Analysis of the retirement landscape by The Conexus Institute suggests that if profit-to-member funds do not move more quickly they face the risk of losing high-value members to the retirement options preferred by financial advisers.

The analysis, contained in the Institute’s State of Super 2026 report, says retirement represents a sizeable cohort “for nearly all funds, whether it be members in or approaching retirement”.

While the Retirement Income Covenant sets out funds’ obligations to develop, maintain and review a Retirement Income Strategy, APRA and ASIC continue to call out funds for slow progress.In addition to being railroaded by regulators, there is “a clear fiduciary obligation for funds to respond to the needs of a large cohort of their fund membership”, along with a clear commercial incentive to react to intense competition for members in the retirement phase from for-profit, or retail, platforms strongly supported by financial advisers.

“Retail platforms that service financial advisers require new members to offset their aging member profiles,” the institute says.

Financial advisers tend to target members approaching or entering retirement with reasonably high super balances and a desire for personalised retirement plans.

“Presently it seems like retail platforms are strongly preferred by financial advisers for implementing and maintaining such retirement plans,” the institute says.

The message is clear: industry funds and for-profit master trusts must evolve their service offerings or face the loss of high balance members to the platforms preferred by advisers.

While financial adviser numbers have declined precipitously over the past six or seven years, from a peak of more than 28,000 to a figure closer to half that number,that should not be a cause for super fund complacency.

“While financial adviser numbers have fallen and will likely grow slowly for a period of time, the objective of many platforms is to increase adviser efficiency and enable them to take on more clients,” the Institute says.

It identifies two clear opportunities for profit-to-member funds. The first is to increase the personalisation of services that cater for differing member needs, “and thus deter members from seeking external financial advice”.

The second is to make the fund’s retirement offering attractive to advisers, and “hence help to retain members or even attract members via referrals”.

“Many of the members who enter retirement will either be looking to their super fund for assistance in meeting their retirement needs or taking direction from financial advisers on how to proceed,” the institute says.

“While the expectations around fiduciary obligations are regularly stated, there is also a strong business case for funds to develop their retirement offering and clear business risk in lagging in doing so.”

The Institute says its call to action “applies not only to super funds, but also to policymakers, regulators and members of the super industry at large”.

“All concerned have much yet to do,” it says.

The Institute’s analysis covers 46 APRA-regulated funds that manage 1.44 million retirement accounts with total assets of $547 billion as at 30 June 2025, a figure that has increased from $468 billion a year earlier. It notes that while these are just over 7 per cent of total accounts by number, they represent 20 per cent of total fund assets. Across the Institute’s sample, retirement accounts average around $380,000 compared to $99,000 for accumulation accounts.

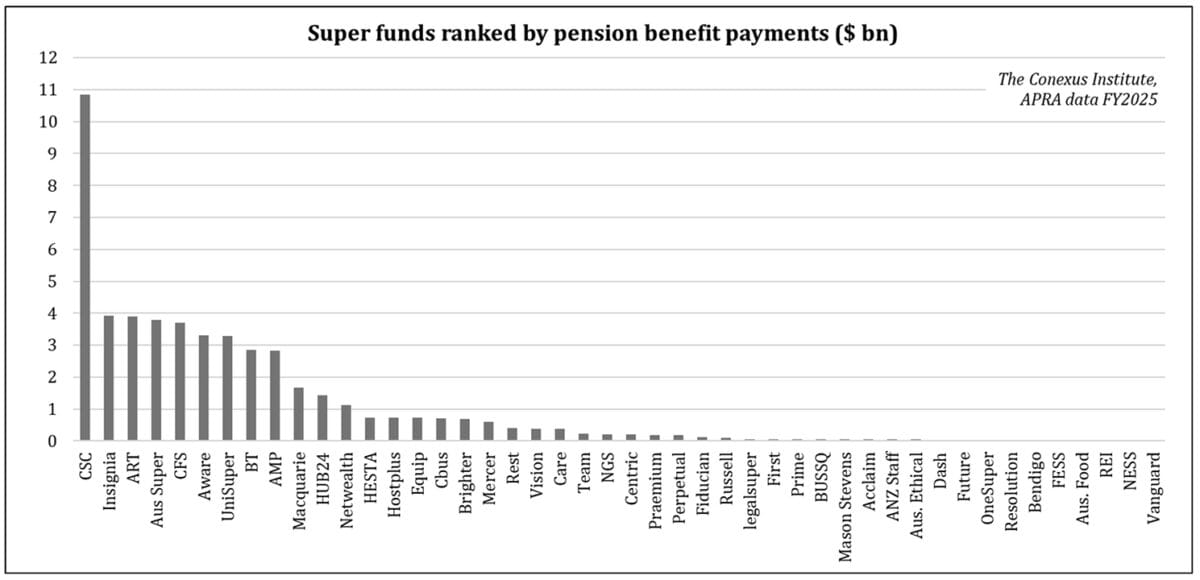

Super funds are already significant payers of retirement incomes, despite – in some cases – the relatively rudimentary nature of retirement income solutions, paying out close to $50 billion in pensions in the 12 months to 30 June 2025.

Not all funds are equally engaged with retired members, and the Institute notes that the 10 largest funds in the sample account for about 80 per cent of pension payments – including Commonwealth Superannuation Corporation which on its own accounts for 22 per cent of payments.

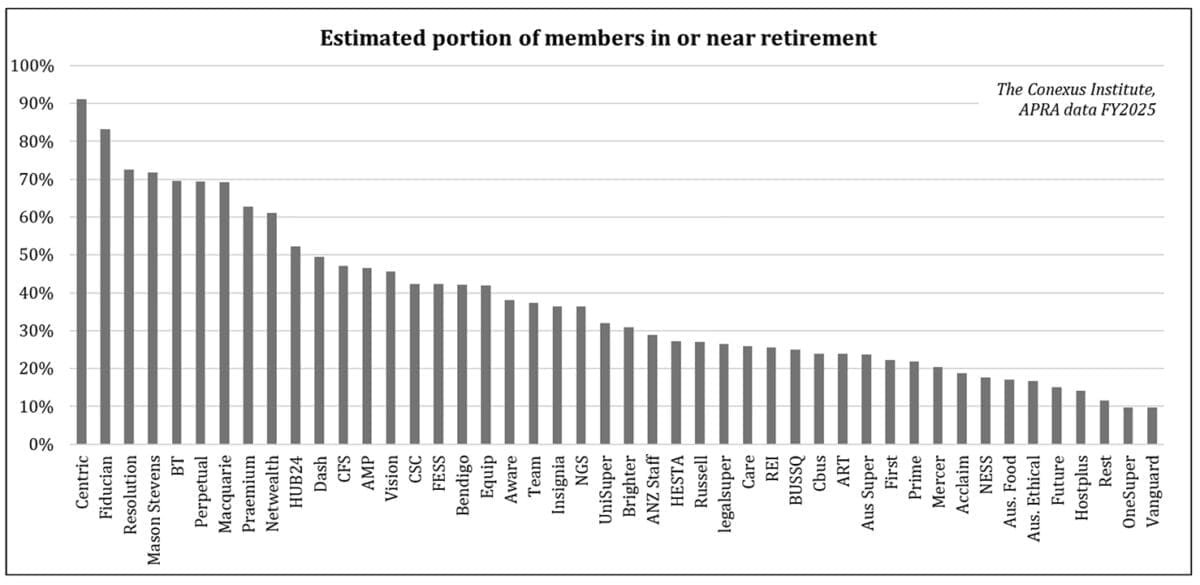

There’s considerable variation in funds’ exposure to the retirement cohort, ranging from a low of 0.5 per cent of accounts and 3 per cent of assets to a high of 84 per cent of accounts and 87 per cent of assets. The median is 5.5 per cent by account numbers and 14.8 per cent by assets.

A contributor to this variation is, of course, the make-up of the membership of funds.

“With regards to age, Rest and Hostplus have a younger demographic. On gender, NESS Super, Cbus, BUSSQ and Team Super have male dominated memberships; while HESTA stands out as a fund with large female representation,” the Institute says.

“Features of a fund’s offering may also impact on its member demographic. A good example is the sustainability focus of Future Group and Australian Ethical, which is reflected in memberships that are younger than average with a greater proportion of females.”

The State of Super report says that all types of funds must consider the business case for developing a retirement income strategy, and they won’t all arrive at the same conclusion, nor necessarily treat the issue with equal urgency.

“Member age demographics may be influential on how much resources and effort a fund is willing to commit to developing its RIS, and indeed appear to be contributing to the variable rates of progress across the industry in developing retirement offerings,” it says.

Profit-for-member funds must also consider the issue of cross-subsidisation, where large numbers of lower-account balance members may end up subsidising the development of retirement income solutions for a lesser number of higher-value members.

Even so, “for 80 per cent of our sample of funds, the proportion of membership in or approaching retirement exceeds 20 per cent”, the Institute says.

“For nearly 40 per cent of our sample, the proportion exceeds 40 per cent. The data suggests that retirement is an important and sizable challenge for the vast majority of funds.”

Leave a Comment

You must be logged in to post a comment.