A world-leading professor of finance has argued that hedge funds have retained a positive value proposition in the wake of the GFC.

Professor Stephen Brown of NYU Stern School of Business also told attendees at a Centre for International Finance and Regulation seminar in Sydney this morning that operational due diligence can add 250bps per annum to diversified hedge fund strategies.

According to Brown, a perfect storm which started in the GFC led to a misunderstanding of the value proposition of hedge funds. Returns in recent years in hedge fund strategies have been poor compared to the market, but he emphasised they are meant to be uncorrelated, and a diversified hedge fund strategy still made sense for intuitional investors.

“People worry about fees, people worry about expenses, but after all that, after they are all accounted for, they remain a value proposition. This was true before the crisis and they remain a value proposition after,” Brown said.

He added as individual hedge funds are risky, the only reasonable way institutional investors can invest is through a diversified hedge fund strategy, with no more than 5 per cent of a portfolio put towards the strategy.

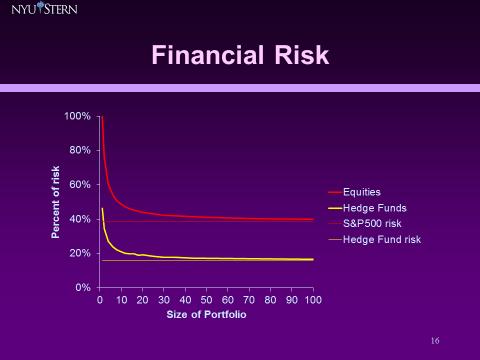

“The proposition has to be qualified. This is true for diversified hedge funds. If you have a portfolio of about 15 funds you have a risk level of about half of [a diversified strategy] the SNP500,” Brown said.

He cited research that showed the only “free lunch” available in the financial markets was diversification. It showed a dramatic drop in risk simply by having diversification.

“Indeed this picture was so influential and powerful it led to a change in the law that had been standing for 800 years – the trust law,” Brown said.

Acknowledged problems

Brown did acknowledge there were problems with a diversified hedge fund approach. The first comes from nature of hedge funds. They earn a positive return in both good and bad markets because they provide liquidity. However, when the rare event of a liquidity crisis occurs they perform badly, whether a diversified strategy is used or not.

The second problem is operational risk, which is particularly prevalent as a lot of hedge funds are reasonably obscure and small.

“It’s a danger to invest in a very small diversified fund strategy because if it has very small assets under management they can’t afford the necessary due diligence. That’s a fixed cost. For a large fund it’s trivial, for a small funds it’s not,” Brown said.

He gave a simple formula to help in the decision making process of whether to take a hedge fund on or not:

Funds under management (FUM) x Management fee > US$12,500

Number of subfunds

The FUM (US$) are divided by the number of funds the diversified hedge fund is investing in. The ratio is then multiplied by the decimal fraction of the management fee.

If the resulting figure is less than US$12,500 the investment should not go ahead, because this is the very minimum it costs for operational due diligence. According to Brown’s, research having operational due diligence can add 250bps per annum.

“In 2012 I found that only 20 per cent of these diversified fund strategies met this test, and that’s pretty shocking,” Brown said.

He qualified that this formula is an understatement, not only because it does not reflect all the costs, but also because the most reputable funds would be looking at 10 times the universe they are investing in.

“That’s why there is economies of scale in diversified funds strategies. Just don’t invest in small diversified funds, that’s the bottom line.”

Leave a Comment

You must be logged in to post a comment.