In the first of a series of how to guides for super funds Alastair Adamson, consultant at Rice Warner, walks through the steps they need to take to ensure the lowest possible premiums when renegotiating their group insurance package.

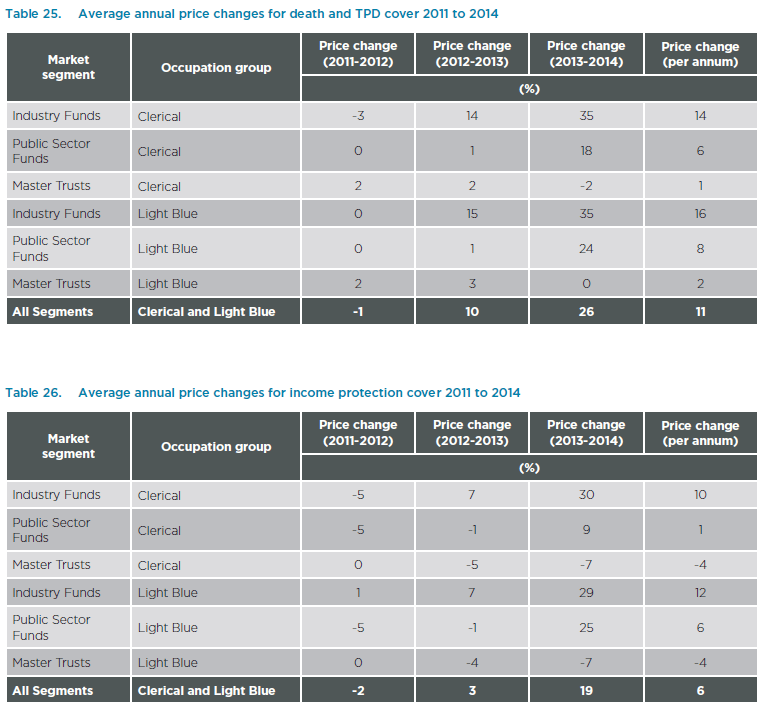

Over the last couple of years wholesale premiums have sky rocketed, and will continue to do so over the next 1-2 years. Average price increases over 2013-2014 for death only, death and TPD, and income protection have been +15 per cent, +26 per cent and +19 per cent. These figures mask a much larger underlying upward shift in prices, as they are typically reviewed only every three years, so only one-third of prices will change in any one year.

Why has this happened?

Australia has recently seen a deterioration of experience for all product types, but worst of all for TPD. This has been due to increased member awareness, resulting in greater number of claims, often with late notification. There have also been challenging economic conditions, a greater involvement of lawyers and there has been a period of product innovation that has led to more generous benefits in terms of automatic acceptance limits and relaxed definitions.

We have seen historical price reductions which, with the benefit of hindsight, were based on over-optimistic assumptions and poor data. Finally, not unsurprisingly, we have seen a lack of reinsurer support in the Australian market, resulting in a less competitive environment.

So how do trustees negotiate a good deal for their members in this challenging environment?

With some funds experiencing price increases of over 150 per cent, how is it best to negotiate with insurers?

Claims experience

The first step is to understand how your claims experience compares with the rest of the market. If your membership is primarily white collar, the likelihood is that the recent claims experience will have been reasonably stable. If your membership is primarily blue collar, or (if you are an industry fund) your industry has experienced losses or adverse changes, then the likelihood is that the experience will have deteriorated over the last couple of years.

A good exercise before going to an insurance review is to review your claims experience, to get to understand your members; who is claiming and who isn’t, and look for patterns. Secondly, if you are able to look at your experience in comparison with your market segment and the broader market – this will put you in a strong position when going into negotiations.

If your experience has been poor, then it is important to establish (beyond environmental factors, that you can’t control) why this is the case. This is where you have a degree of control – if you agree to modify some of the terms and conditions, then potentially your claims experience can be managed better and premium increases can be offset.

Product Design

The great thing about group insurance is that each fund can customise its default option to take account of the profile of its membership. In each review it is important to re-evaluate whether your insurance product design is appropriate.

- Default cover

Is your default insurance cover appropriate? Do your members need equal amounts of death and TPD cover, or more TPD at younger ages? Some insurers won’t quote where TPD cover is more than death cover; so one trending option is to provide default income protection.

- Adequacy of risk controls

On what terms can your members start cover or increase cover without underwriting? When they first join and upon certain life events? Do the same terms apply to casuals as they do to full time employees? Do your current terms expose the fund to anti-selection?

- Erosion of account balances

Check the continuing appropriateness of the amount of cover being provided and the affordability of this level of cover, especially following significant price increases.

- Disability definitions

You need to ensure that the definitions are both SIS compliant and are in the best interests of the whole membership of the fund.

- Checking of cross-subsidies

Many funds have cross subsidies. If some of your fund’s members are cross subsidising other members – Is this still appropriate?

- Pre-existing condition (PEC) exclusions

Some funds are introducing pre-existing condition exclusions, and other exclusions, as part of a comprehensive risk control program.

Pricing

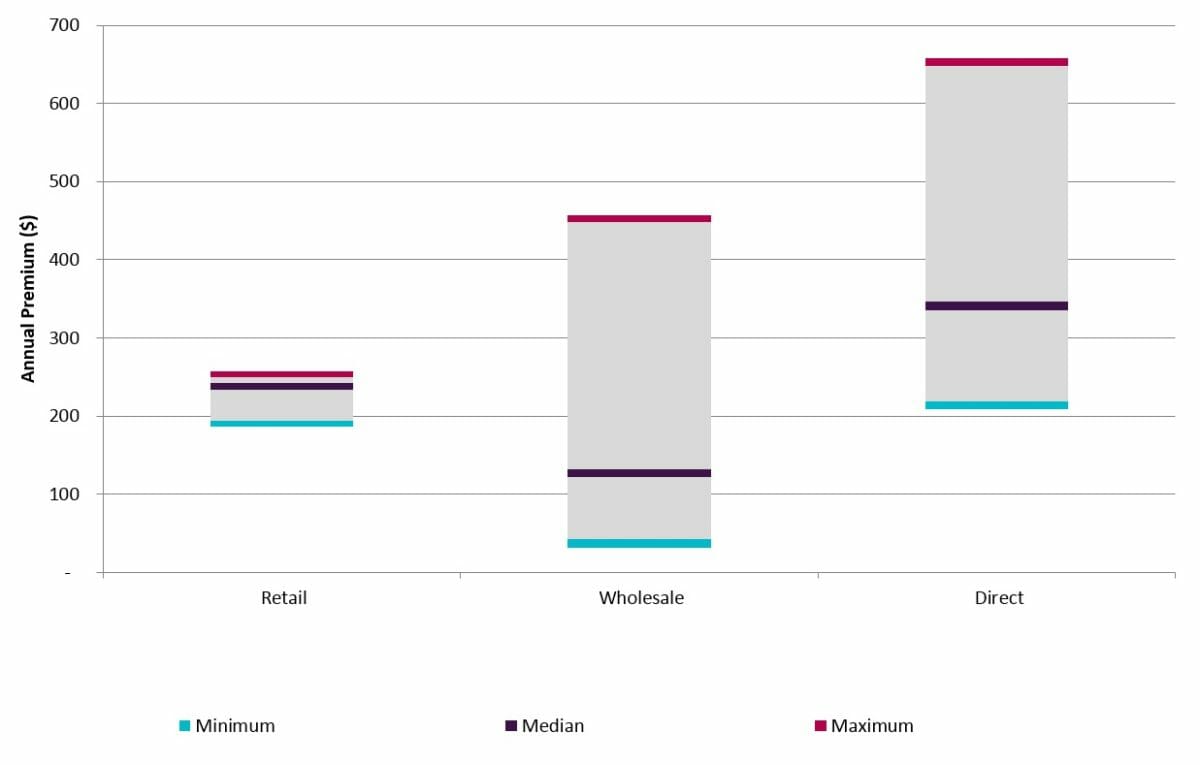

It’s important to get things into perspective, generally speaking wholesale prices are cheaper than both retail insurance (sold through advisers) or direct insurance, with the median price for insurance being well below either of these product types. Pricing of your book will depend on the design of your product, and your claims experience amongst other factors.

Reporting, claims and communication with the insurer

It’s great to have the best product design and pricing for your members, but an often forgotten element is the support that your insurer provides, and the better the fund communicates with the insurer, the better the outcomes are for members.

We recommend you focus on:

Member experience – a) Ways to make it easier for members to get cover, whether by telephone or online. b) Claims lodgement processes and ability to track progress

Fund experience- a) Tailored service models – split between administrator, fund/trustee and insure. b) Underpinning technology and reporting processes. c) Service levels for underwriting and particularly around claims

Early intervention strategies – a) Rehabilitation specialists and return to work programs. b) Healthy work places

Conclusion

Whilst there have been recent increases to premiums and changes to definition for group insurance members, we are confident that the market will stabilize and reach its own equilibrium. The value of insurance to superannuation members is not in doubt, however trustees must engineer a balance between the need to provide members with affordable protection against the financial risks of mortality and disability, without unduly eroding super balances.

In this challenging environment, trustees who understand the implications of claims, product design and pricing will be in the driver’s seat.

The 4th annual Group Insurance Summit is being held in Sydney on August 19, 2015.

To register for the conference visit https://www.eiseverywhere.com/ereg/index.php?eventid=125466&

Leave a Comment

You must be logged in to post a comment.