to generate gains for the period on the back of the tariff rollback rally. Further, the Trump administration’s announcement of 90-day tariff pauses on April 9, 2025, gave high yield bonds a welcomed reprieve, and since the immediate aftermath of Liberation Day, the high yield market has enjoyed a healthy rebound.

Figure 2. Tariff Turmoil: 2025 YTD Performance Breakdown, US High Yield Bonds

Source: ICE, ICE BofA US High Yield Index as of May 31, 2025

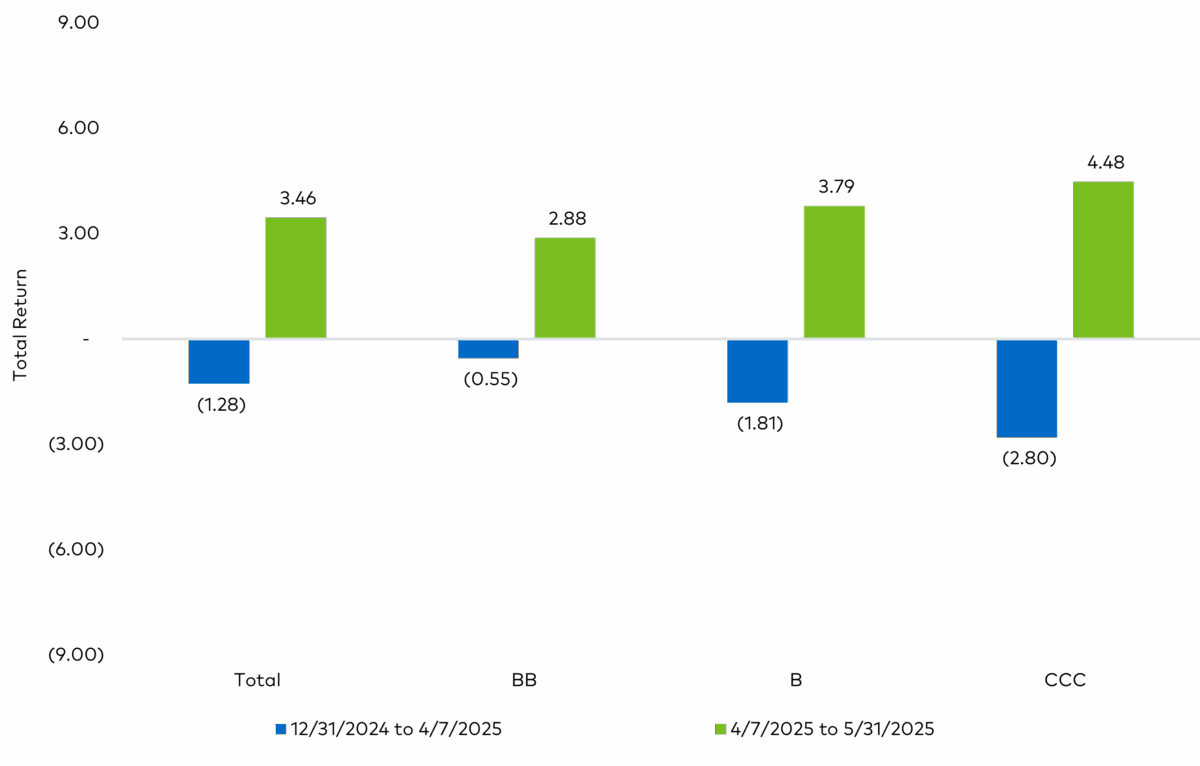

The leveraged loan market saw a similar pattern in performance as it too grappled with the macroeconomic ramifications of the seismic shift in trade policy, as reflected in Figure 3. Aided by higher coupons and a lower sensitivity to swift price moves driven by risk-off market sentiment, loans outperformed their fixed rated peers during the sell-off but lagged during the recovery. Further, like high yield bonds, those sectors most sensitive to tariffs and a slowdown in economic activity were the weakest performers. Although most of those sectors staged a recovery through May, the Chemicals sector stood out as the only sector still generating a loss for the year. That said, like their fixed rate peers, leveraged loan performance recovered much of what was lost following Liberation Day.

Figure 3. Tariff Turmoil: 2025 YTD Performance Breakdown, US Leveraged Loans

Source: S&P UBS, S&P UBS Leveraged Loan Index as of May 31, 2025

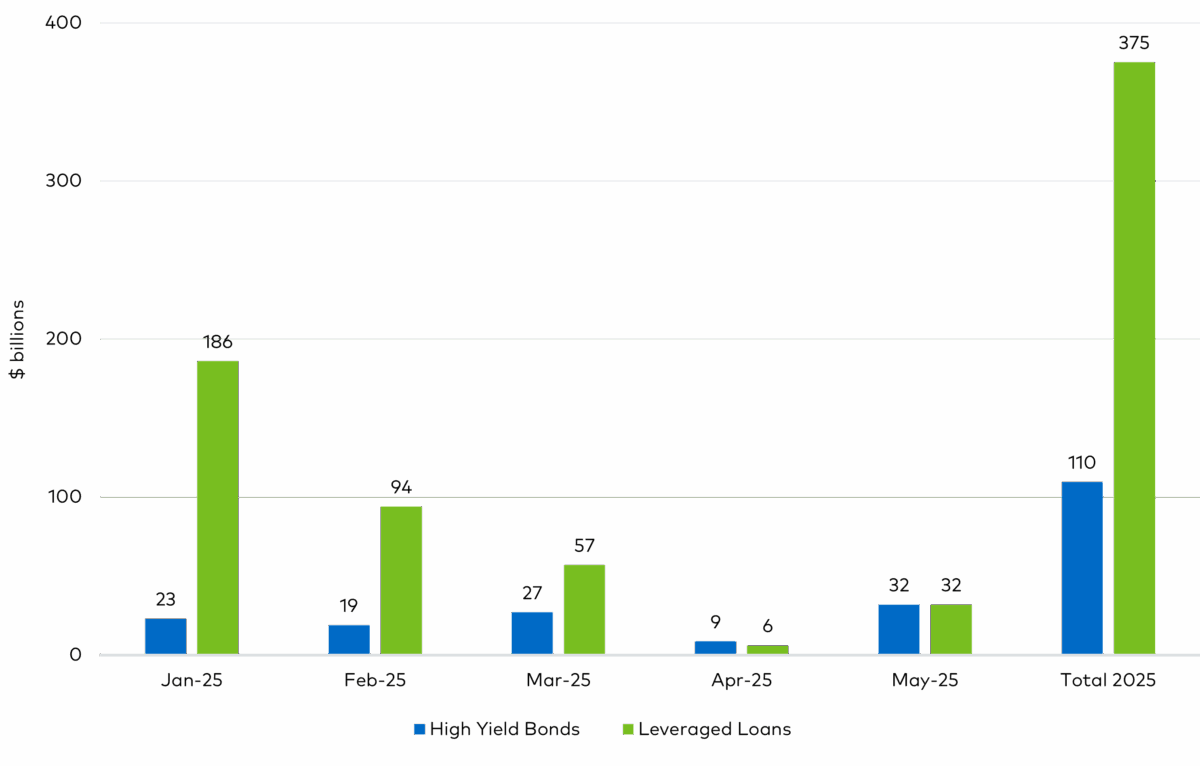

These volatile conditions have done little to engender confidence among leveraged credit issuers. As a result, deal flow, which had begun the year at a healthy pace, petered out in April before staging a slight comeback in May (Figure 4). That said, even pre-Liberation Day primary market activity was dominated by refinancing and repricing activity. Although more recent activity has been slated for leveraging transactions, like M&A and dividend deals, the dearth of new debt supply experienced over the last several years continues.

Figure 4. Primary Market Activity, US High Yield Bonds and Leveraged Loans, 2025 YTD

Source: J.P. Morgan, as of May 31, 2025

In addition, defaults remain contained. According to data from J.P. Morgan, as of this writing, the par-weighted high yield bond default rate sits at 0.43 per cent, while for loans, the par-weighted default rate is 1.42 per cent. Including distressed exchanges, those rates increase to 1.33 per cent and 3.62 per cent, respectively. That said, in April, J.P. Morgan revised their default forecast higher for the remainder of 2025 as well as for 2026, based in part on their assumption that the US will enter a recession in the second half of 2025. The new projections see high yield bond defaults at 1.50 per cent and 2.75 per cent, respectively, while loans are projected to reach 3.25 per cent and 4.75 per cent, respectively.

Those projections exclude liability management exercises (“LMEs”), which have been a primary driver of higher default rates for the past several years, especially among loans. Given elevated rates, looser covenants, and weaker fundamentals, these “soft” defaults have been a way for issuers to extend runway and provide liquidity to bridge a soft patch in earnings. This LME activity is responsible for driving a wedge between high yield and leveraged loans defaults not seen in more than 25 years (Figure 5).

Figure 5. Difference in Default Rates: US High Yield Bonds vs. Leveraged Loans (Including LMEs)

Source: J.P. Morgan, as of May 31, 2025

To date, this activity, a byproduct largely of looser covenants that have weakened creditor protections, has allowed issuers to delay negotiations with creditors, which often results in an erosion of the issuer’s enterprise value and lowers recovery rates. Unfortunately, this activity seems here to stay for now and highlights the need for debt investors to consider many scenarios under which their investment may be at risk beyond a traditional default.

Shifting attention to our outlook for the remainder of the year, we expect continued volatility, driven largely by geopolitical risks. If anything seems true in today’s environment, it is the inherent difficulty of forecasting and providing an outlook. Few prognosticators would have predicted the scope of the tariff announcements on April 2, 2025, and the effect they had on markets.

Even safe haven investments like US Treasuries were not immune. With Moody’s recent downgrade of the United States credit rating, there are no longer any ratings agencies that think the probability of a default by the United States government on its debt is zero.

We do not envy ratings agencies, nor do we take their opinion at face value. We would like to believe that others share the same opinion, but after almost 30 years of investing in underfollowed areas of below investment grade credit markets, the stigma associated with certain ratings is tough to shake.

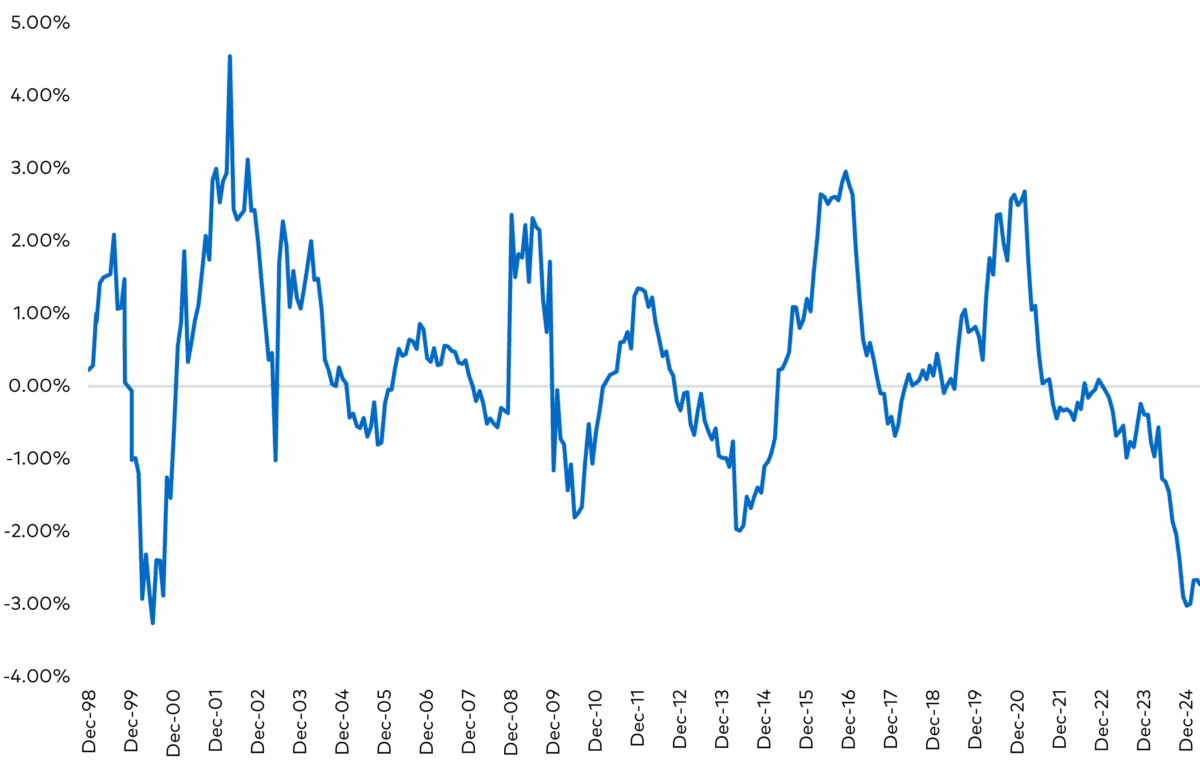

Figure 6. High Yield Bonds: Option Adjusted Spreads (“OAS”), ICE BofA US High Yield Index and Sub-Indices by Credit Quality Rating

Source: ICE, as of May 31, 2025

Turning to the recent moves in US high yield bonds, the market seemed indifferent to Moody’s downgrade of the US credit rating. Instead, from the data in Figure 6 above, we see the ICE BofA of US High Yield Index option adjusted spread (“OAS”) responded swiftly to the shift in global trade policy. However, given that most US high yield issuers operate domestically focused businesses, the high yield market is generally more insulated from the first-order effects from tariffs. Rather, it was the potential impact of tariffs on overall economic activity that weighed more heavily on high yield bonds. This concern can be seen in Figure 6 in the move in spreads among the lowest-rated high yield bonds.

While the announcement of “pauses” in reciprocal tariffs was well received, high yield bond market spreads remain wide of recent lows. Further, the May 2025 decision by the US Court of International Trade to block the tariffs imposed by the Trump administration provided another respite for markets. Although the administration’s subsequent appeal and the stay granted by the US Court of Appeals leaves markets in a continued state of flux regarding the imposition of widespread tariffs.

The same is true in the leveraged loan market. Although April’s widening did create some buying opportunities, treading lightly is warranted. As we have seen, tariff headlines shift quickly, and details on trade deals remain very limited. While we believe that trade deals will be consummated in a mutually beneficial manner with the end of the 90-day pause approaching and the uncertainty created by recent rulings, we could see more “fireworks” ahead of the US Independence Day on July 4th if deals cannot be reached.

While we believe that trade deals will be consummated in a mutually beneficial manner with the end of the 90-day pause approaching and the uncertainty created by recent rulings, we could see more “fireworks” ahead of the US Independence Day on July 4th if deals cannot be reached.

The tariff announcements by the Trump administration led many market participants to adjust their outlook for economic growth lower, and in many cases, the likelihood of a recession in the second half of 2025 seemed pegged as a foregone conclusion. We cannot say for certain that recession is imminent, though as of this writing, markets are acting as if such an outcome is unlikely. For now, company fundamentals have proven resilient. Inflation has come down, even if it remains above the Fed’s target, and unemployment is low, but consumers seem weary.

We cannot say for certain that recession is imminent, though as of this writing, markets are acting as if such an outcome is unlikely. For now, company fundamentals have proven resilient.

On top of this, we have potential deficit and inflationary pressures from the “One Big Beautiful Bill Act” recently passed by the US House of Representatives. Whether these pressures come to be is anyone’s guess, as the bill remains subject to approval by the US Senate, but for now, there appears to be enough uncertainty to keep the Fed from acting. While President Trump said he will not remove Chairman Powell ahead of the end of his term, the President’s repeated calls for rate cuts seem counterproductive. The Fed’s desire to remain apolitical leaves it in a difficult position, particularly since delivering a rate cut following extreme political pressure would likely be viewed as anything but apolitical. However, if the economy suffers a setback and the Fed is slow to loosen monetary policy in response, due to a desire to appear apolitical or otherwise, it could exacerbate the situation. Such a monetary policy mistake has been on our list of potential risks for markets, and in our opinion, that risk has only grown in the weeks since Liberation Day.

Not surprisingly, this turbulent climate has not been conducive to private equity realizations. At the start of the year, we thought that a revival in M&A activity stemming from a more favorable regulatory environment, as well as lower yields in the leveraged credit markets, would drive new deal flow. However, that scenario has not unfolded. Be that as it may, the need for private equity sponsors to divest from their portfolio investments remains. We have not dismissed this outcome, but until conditions improve, M&A activity may remain subdued. Nonetheless, as capital markets thawed following the shock of the initial Liberation Day announcement, an increasing number of dividend deals have provided private equity sponsors, and as a result, their LPs, with some liquidity.

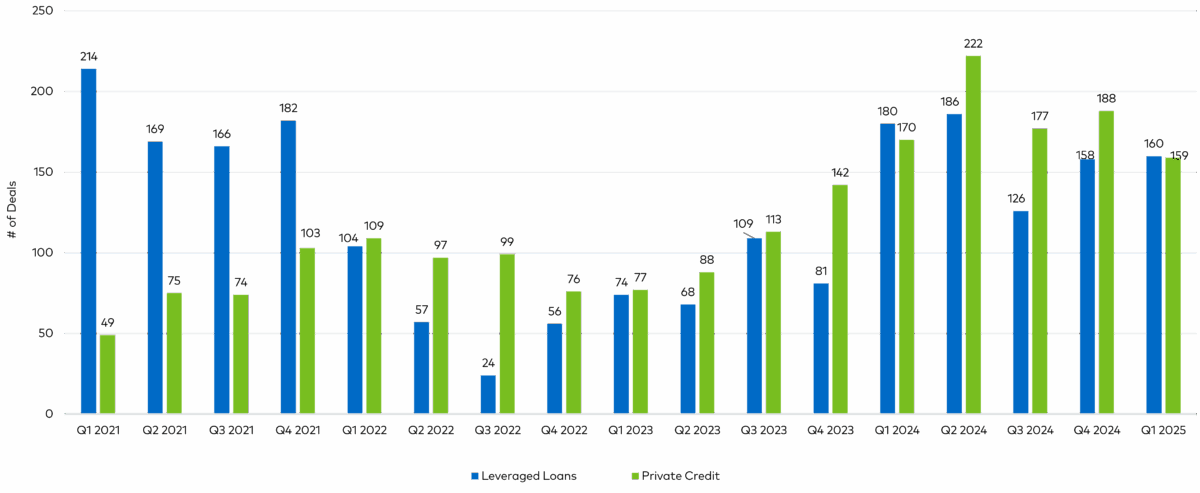

The shortage of deals is not all bad, as the lack of new supply, when combined with the strong demand for yield, has resulted in a positive technical bid for leveraged credit markets, resulting in higher prices. However, this outcome is also the primary driver of the market’s insatiable appetite to refinance and reprice existing debt, thus driving spreads lower. This lower-spread environment has extended to private markets. Direct lending deals continue to come to market at lower spreads as they carry on competing with the leveraged loan market for deal flow (Figure 7).

Figure 7. Count of Non-LBO Deals Financed, Leveraged Loan Market vs. Private Credit, 2021-Q1 2025

Source: Pitchbook, as of March 31, 2025

Recent volatility notwithstanding, high yield bonds continue to offer attractive all-in yields. As of May 31, 2025, the yield to worst on the ICE BofA US High Yield Index stood at 7.53 per cent, 80 bps higher than the 10-year average. With an average dollar price of approximately US$95 ($146), coupled with strong issuer fundamentals, we believe that high yield continues to offer a compelling entry point for investors. Similarly, leveraged loans, as measured by the S&P UBS Leveraged Loan Index, are providing investors with elevated yields relative to history. At the end of May, the yield to three-year takeout stood at 8.30 per cent, more than 100 bps higher than the 10-year average. While leveraged loan issuers have experienced more challenging fundamentals as compared with issuers of high yield bonds, the prospects for an active manager like Polen Capital to identify attractive risk-reward opportunities in today’s environment remain.

In our experience, today’s environment is just part of the natural fluctuations of the credit cycle. What is most interesting to us is that periods of increased volatility often present significant opportunities. Active investment managers can exploit sell-offs in the market to identify and invest in solid credits that provide superior yields to the broader high yield market, while taking advantage of market strength to sell credits where relative value has been realized. Maintaining discipline in the face of market ebbs and flows enables astute investors to seize opportunities where perceived risks may be exaggerated by current volatility, leading to attractive risk-adjusted returns in the long term.

David Breazzano is head of team for credit at Polen Capital, where he serves as co-portfolio manager of the US Opportunistic High Yield and US High Yield strategies.

Leave a Comment

You must be logged in to post a comment.