Regulatory assessment of super fund’s retirement income strategies (RIS) is a near certainty. It is also essential for super funds to self-assess their RIS through the lens of continual improvement.

All the breadcrumbs lead to regulatory assessment of RIS. APRA has recently started publishing performance for account-based pensions (ABPs) and is considering what other data needs to be collected and shared. Meanwhile various groups, including SCA and SMC are calling for the Your Future Your Super (YFYS) performance test to be extended to account-based pensions. The challenge is what form regulatory assessment should take to motivate good outcomes without creating adverse unintended consequences.

Pleasingly, we have seen some super funds developing assessment metrics, mainly based around measuring member retirement-related activities. Generally more uplift is required.

Given the current state, slow progress by many super funds and the risk that it ends up taking ten years for industry to have high-quality RIS in place, more holistic assessment of super fund RIS must come. But what form might RIS assessment take? We see a role for a balanced approach that draws on a range of inputs but with capabilities assessment as the foundation.

A conundrum created by horizon mismatch

In 2022, the Conexus Institute published a thought piece titled Assessing retirement income strategies… when outcomes are but a promise. The underlying thesis was that retirement is difficult to assess as outcomes are delivered well into the future, largely in the form of an income stream. Yet RIS assessment needs to be based around what is observable today, giving that waiting to see the outcomes is simply not feasible.

Accordingly, we argued that it becomes necessary to focus on the effectiveness by which super fund trustees are assisting their retired members to achieve their retirement goals. But how?

Four approaches

Conceptually there are four broad approaches to gauging whether super funds are effectively assisting members with their retirement needs:

1. Measure outcomes, i.e. the outputs – The three objectives under the Retirement Income Covenant are (a) maximising expected income, (b) managing risk to expected income, and (c) providing flexible access to funds. Outcomes under these objectives are not only potentially delivered over decades, but are also partly a function of decisions made by members themselves. While it may be possible to measure investment performance, this is but one determinant of outcomes alongside the presence of other income sources and drawdown choices. It also glosses over provision of flexible access to funds; and the help, guidance and advice services made available to assist members with retirement. Capacity to measure outcomes is largely infeasible or at best extremely limited.

2. Examine member activity – Gauging whether trustees are effectively assisting members by observing member activity is more feasible. It may take the form of observing actions and surveying members. For example, the percentage of members who adopt more efficient drawdown strategies and retirement solutions, or make use of guidance and advice services, can provide useful insights on whether a RIS is working as intended. Surveys can reveal responses to the fund’s retirement offerings or retirement confidence. While we support the industry assessing member activity, we question whether this suffices. In particular, it says little about the quality and scope of the offerings being presented to members.

3. Modelling expected outcomes – This entails projecting potential retirement outcomes and assessing them against objectives. (See our June 2023 thought piece How to Approach Quantitative Assessment of Retirement Income Strategies for an example). This approach suffers from the need to make subjective assumptions and being difficult to implement, especially given the complexity of defining and trading off various retirement objectives.

4. Evaluate capabilities, i.e. the inputs – A fourth alternative is to focus on the range of capabilities that trustees have developed to deliver a RIS. This would entail evaluating the scope and quality of those capabilities in order to assess the current status and identify gaps, thus supporting ongoing improvement. While this approach does not measure outcomes directly, it can speak to how well-positioned a super fund is to assist retired members to best achieve their retirement goals.

We see a role for all approaches. Nevertheless, we consider that evaluation of capabilities should sit at the foundation as it can provide a comprehensive assessment.

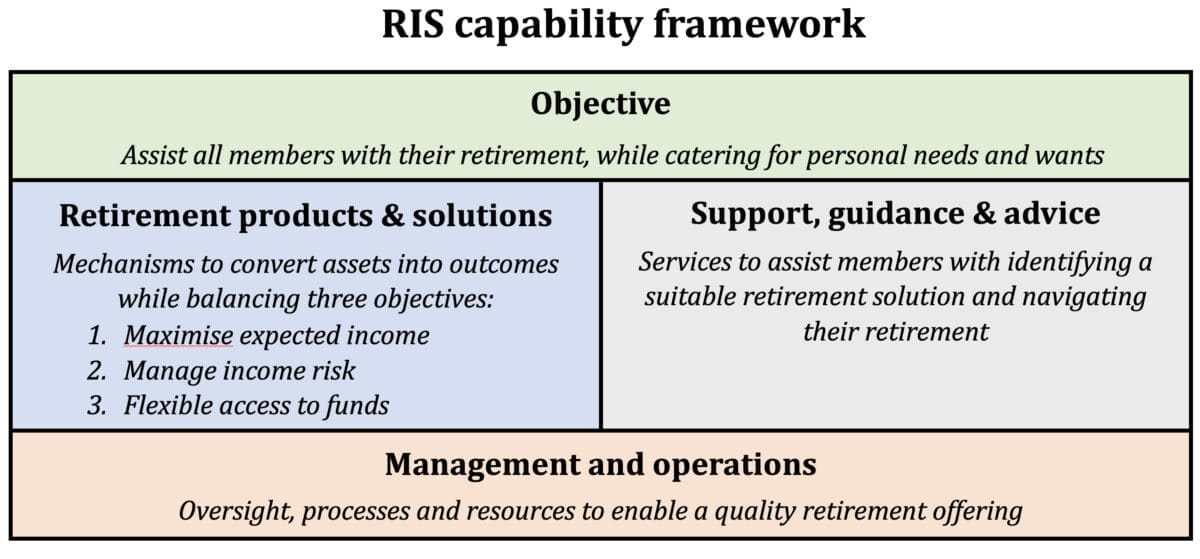

RIS capability framework

Our short thought piece sets out our vision for an “RIS capabilities framework”, for which we are seeking feedback. The framework is based around identifying the set of offerings and activities required for a super fund to deliver a high-quality RIS that caters for members with differing needs. It may be operationalised through a checklist of items that trustees should be addressing in developing their RIS, i.e. a “to-do” list.

The figure below, taken from the thought piece, describes the broad structure based around three components that are in turn fleshed out via a checklist:

1. Retirement products and solution offerings – These are the mechanisms provided to members to support conversion of assets into regular income and other retirement outcomes, which may include access to funds for spending needs not covered by regular income. The ultimate aim is to have the capability to deliver integrated retirement solutions where assets are allocated to various products from which income is generated that cater for key member differences.

2. Support, guidance and advice offerings – These are the set of services provided to members to assist them towards a retirement solution that is suitable for their needs and navigate their way through retirement.

3. Operational support – The retirement offering needs to be underpinned by a range of business resources and processes. This component covers aspects such as governance, staffing, systems, management of risk and suppliers, and a review and improvement process.

Evaluation against the checklist would depend on purpose for conducting any assessment, and is likely to evolve over time as the industry develops its retirement offerings. Some kind of subjective grading is probably necessary. Our thought piece floats the idea of grading capability under each checklist item as either “undeveloped”, “basic”, “highly-developed”’ or “best-practice”. All super funds should aspire to move up through the grades, with the bottom two grades a clear signal that more needs to be done.

A capabilities framework has many potential uses

Specifying a checklist of capabilities required to deliver a quality RIS can provide a foundation for building out Australia’s retirement system in a number of ways:

• Supporting self-assessment by super fund trustees.

• Furthering RIS development by highlighting capability gaps for trustees to address.

• Supporting regulators in scoping out the capabilities they expect super funds to develop. These might initially be included in regulatory guidance if not regulatory standards, and could potentially form the basis of a regulatory assessment regime.

• Establishing a framework for use by observers such as industry research houses, asset consultants and financial planning groups.

• From a policy perspective, a basic set of capabilities might provide the basis for licensing conditions under a retirement licensing regime as proposed by The Conexus institute or a “best-in-show” list as proposed by the Grattan Institute. It could supplement the best practice principles for retirement being considered by Treasury.

Next steps along the assessment pathway

RIS assessment will become an increasingly important feature of a developing retirement system. Further, some form of regulatory assessment seems almost certain, with the challenge being how to frame it to address the complexity of retirement and motivate good outcomes while avoiding adverse unintended consequences.

Given the large and diverse number of criteria required for a quality RIS, we think multiple assessment frames will be required. Assessing outcomes where measurable, examining member activity, outcomes modelling and evaluating capabilities in combination can create a rich perspective.

Of many examples, the YFYS test is probably the most prominent case study of assessment driving a range of industry behaviours, not all of which align with best member outcomes. This highlights the importance of developing a well-framed RIS assessment framework at a regulatory and industry level, with capabilities at the foundation.

Leave a Comment

You must be logged in to post a comment.