In January this year, the value of assets held by MTAA Super ticked over the $10 billion mark for the first time in the fund’s 26-year history. If the value remains above that threshold, then the Conexus Financial Superannuation Awards 2017 Medium Fund of the Year winner will next year find itself competing for recognition against the giants of the industry.

MTAA Super’s executive manager of investments, Philip Brown, says the funds-under-management milestone marks “an important time for the organisation – not just the investments team but the whole organisation – to stop and reflect on what we’ve achieved over 26 years”.

“Not just the people here now, but those who came before us,” he says. “It was a milestone for everybody, and every little piece of effort adds up to the $10 billion, in my view.”

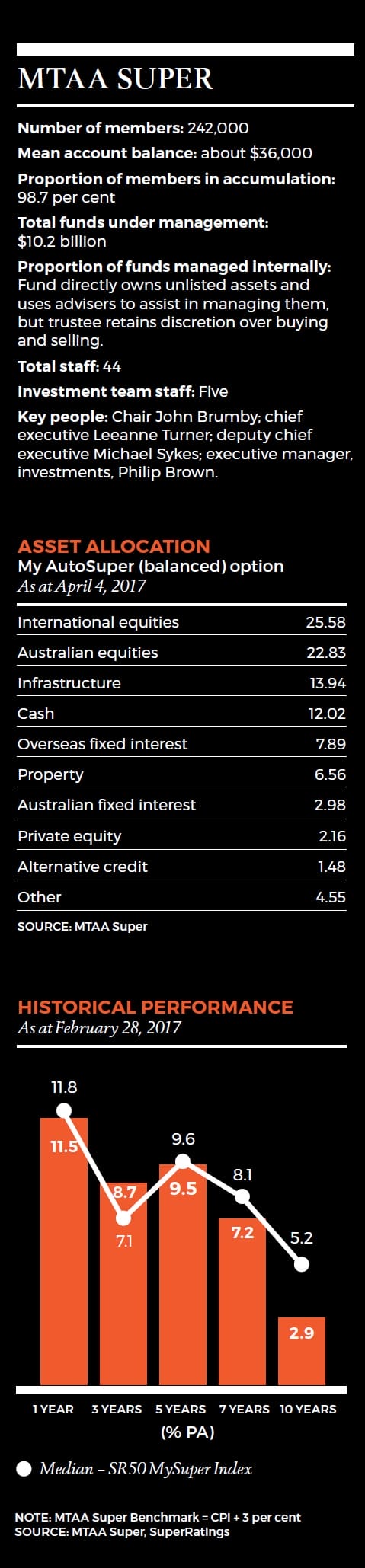

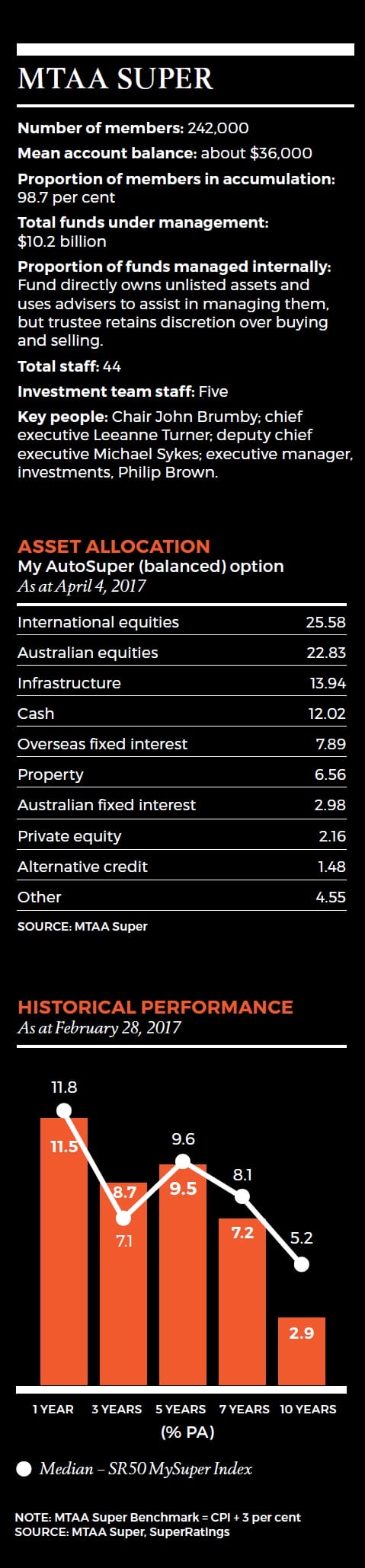

MTAA Super has bounced back since 2008-09, when it posted a nearly $1.7 billion investment loss on a portfolio then valued at less than $6 billion, and became the target of an Australian Prudential Regulation Authority investigation into its governance and investment performance.

Back then, about 45 per cent of the fund’s portfolio was invested in unlisted, illiquid assets. Today, the allocation to unlisted assets has been reduced to less than 30 per cent, following a strategy overhaul.

Brown, who has been with the industry fund for motor trades workers for 12 years, joined as “the fund’s first dedicated investment resource”, looking after MTAA’s in-house assets.

The investment chief now heads a team of five, charged with managing the fund’s relationships with suppliers – including external fund managers and investment advisers – and with managing a portfolio of property and infrastructure assets in-house.

It’s a small team, Brown says, but “small teams can punch above their weight often”.

“We do that,” he says. “We don’t necessarily manage a lot of the money inhouse in the traditional sense…But [our team] manages a lot of external relationships and an investment operations function.

“A lot of time and effort is employed in managing our alternatives, or the unlisted part of our portfolio, which is about 26 to 30 per cent, depending on whether you look at the actual or strategic weights…We do directly own and manage those assets. That’s the closest we have to in-house assets, and we do that under the guidance of advisers.”

The Goldilocks zone

Brown says that, for the foreseeable future, MTAA Super will enjoy the best of both worlds – capitalising on economies of scale but remaining agile.

“At our size, we’re not too big to be locked out of investment opportunities, not too small to be able to access them with some efficiency. We think we’re still enjoying quite a good sweet spot,” he says.

“It’s hard to be precise about what that range is, but it’s around our size.

“In particular, we can access some very good investment opportunities that large funds, I believe, couldn’t because [the opportunities] are too small to be effective. We can access some fund managers and build the listed part of our portfolio in a way that some of the larger funds can’t, and some of the smaller funds can’t justify on a fee-efficiency argument.”

There are pluses and minuses to managing a small investment team. On the one hand, it’s small enough not to require layers of reporting; on the other hand, everyone has to be on the ball, all the time, and there’s nowhere to hide.

In this context, Brown says his approach to managing the team is “less structured than some managers’ ”.

“My personal style is I expect my staff to be self-starting and manage their own workflows. I allow them to proceed with their work and come to me as a sounding board. We have a fairly fluid approach,” he says. “We like to enjoy what we do and we see the lighter side of things but, of course, what we do is very serious, in terms of looking after members’ money.”

Evolution in management

Brown says that as the fund continues to grow and the investment team expands to match, it will require more structure and a change in his own role. He says this will necessitate an evolution in his management approach, “because when I started here, I was a doer”.

“I’m still a bit of a doer, and I need to be a little bit more of a manager,” he says.

“I can lead the team by my example and my work ethic, but ultimately we are looking to enhance and empower the team more and for me to have more of an oversight role, as someone in my [position] should.

“I still consider myself one of the team in terms of task allocation day to day, as opposed to just being a manager. But it’s a personal goal and challenge for me to have the team doing more and me doing less.

“Given the interesting things we do here, it’s something I’ve always liked to be involved in; so it’s just a personal approach and a character trait.”

Winning turnaround

Winning turnaround

Since the arrival of MTAA Super chair John Brumby and chief executive Leeanne Turner in 2011, the fund’s investment approach has changed considerably from when it was about 45 per cent invested in illiquid assets and got caught out when the global financial crisis hit.

Turner says it was the former board, rather than Brown, that had decided to position the fund so deeply into illiquid assets, and that the investment chief has been instrumental in implementing the strategy that has underpinned the improvement in the fund’s fortunes since then.

“We did have to undertake a divestment program at that point,” Turner says. “Phil had pretty much sole carriage and responsibility for that. It had to be carried out in a very measured and strategic way, so we weren’t diluting members’ returns and we weren’t in any sort of fire sale situation at all. That was down to Phil’s expertise.

“Phil was a large part of the solution, and I felt so strongly about that I nominated him for an award.”

In 2013, Brown was awarded the Super Investment Award for Excellence by the Australian Institute of Superannuation Trustees.

Turner says she and Brown have a close working relationship, although her style, much like Brown’s own, is to “empower my executives so they have carriage and responsibility for their areas of expertise”.

“In Phil’s case, I have the utmost confidence and respect for him and what he brings to the role,” she says. “I’m very happy to let him run things.”

Brown says the fund’s investment strategy has been “fundamentally altered” since 2011 and its current exposure to infrastructure and property is about 26 per cent.

“Some of the advisers are the same but the portfolio construction has been fundamentally enhanced and rewritten,” he explains. “A whole new series of parameters around vintage, diversification, position, sizing and other things has been implemented. Liquidity management has been fundamentally overhauled. A whole range of things mean what we do and how we do it today and what we’ve done in the past really can’t be compared.

“We had a different chief executive, we had a fundamentally different board and they had an approach that doesn’t exist anymore.”

Boosted by windfall profits from the sale of the Moto Hospitality service station business in the UK in 2015, MTAA Super has returned to near the top of the performance charts, a position it regularly occupied before the GFC.

MTAA Super’s MySuper option was the second-best performing fund in the three years to the end of February, SuperRatings data shows, with a return of 8.68 per cent a year, narrowly beaten by Hostplus’s 8.83 per cent a year, and ahead of the Cbus MySuper option’s 8.46 per cent a year. It’s a significant improvement on the 2.92 per cent a year return the fund achieved over the last 10 years.

“We have hit our stated investment objective over periods out to the last seven years, which is the recommended minimum investment time horizon for the balanced MySuper option,” Brown says.

“The 10-year number is low, as it still includes the impacts of the GFC. The investment strategy today and the portfolio are vastly different, in many ways. The strategy is more refined now than it was 10 years ago.”

Brown says many of the issues MTAA faced were “misreported or misstated” at the time.

Nevertheless, he says it “wouldn’t have been a very intelligent approach not to have learned something from those things along the way”.

“There have been many things to learn, a lot of enhancements, and we’re on a journey, still, of continuous improvement, as every organisation should be,” he says.

Today’s challenges

In today’s market conditions, Brown says, investing in infrastructure and property – the assets MTAA manages in-house – is particularly challenging.

“We’re being very selective in that space and not wanting to deploy too much capital at a potential high point in the cycle,” he says.

“We’re able to play in a part of the market, with our size, that is probably less competed over on a global basis.

“We do not need to play in large [global] asset-bidding competitions against huge sovereign wealth funds or very, very large funds that are looking for large stakes in large assets. We can play in a smaller part of the market but do it efficiently.”

Brown says MTAA Super has found what it believes to be better risk-adjusted returns in “midmarket” assets, and in particular in infrastructure debt, rather than infrastructure equity. He cites Alpha Trains, a European rolling stock leasing company, which MTAA Super invested in a couple of years ago and, more recently, Calvin Capital, a UK smart metering company.

“You need to be very careful about how you deploy your capital in that market environment. We’re able to avoid the large, heavily contested auctions for big assets,” he says. “We can deal in different parts of the market and still deploy capital effectively. That’s important for us, particularly given how much we play in private markets and the unlisted space.”

Perhaps not surprisingly, given MTAA’s ups and downs over the last eight or nine years, Brown says resilience is a characteristic he values highly.

“It means continuing to focus on the goal and the member outcome as the ultimate – persevering, really,” he says. “This organisation and many of my colleagues, and hopefully myself, have been very resilient, in terms of remaining focused, staying the course, striving for continuous improvement, dealing with issues, learning along the way, and just remaining focused on what we do every day.

“It’s a very powerful concept.”

Leave a Comment

You must be logged in to post a comment.