The move to net zero emissions will be “the biggest transition any one of us will be involved in”, HESTA CEO Debby Blakey told the AICD’s Climate Governance Forum last week.

Company director and former Telstra CEO David Thodey told the same event that the imminent introduction of mandatory climate reporting was “the biggest change in my career in terms of what directors are expected to [do]”.

In late June, Treasury released a consultation paper setting out the government’s proposed design for a climate disclosure framework that will begin imposing reporting obligations on Australian entities from 1 July 2024. The framework will be aligned with the International Sustainability Standards Board’s (IISB) recently-released IFRS S2 Climate-related Disclosures as adapted to the Australian market by the Australian Accounting Standards Board (AASB).

Unique challenges

While institutional asset owners broadly welcome standardised and internationally-aligned disclosure requirements, the new reporting regime presents them with some unique challenges.

In its submission to the consultation, AustralianSuper noted: “Asset owners (including superannuation funds) and investment managers will be both users and preparers of climate change disclosure, and face reporting challenges that won’t be applicable to companies”.

Australia’s largest super fund argued the government’s proposed approach therefore needs “to be tailored to accommodate differences between companies and investors”.

And it is not only the biggest asset owners who are about to be impacted. Treasury outlines a three-stage phase-in “starting with a relatively limited group of very large entities”. However, the Investor Group on Climate Change (IGCC) says the proposed initial $1 billion total asset threshold would capture around 75 per cent of APRA-regulated funds, representing over 99 per cent of assets under management (AUM). IGCC’s submission argues “the structure of managed funds as distinct from companies warrants consideration of alternative thresholds”.

Reporting organisations will be required to disclose on governance, identification and management of climate risks and opportunities, transition plans, qualitative scenario analysis and scope 1, scope 2 and (after a one-year exemption) scope 3 greenhouse gas emissions. So what are the requirements that are most likely to keep asset owners awake at night?

Reporting time lags

The Australian Council of Superannuation Investors (ACSI) says while most entities covered by the proposed new regime reporting on operational emissions, asset owners and asset managers will be reporting on their portfolio emissions. “Here they must rely on investee entities to provide the data they require. “There will be even longer time lag for asset owners, including superannuation funds when they are dependent on information sourced from asset managers, who will in turn be waiting on information from investees,” ACSI said.

ACSI notes this may make it hard for asset owners to meet the same reporting dates as other entities as they will need time to receive the data, collate, reconcile and then release the consolidated information. There are further challenges where investees are unlisted companies or located in jurisdictions that have not or will not adopt the ISSB standards .

Coping with Scope 3

The government proposes that disclosure of material scope 3 emissions will be required for all reporting entities from their second reporting year. Scope 3 emissions disclosures could also be made could be in relation to “any one-year period that ended up to 12 months prior to the current reporting period”. The Australian Sustainable Finance Institute (ASFI) notes that where investors are required to report ‘financed scope 3 emissions’, this option for investees to report up to 12 months in arrears could result in investors “reporting emissions data that is up to 24 months old”.

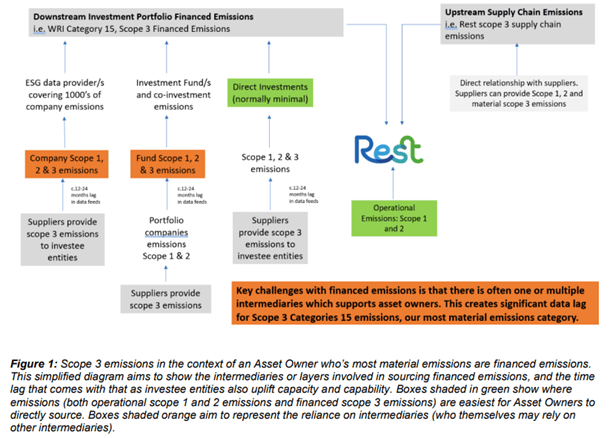

In its submission to the consultation, REST Super notes the complexities of reporting scope 3 financed emissions. A diagram it includes in its submission captures the basic flow of emissions data as it relates to REST as both a user and preparer of climate-related information. It uses orange boxes to highlight there are “significant challenges where intermediaries exist”.

Uncertainty

Added to this seems to be uncertainty about the “financed scope 3 emissions” asset owners will need to report. Most are assuming these to be the scope 1 and 2 emissions of their investees. But others are asking if this also covers the scope 3 emissions of their investees. There is a huge difference here, as for example, the scope 3 emissions of oil and gas companies typically represent 80-90% of the emissions in their value chains.

AustralianSuper’ says investors “require confirmation on what is required for inclusion in Scope 3 portfolio emissions”. It asks that when asset owners and managers report emissions associated with their investments does this require the reporting of scope 1 and 2 emissions associated with portfolio companies, or are investors expected to additionally collect and report portfolio company scope 3 emissions?

So why the uncertainty here? Greenhouse Gas Protocol guidance says scope 3 emissions from investments are the scope 1 and 2 emissions of investees.

But it also says, “if relevant”, investors should account for the scope 3 emissions of investees. An example provided is the scope 3 emissions of a light bulb manufacturer (i.e. from consumer use of sold light bulbs) when they are “significant compared to other source of emissions or otherwise relevant”.

Scenario shopping

The government is proposing reporting entities will be required to disclose climate resilience assessments against at least two possible future states, one of which must be consistent with the global temperature goal set out in the Climate Change Act 2022.

The Environment Defenders Office (EDO) is concerned about giving entities discretion to choose climate scenarios that are consistent with the objective of holding the global average temperature increase above pre-industrial levels to 1.5°C or “well below” 2°C (as stated in the Act). The EDO says there hundreds of climate scenarios that might seem consistent with that objective and is worried about ”scenario shopping” where entities may “cherry pick” scenarios that appear to minimise risk in their operations and business strategies.

ACSI also notes “this allows reporters to adopt a range of scenarios (i.e., one reporter could report against a 1.5° scenario, while another will report against a 2° scenario), and will reduce the comparability of scenarios”. ACSI recommends that reporting requirements state that one of the at least two scenarios disclosed should be a 1.5° scenario.

The Australasian Centre for Corporate Responsibility (ACCR), an environmentalist group, also observed that many companies are currently “using scenarios which are most favourable to their products; not disclosing fundamental assumptions of that scenario; and/or selecting particular parts of a chosen scenario to present”.

Transition plans

Treasury says there will be a “a focus on transparency, rather than prescribing certain transition planning activities or a level of ambition that firms should meet”. Instead of companies being required to adopt and disclose transition plans that, say, reflect actions to limit global warming to 1.5°C, the Government is hoping that “that investor demand will drive improvements in transition planning and target setting”.

This places added onus on asset owners to communicate their expectations to investees and develop their capabilities to assess and monitor investees. There is growing number of tools being created to help asset owners here.

For example, The Institutional Investors Group on Climate Change (IIGCC) has published an Investor Expectation of Corporate Transition Plans framework with a set of net zero alignment criteria to assess portfolio companies (The Europe-based IIGCC is aligned with the IGCC via the Paris Aligned Asset Owners initiative). Six criteria (below) are used to assess alignment of an investee’s transition plan.

The criteria can be used to classify assets held by investors into five “alignment maturity” categories. Asset owners and managers can then set and monitor portfolio coverage targets as to how their AUM are aligned.

Intended audience

The government’s framework is focused on enabling investors – and policymakers and regulators – to understand and assess the climate-related financial risks and opportunities faced by reporting entities. Similarly, IFRS S2 requires disclosure that is “useful to users of general purpose financial reports” in making investment decisions. However, IGCC notes the primary reporting audience for asset owners is their members or prospective members.

AustralianSuper agrees. “The level and type of climate disclosures suitable for superannuation fund members (who in the most part are not making investment choices) is not likely to be the same as that of an institutional investor or regulator,” it says in its submission. It wants the intended audience of a fund’s climate disclosure to be clearly stated, because if the end users are its members it believes “a simplified reporting template may assist communication”.

Russell Baker is a journalist and consultant specialising in ESG and impact investing.

Leave a Comment

You must be logged in to post a comment.