This article originally appeared in the print edition of Retirement Magazine Vol. 2

All of the heat and energy in retirement policy has been focused on financial advice, with the long-awaited Delivering Better Financial Outcomes (DBFO) legislation and, to a lesser extent, Treasury’s development of the Retirement Best Practice Principles for super funds. While advice and system design have a place, people who want to take more of a DIY approach to retirement planning are being let down.

If DBFO is enacted, super funds will be unshackled from their self-imposed barriers and start giving more advice and start asking questions about what members really want. Some funds have realised that no true barriers exist and have already forged ahead.

The changes might result in more consumers transitioning their savings to the retirement phase earlier, and some may further optimise their drawdown patterns. But given the significant tax incentives to stick to the minimum drawdowns and the super fund-imposed barriers to transitioning to retirement (for example, minimum balance requirements), we fear the actual outcomes from the past five years of retirement focus will be far more muted.

The new class of “advisers”, employed by funds and with limited training, should help funds retain members at retirement. But it remains to be seen whether they’ll deliver any actual value. We highlighted guidance failures by super fund calculators in this publication last year, finding that most fund calculators either encouraged people to spend down at artificially high levels or had them spread their savings thin to last beyond 100. If the quality of this guidance is anything to go by, we’re in for a rocky few years.

The conversation on retirement reform has been completely devoid of discussion about how we make super funds compete with each other to deliver the best outcomes for retirees.

A ‘black spot’ in the drive for competition

We have a market with plenty of potential competitors, relatively low barriers to entry for funds and investment options (perhaps too low in the recent cases related to the Shield and First Guardian failures) and all Australians are forced to contribute, so there is no lack of demand. The biggest “black spot” is comparability. There are thousands of product choices but no real way for the average person to independently understand their needs and compare what’s on offer.

It’s embarrassing that we have built a $4.1 trillion superannuation system without providing even basic information for consumers to compare retirement options. We’re even lagging New Zealand which, despite the infancy of its super system, has an independent consumer-facing comparison tool to help people wade through the morass of investment options. It includes clear information about fees, returns, customer service experience and risk (note 1).

Australia needs urgent action to increase consumer-facing transparency of retirement options. At the moment we’ve got a comparison tool that only compares a fraction of the accumulation market, which is siloed away on the ATO website. This tool has not been expanded or updated to improve its usefulness for consumers. Instead, its only minor change came after heavy industry lobbying, which saw it move from being sorted by fees to being sorted by returns – despite consumer research showing that people are far more responsive and more likely to consider switching based on fees. We can already hear the clamour of voices pointing out that net returns are the best measure of outcomes. Sure, in hindsight; but unlike its NZ equivalent, the Australian tool doesn’t even attempt to communicate risk. Once again, industry interests are put ahead of consumers, even on tools that are meant to be designed for consumers.

We test the performance of accumulation products, why not drawdown products?

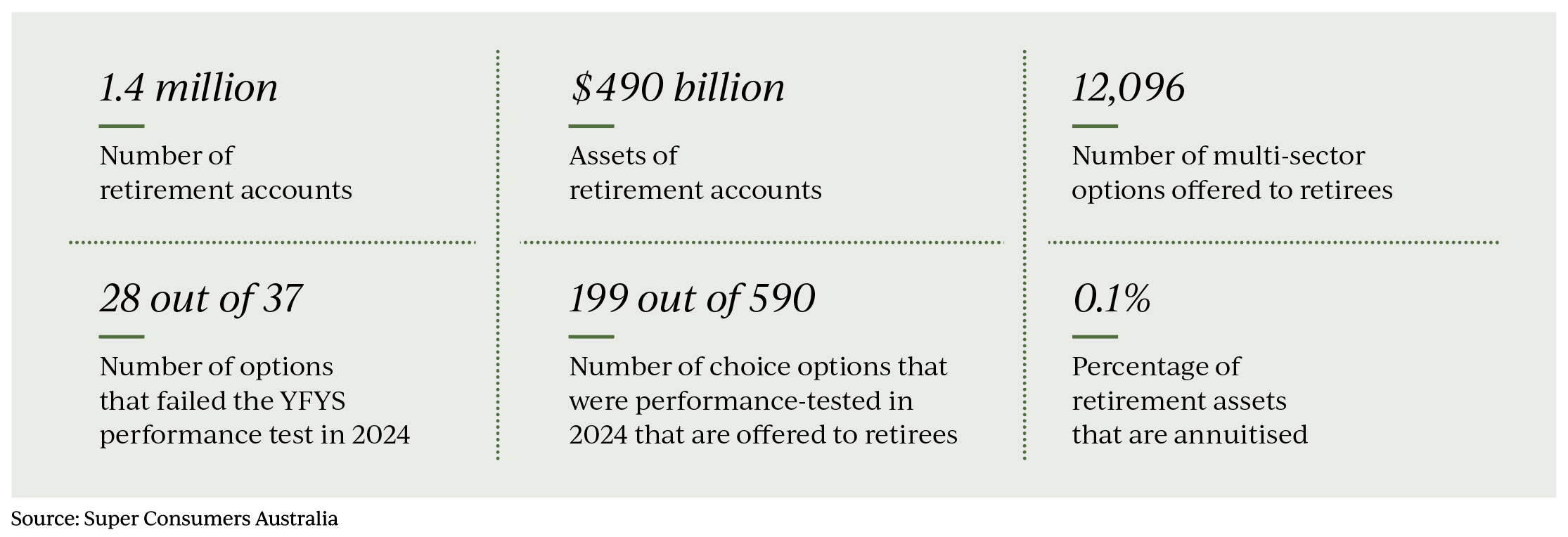

The retirement phase of superannuation is big and will continue to grow. There are currently 1.35 million accounts with $490 billion in assets in the retirement phase of APRA-regulated superannuation funds (note 2). APRA estimated that we are tracking towards $3 trillion in the retirement phase in the next 20 years (note 3). With more than 200,000 new pension accounts opened every year since 2015, an increasingly large group of the population is lacking transparency about their choices (note 4).

There are currently 67 funds offering 215 retirement products with 12,096 multi-sector investment options (note 5). With this dizzying array of options to choose from, consumers cannot simply gather information themselves to do a comparison of retirement options. We need a comparison tool that provides people with easy-to-use relevant information so that they are empowered to find the best retirement option for them.

In June 2025 APRA released data for the first time on the historical returns and fees of some multi-manager multi-sector retirement investment options that underpin account-based pensions Note 6). This is an important first step in increasing transparency but it is a long way from providing data in an easy-to-use consumer facing comparison tool.

We have analysed this new data and it does appear that some retirement drawdown products may be harmful to consumers. But consumers are not getting any warning that they are invested in poor quality products.

Of the 37 accumulation investment options that failed the 2024 performance test, 28 are offered in the retirement-phase. APRA published 10 years of historical data on eight of these. When compared with other retirement phase options with similar growth/defensive weightings, these failed options consistently perform in the lowest quartile of their category (note 7).

This suggests that these investment options are not only harmful to the accumulation members who are warned about them, but that they are also poor performers when compared to retirement options and potentially harming retirees as well.

We need to stop this harm immediately.

Inclusion in the performance test

At this point in time, the main retirement options are account-based pensions, which are straightforward investment options with a return and a fee. They may have investments more tilted towards income generation than accumulation phase options, given that the investors will be drawing down some of their money each year, but overall they are very similar, if not identical, to

accumulation-phase investment options. In fact, 199 of the 590 choice options tested in the 2024 performance test are offered in the retirement phase (note 8).

All multi-manager multi-sector retirement drawdown investment options could be included in the annual performance test immediately. This would cover 52 per cent of the retirement assets and would directly reduce harm to people invested in poorly performing retirement options (note 9).

For retirement drawdown products with a guarantee (for example, traditional annuities, market-linked annuities) the current performance test could simply not be used. There are 5530 member accounts with $464 million (0.1 per cent of the $490 billion in retirement assets) in retirement drawdown products with guarantees available at the moment (note 10). We shouldn’t hold up performance testing of account-based pensions simply because we haven’t figured out how to test this 0.1 per cent.

Even so, for these annuity-style options, consumers would benefit from having a standardised measure of the retirement income payable from each option, plus the out-of-pocket fees. For example, it would be useful to compare the income that a 60-, 70- or 80-year-old male and female could generate for $100,000 invested in a lifetime income product.

There could be some simple categories used to group lifetime income products, such as market-linked/non-market-linked, term/lifetime guarantee, reversionary/non-reversionary and immediate/deferred. This would enable people to judge which products in a category would be the best for them, given the income provided and out-of-pocket fees charged. The government could also set a quality benchmark of income/fees that it deems is acceptable performance of a lifetime income product and assess which lifetime income products pass or fail that benchmark.

The government should expand the YourSuper Comparison Tool to provide standardised information on retirement products (returns or income per $100,000, fees, risk and pass/fail mark). This would put the key information in one easy to use spot for people to compare retirement products.

In addition to transparency for comparison, and quality testing to identify harmful products, the consequences for trustees should be extended to poor performing retirement drawdown options. This ensures that trustees will be motivated to improve and ensure that they offer products that meet the minimum quality standards set by the government. Even without expanding the performance test, the government could require that the letter that is currently sent to members of a failing trustee-directed product is sent to any superannuation investor (accumulation, retirement or transition to retirement phase) who is in that option in any fund.

Other measurement

Although our focus is on providing transparent measurement of quality for consumers, it is also important that trustees have robust internal measurement of the success of their retirement drawdown options and that regulators have metrics that measure the overall status of the retirement drawdown phase.

Interesting ideas on trustee self-measurement of success are provided in the paper by David Bell and Geoff Warren (note 11). What is measured matters, and all trustees should be using metrics that measure how well their retirement drawdown products are being used by members, how competitive their offerings are and whether all members are benefiting from the offerings or if there are differences across cohorts of members. These insights would help to shape continuous product improvement and development of new products for members with unmet needs.

The Treasury consultation package on a Retirement Reporting Framework is also an important step towards greater transparency on the retirement drawdown phase of superannuation (note 12). The purpose of the framework is to inform policy reform and provide information to support regulatory work. Building a reporting framework for these purposes is essential for the health of Australia’s superannuation system and goes beyond consumer-focused transparency.

Although both reporting regimes are important, consumer-focused transparency is vital and should be prioritised so that future generations of retirees have access to free, reliable and easy to use information.

Dr Katrina Ellis is deputy chief executive officer of Super Consumers Australia.

Xavier O’Halloran is chief executive officer of Super Consumers Australia.

Notes:

1. Sorted.org, Kiwisaver fund finder: http://sorted.org/

2. Figures for 31 March 2025 in Table 1, APRA Quarterly Superannuation Industry Publication: https://www.apra.gov.au/quarterly-superannuation-industry-publication

3. Remarks to the Conexus Retirement Conference, 13 August 2025: https://www.apra.gov.au/news-and-publications/apra-deputy-chair-margaret-cole-remarks-to-conexus-retirement-conference

4. Table 3, APRA Annual Superannuation Bulletin published 30 January 2025: https://www.apra.gov.au/annual-superannuation-bulletin

5. SCA analysis of Table 1, APRA Quarterly Superannuation Product Statistics published 26 June 2025: https://www.apra.gov.au/quarterly-superannuation-product-statistics

6. Source Tables 7a, 7b, 7c, 7d, 9, 9a APRA Quarterly Superannuation Product Statistics published 26 June 2025 (ibid)

7. SCA Research Report

8. SCA Research Report

9. SCA analysis of APRA Table 1b Quarterly Product Superannuation Statistics published 26 June 2025, $256 billion invested in multi-manager multi-sector retirement investment options with $490 billion in the retirement phase reported by APRA in the Quarterly Superannuation Industry Publication published 26 June 2025 (ibid)

10. SCA analysis of APRA Table 1b Quarterly Product Superannuation Statistics published 26 June 2025. (ibid)

11. Conexus Institute, “How to best assess retirement income strategies”, David Bell and Geoff Warren, 31 July 2025: https://www.investmentmagazine.com.au/2025/07/how-to-best-assess-retirement-income-strategies/

12. The Treasury, Retirement Reporting Framework Consultation, 2025: https://consult.treasury.gov.au/c2025-672325

Leave a Comment

You must be logged in to post a comment.