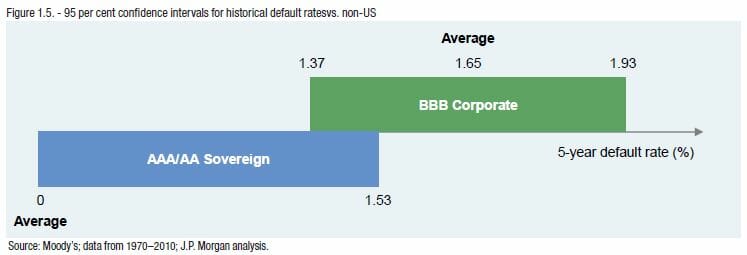

Over the 40 years since 1970, Moody’s five-year default rate for Baa corporate issuers is 1.65 per cent. Under the simplifying assumption that Baa corporate defaults occur independently and that there are 1000 issuers, each observed over eight five-year intervals, there is a 95 per cent chance that the underlying probability of default (of any individual entity) lies between 1.37 per cent and 1.93 per cent.

Over the same period, sovereigns rated better than AA have experienced no defaults. Assuming that there are 30 of them, the corresponding 95 per cent confidence interval ranges from 0 per cent defaults to 1.53 per cent. In other words, while our best guess for the five-year default rate of highly rated sovereigns is zero, there is a 2.5 per cent chance that it actually exceeds 1.53 per cent, which is close to the Baa average.

So there is much less daylight between the experience of highly rated sovereigns and Baa corporate than their average defaults suggest. This is purely the result of the limited experience of sovereign ratings. Had there been 1000 followed over the 40 years, the upper limit would shrink from 1.53 per cent to 0.05 per cent.

Rephrasing investment

The sense that there is greater uncertainty surrounding sovereign credit risk than corporate is only strengthened by a review of the rating agencies’ framework for evaluating the ability of each to repay their obligations. S&P bases its ratings of corporate bonds on a combination of two broad categories: business and financial risk. Both are calibrated extensively using quantitative measures, examples of which are traditional financial ratios such as debt/EBITDA, and measures of liquidity. Business risk involves some qualitative factors such as the firm’s growth prospects, but also many quantitative ones, such as a comparison of operating income with the firm’s peer group.

In general, the rating of US corporate debt is facilitated by the Securities and Exchange Commission’s reporting requirements for public companies. The large number of entities reporting this information has the effect of creating a sort of controlled experiment–rating corporates becomes, in part, an exercise in benchmarking.

In contrast, sovereign debt ratings involve much more subjective elements. S&P bases its sovereign ratings on two broad categories – politic, investment guidelinesal and economic profile, and flexibility and performance.

Approximately half the contributing factors are qualitative or subjective, such as the effectiveness and stability of the sovereign’s policymaking, the government’s willingness and ability to raise taxes and reduce expenditure, and ability to address domestic economic stresses through control of the money supply. These subjective elements reflect the realities of sovereign ratings. Sovereigns’ reporting is not bound by pain of prosecution and their opportunities to run off-balance-sheet operations are far less circumscribed than corporates’, with the result that the rating agencies have no other choice than to make judgments based on the disposition of the administration in power.

Leave a Comment

You must be logged in to post a comment.