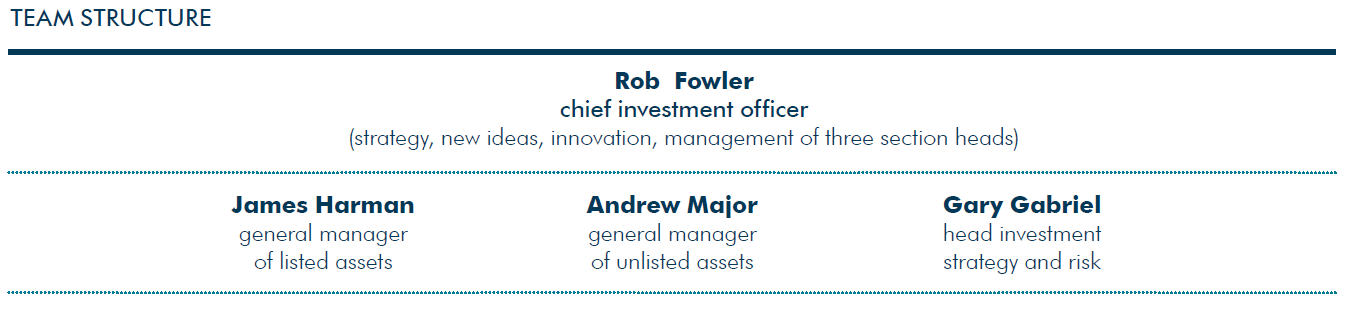

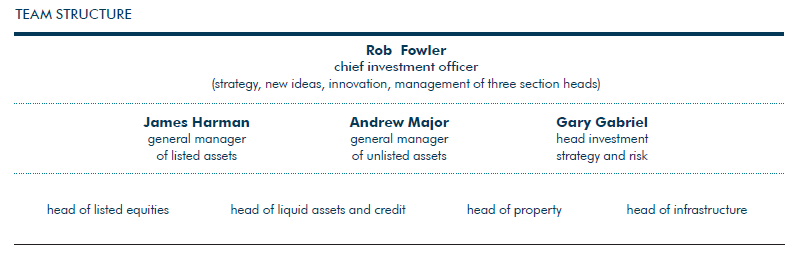

The job of Rob Fowler, chief investment officer of HESTA, is about to change significantly. He still has the same job title, but a team restructure means he will spend less time on day-to-day investing, and more on strategy and innovation.

HESTA has joined the ranks of the world’s most sophisticated funds by raising the size of its investment team to enable a more granular approach to its asset allocation and implementation. It will allow its chief investment officer the time to think about where its next move might be, rather than day-to-day investment matters, which have transitioned to three investment heads with James Harman looking after listed assets, Andrew Major general manager of unlisted assets, and the newly-appointed Gary Gabriel as general manager of investment strategy and risk. In particular, Gabriel is taking on a responsibility that took up much of Rob Fowler’s time.

The main investment team – which is set to double from nine to 18 over the next two years – will now report directly to these three staff instead of Fowler.

With less management responsibility, hands-on investment work, or trips to overseas fund managers, Fowler will now – in a word he uses frequently – “innovate”, and pose left field questions at the $33 billion fund. The increased resourcing will give the investment team, “more control, and veto over what we are investing in”.

These projects can be listed as follows:

These projects can be listed as follows:

- The control and veto has already begun with the market-leading ESG scrutiny it applies to its investments, but will now be more continuously applied to ensure that its portfolio of managers is not creating redundancy, rather than alpha. To help, Fowler has the go-ahead to appoint two analysts over the coming year.

- A much more flexible approach to allocating across alternative growth assets. Fowler reasons that there needs to be flexibility in the deployment of capital in the unlisted space – if the team could not put money to work in infrastructure, then it could potentially be deployed in property. Likewise for private equity where the allocation could also go into shorter-term high-return positions anywhere across this new team.

- There will also be a concerted effort to purchase private equity at cheaper rates than 2 and 20, either as a co-investor or by exploiting the virtues of being a long-term investor as an alternative to the traditional private equity five-year hold model and then divest.

- One project that has been completed recently was a review of the cost of currency transactions to seek to reduce “frictional transaction costs”.

Across all these projects the theme is a more granular approach that will lower risk, identify opportunity and reduce investment costs – the base fee for the default option is currently 59 bps.

However, unlike most other large funds HESTA will not be using its increased scale for internal management just yet. Term deposits are managed in-house, but other than that it favours co-investments or mandates in unlisted assets, property and unlisted debt.

Fowler reasons that the competitive pricing of its passive equity and infrastructure provider IFM and its property manager ISPT, for both of which it is a shareholder, means that it has not yet been worthwhile to consider in-house investing.

“IFM know if they keep ticking up the price for indexed Australian equities to the point where it is worth it for me to put in the required systems and employ some people to do it, then I will consider it.”

“IFM know if they keep ticking up the price for indexed Australian equities to the point where it is worth it for me to put in the required systems and employ some people to do it, then I will consider it.”

The case is the same for the fees payable on the infrastructure managed by IFM and the property managed by ISPT.

Fowler notes that HESTA has supported IFM starting an international equity capability, not because it will prove cheaper than other passive managers, but because it will be able to offer factor-based investing for “significantly less” than the commercial managers look to charge for such services.

Consultant

In all of this, the role of the fund’s investment consultant, Frontier Advisors, has changed. Frontier is now structured so that it can also work on a project basis on the likes of co-investments and property acquisitions with the fund, providing the extra resourcing capacity when needed.

Fowler describes this role as forming an integral part of the team. “They have restructured themselves sensibly to be able to provide personnel to effectively substitute our extra heads to assist with due diligence – a bit of a hit squad so to speak,” he says.

{kind=link}

Leave a Comment

You must be logged in to post a comment.