There has been increasing demand for equity indices in Asia. This is because global investors want to benefit from the region’s growth, and consequently from its financial markets. As many US and Europe-based investors do not have the expertise to conduct stock picking in Asia, equity investments are often passive for Asian-oriented portfolios. Therefore, the question of index quality in Asia is an important issue.

In recent research, we assessed the quality of Asian indices by focusing on the following three aspects: efficiency, concentration and stability. From our study, it appears that all the popular indices used in Asia as reference benchmarks are inefficient in the risk/return sense, with some of them being more so than others. For all of them, an equal-weighted index constructed from the same components outperforms the corresponding cap-weighted market index. The levels of inefficiency of Asian market indices were found to be quite comparable to those of European and US indices.

Inefficiencies explained

One of the explanations for this inefficiency is that most indices in the Asia-Pacific region are highly concentrated. In addition, the level of concentration is not constant over EDHEC-Risk Institute recently concluded a study that assessed the quality of asian stock market indices. time. The concentration in indices leads to less diversified portfolios and performance drag. Finally, our research evidenced a lack of stability in risk factor exposures for Asian indices, to a greater extent than what was previously shown in Europe and the US. This latter issue is a major concern, particularly for passive investors who are confronted with unexpected changes in style bets when they are holding the index portfolio.

Investing in Asian indices may come with important challenges for investors, including operational challenges for running portfolios, which include stocks from different markets and in different time zones. This effort may be worthwhile due to the expected outperformance of these markets. However, an important question is whether the distance of equity investments in standard indices compared to improved indices in terms of performance is, in the end, not as meaningful as the distance between US standard indices and Asian standard indices, for example. Our research assesses the distance from optimal in-sample portfolios in Asian markets and finds that this distance is significant but, all the same, comparable to the distance found in US markets, for example.

Sharpening up the numbers

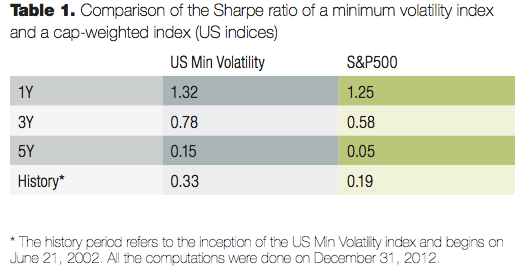

It may be interesting to present a comparison between the performance of a cap-weighted index and the performance of an index using an improved weighting scheme. We perform the comparison on both the US market and an Asian market. We choose to use a minimum volatility strategy as the improved weighting scheme. Table 1 displays the Sharpe ratio (a measure of excess risk-adjusted return) obtained for the US Minimum Volatility index and for the S&P 500 (cap-weighted) index for various time periods.

In all cases, the US Minimum Volatility index exhibits higher Sharpe ratios than the S&P 500 index. If results obtained on a one- year period appear to be comparable, the gap between the two Sharpe ratios became wider for longer periods, with, for example, a Sharpe ratio of 0.15 over a five-year period for the minimum volatility index, compared to a Sharpe ratio of 0.05 for the cap-weighted index. Similarly, over the period corresponding to the whole data history available for the minimum volatility index, and including more than 10 years of data, the minimum volatility index significantly outperforms the S&P 500 index with a Sharpe ratio of 0.33 versus 0.19 for the cap-weighted index.

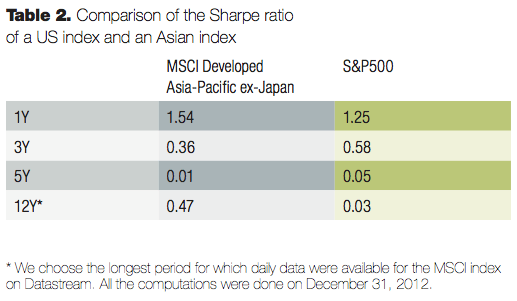

Alternatively, the investor may have invested in an Asian index instead of the US index. In order to show the possible improvement, we compared the Sharpe ratio of the MSCI Developed Asia-Pacific ex-Japan index and the Sharpe ratio of the S&P 500 index. The results are displayed in Table 2. We see that investing in an Asian index leads to a significant performance improvement both for the shortest period and the longest period. Over the one-year period, the US index produced a Sharpe ratio of 1.25, while the Asian index produced a Sharpe ratio of 1.54. Over the 12-year period, the Sharpe ratio of the US index was not far from zero (0.03), while the Asian index produced a Sharpe ratio of 0.47. Over the 5-year period (2008-2012), both indices produced respective Sharpe ratios that were not far from zero.

In view of Tables 1 and 2, it appears that while investing in an Asian market rather than in the US market can lead to significant improvements in performance, the performance improvement provided by the choice of a better weighting scheme is more constant through time, and less related to the choice of the investment period, as shown by results obtained for the US (displayed in Table 1).

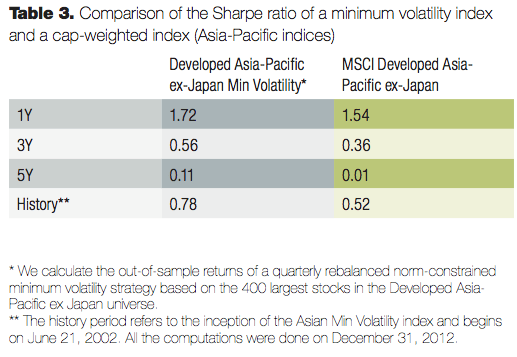

If investors want to capture the premium of Asian markets efficiently, they have the possibility, as on the US market, to use an improved weighting scheme for the Asian stocks. Table 3 displays the Sharpe ratios obtained for the Developed Asia-Pacific ex-Japan Minimum Volatility index and for the MSCI Developed Asia-Pacific ex-Japan (free-float weighted) index for various time periods. The Asian Minimum Volatility index exhibits higher Sharpe ratios than the MSCI Asia index for the whole time period. The most significant improvements are obtained for the three-year period, with a Sharpe ratio of 0.56 for the minimum volatility index versus 0.36 for the MSCI index, as well as for the historical period, which includes more than 10 years (0.78 versus 0.52).

Overall, if investors want to capture the risk premium in Asia, it is regrettable that they then suffer the drawback of a sub-optimal weighting scheme choice. Indeed, investors should recognise that the choice of an efficient weighting scheme to capture the outperformance is probably as important as the choice of the right geographic exposure.

Leave a Comment

You must be logged in to post a comment.