Someone who retires with twice as much saved as someone else should expect that income to last at least twice as long. That simple insight belies a complex problem in the system: namely, how to engage with members to help them make active investment choices earlier in life.

New research highlights a yawning gulf between the final balances of members who actively choose their investment strategy and those who remain in default MySuper options. Australians who make investment choices earlier in life experience significantly better outcomes in retirement because they accumulate more. Often a lot more.

“People in choice products have a higher balance, but I don’t think they understand the magnitude,” says Duncan McPherson, principal of Borromean Consulting and author of a report, The Power of the Active Member: Why engagement – and not just investment returns – is the real driver of retirement success.

McPherson, who was chief executive officer of Link Advice prior to its acquisition by MUFG and is a former senior advice executive with MLC, argues that making an active investment choice is a proxy for member engagement, but caution is needed in interpreting the link. It may be that engagement is driven by factors such as higher account balance to begin with; or engaged members might already be receiving advice.

“What I am pointing to is a correlation – positive, and strong – between active investment choice and broader member engagement,” he says.

“While I can’t attribute causation, members who make an active investment choice are demonstrating a level of awareness, interest and confidence in their super that appears to translate into better outcomes over time.”

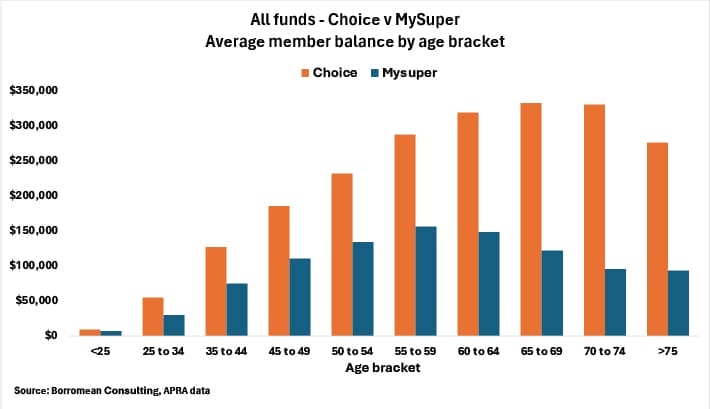

McPherson’s research suggests that members aged 60 to 65 who have made active investment choices have an average account balance of $318,000 compared to people the same age in default MySuper accounts, who have an average account balance of $148,000.

Compounding

The story is replicated to varying degrees across age bands. McPherson says choice investment options have on average outperformed MySuper options by about 2.5 per cent a year over the past five years. Compounded over decades, the difference is material.

Simplistically, an individual who arrives at retirement with $300,000 compared to a member who gets there with $150,000 will – assuming each receives the same income each year – see their money last more than twice as long.

Or to look at it another way, one member could draw down twice as much as the other over the same period.

“If we’re looking for Australians to have a dignified retirement, and we believe in the power of compounding, then we’ve really got to start helping people engage more, to make simple, active decisions,” McPherson says.

“If we’re looking for Australians to have a dignified retirement, and we believe in the power of compounding, then we’ve really got to start helping people engage more, to make simple, active decisions,” McPherson says.

However, a majority of members aren’t equipped to make investment choices on their own, even if the idea occurs to them in the first place. In addition, McPherson’s analysis suggests fund members typically do not engage with super and make active investment choices until they’re into their 50s, meaning they miss out on the full benefits of long-term compounding.

Therein lies the challenge for super funds: how to engage a younger cohort of typically disengaged members, in a way that provides them with the tools they need to make effective choices. McPherson says the research points to a clear conclusion: empowerment, rather than education.

“There’s a lot of education material – ‘watch this video’ – but people don’t want to be educated,” he says. And it’s also not true that funds can’t do more to empower members without legislative change to support it.

“I’m very reluctant to point the finger at legislation being the innovator,” he says.

“There is still a lot of lot of inertia by funds out there saying we’re waiting on DBFO, and I am actually not convinced of what that will do for them.

“Funds need to change their message in order to move it into enablement. Messaging, I think is consequence messaging, shorter messaging.”

A lot going on

Younger members have a lot going on: careers, families, buying a home, paying off other debts. They don’t have the time or the inclination to essentially study superannuation.

Instead, he recommends focusing on “consequence messaging”: shorter, sharper, communication that clearly links actions to outcomes.

“The consequence of you making investment choices is you’ll end up with more money at retirement,” he says.

He stresses that this is not about asking members to contribute more to super at a time when their other financial commitments are peaking but is simply about making active choices about the contributions they do make.

McPherson says there’s evidence that the best engagement approach is digital.

“Funds need to invest in website and digital tools and scale the services,” he says, and he notes that some retail and smaller funds – those labelled in Borromean analysis as “empower enablers” – have high choice-participation rates precisely because they have invested in proactive, digital-first engagement. Big funds (those with a million members or more) tend to lag.

A core finding of McPherson’s analysis is that many funds misallocate member engagement spending, favouring reactive over proactive services.

“Proactive servicing is website, digital tools, education, data analysis. Reactive is essentially a contact centre,” he says.

“The average not-for-profit fund is spending just over $11 per member on contact centres and just under $7 on websites and digital tools.

“All the funds I’ve spoken to over the years want to move contact centres from reactive to being value-based, when people have got hardship calls or [insurance] claims or they retire and they call the contact centre [and] for everything else they got to a website. But in order for people to go to the website, they need to invest in the website and digital tools and scale the services, and I’m not seeing that.”

Leave a Comment

You must be logged in to post a comment.