Michael Zelouf, CFA, and head of London operations at Western Asset, shares his perspective with Investment Magazine on how to secure a reasonable level of income from bonds while maintaining their role as a ballast to equities and a tool for capital preservation.

Central bank rate cuts, quantitative easing, a subdued global recovery and extraordinarily low inflation have left global bond yields close to record lows. Some sectors still offer value but a divergence from the current benign environment could see volatility increase. The focus for bond investors will therefore increasingly be on seeking additional flexibility from their bond strategies to protect investments from increased market volatility and limit potential losses.

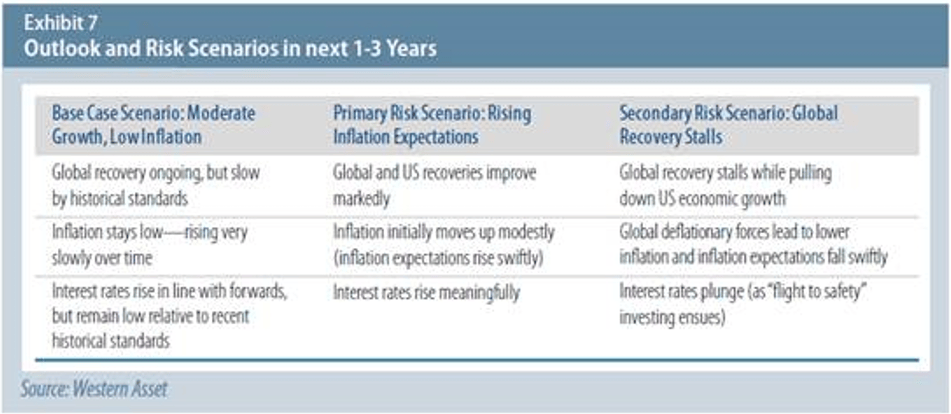

Near term, the global economy is expected to remain on a modest recovery path as low inflation boosts real incomes in developed economies and allows central banks to maintain a very accommodative monetary stance. The primary risk to bond investors is that inflation will begin to rise in a belated response to extraordinary monetary stimulus. Fears of higher inflation could see government bond prices fall sharply even as credit spreads narrow as better growth supports credit fundamentals. A less likely but potentially more serious “tail” risk is a deflationary stall in the global recovery. This could occur if the headwinds of China’s slowing economy further weaken commodity prices and other developing economies and ultimately drag down US and eurozone growth. This would raise fears that inflationary expectations could become “unanchored” from central bank policy. Government bonds, especially for longer maturities, would benefit, but credit and other spread sectors could perform poorly.

Against the background of these risks, bond investors are grappling with a challenging dilemma: how to secure a reasonable level of income while maintaining bonds’ role as a ballast to equities and as a reliable asset class for capital preservation. Our analysis points to actively-managed, global and unconstrained bond strategies offering more effective solutions to these investment objectives versus passive bond strategies.

Traditional active bond management have risk profiles that broadly track those of bond indices but with the flexibility to cushion price declines during periods of rising rates by underweighting duration and overweighting sectors that offer value. Unconstrained fixed-income strategies which are not obliged to track traditional benchmarks have the latitude to manage risks more nimbly and seize opportunities when valuation diverge significantly from fundamentals. This latitude can help deliver positive returns in both positive and negative bond market environments.

(Continued below)

[tv playlist=’55c989c3150ba0fb768b458c’ theme=’im_article’]

This does not imply that there are no risks from active and unconstrained bond strategies. Each strategy delivers a distinct mix of return, risk and correlation characteristics at different points in the interest rate and business cycle. Ultimately, the choice of strategy for the investor must be a thoughtful one based on factors such as income, liquidity, principal preservation and risk tolerance, investment horizon, diversification to risk assets and regulatory constraints on investments. Finally, investors should carefully evaluate asset managers’ resources, process and track records in managing active and unconstrained fixed-income strategies

How Are different Strategies Likely to Fare in the Future?

Our fundamental outlook and risk scenarios for the next 1 to 3 years are summarized in Exhibit 7 (click to enlarge).

Leave a Comment

You must be logged in to post a comment.