Wood, who is also a founding shareholder in Australian equities boutique Vinva Investment Management, says funds, like all companies, are subject to an economic Darwinism. Successful businesses that satisfy customers in better ways are imitated by competitors and start-ups, then forced to innovate further to stay ahead. In financial markets, investors who bet early on new and successful strategies gain what’s known as a first-mover advantage. But new ideas get old fast as other investors catch on. Investment strategies evolve in a game of follow the leader and those used by the pack become similar.

Funds also use similar asset allocations because they are afraid of performing poorly as the pack moves on. This so-called business risk is not new or endemic to superannuation. In 1936, John Maynard Keynes wrote in The General Theory of Employment, Interest and Money that fear of failure kept businesses from using new or radical strategies. “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally,” Keynes wrote. In their pursuit of investment returns that outpace inflation, most super funds seem fearful of success through unconventional strategies. It may cause them to fail in isolation.

“Business risk is real,” Wood says. “If you do something different and you’re right, it’s great. But if you’re wrong, you can lose a lot.”

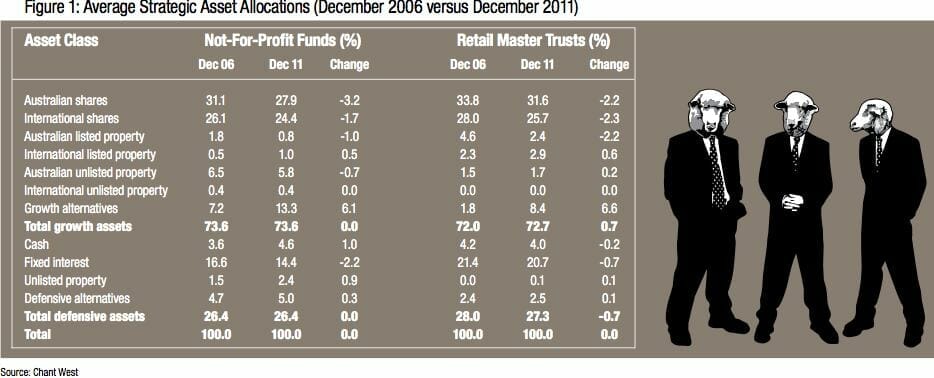

Australia’s predominantly defined-contribution pension system, which obliges members to pay at least 9 per cent of their salaries into funds, is also cited as a reason for herding. Funds’ common aim of maximising workers’ savings sees them invest heavily in stocks under the guidance of one of a handful of investment consultancies. This helps explain not-for-profit funds’ average allocation to Australian and global stocks of 52.3 per cent, and the 57.3-per-cent average allocation made by commercial funds, at December 2011 (see figure 1).

Input or outcome? Members’ freedom to move between funds, plus the widespread publication of short-term fund performance, also makes it practical to invest large sums of money in stocks. Members wanting to switch into the best performing fund can do so at 30 days’ notice. To enable members to move, funds need plenty of liquid assets. An equities bias also complements the stable income provided by the age pension, which acts for many Australians like an “inflation-linked bond provided by the government for life,” according to Wood. Given the importance of equities in a defined-contribution system where fund members are mobile, are funds guilty of consciously copying each other?

Leave a Comment

You must be logged in to post a comment.