An industry-wide study has concluded that nearly one-quarter of all superannuation funds are failing the Australian Prudential Regulation Authority’s scale test, leading the author of the report to call for the regulator to do more to shut down these funds.

The SuperRatings’ benchmark Report 2017 shows that roughly 23 per cent of superfunds studied, or 32 out of 140, should be considering winding-up or finding a merger partner.

SuperRatings granted Investment Magazine exclusive access to the annual super fund benchmarking study it produces for clients.

No individual funds are identified in the report but it shows some striking trends in how average performance varies between small, medium and large funds.

One of the most critical issues highlighted in the 2017 study is the disturbing number of funds that are struggling to pass, or even failing, the regulator’s scale test.

The Australian Prudential Regulation Authority’s scale test requires that super funds can show they are financially sustainable and positioned to deliver in their members’ best interests both now and into the future.

The application of the scale test is stricter for MySuper funds – those entitled to be nominated by employers as a default option for workers who do not wish to choose their own fund.

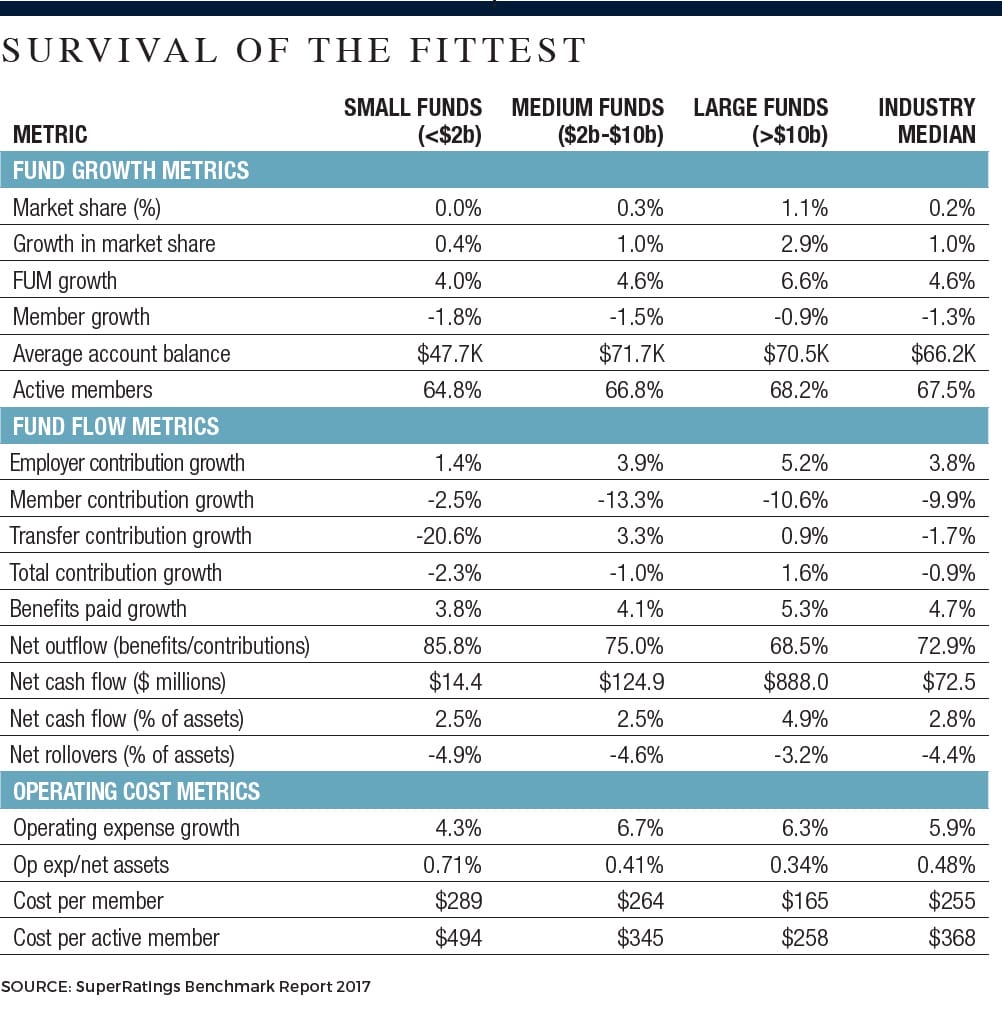

SuperRatings measured and compared funds across five areas that it considers key to assessing whether providers are meeting the scale test: membership growth/loss, net inflow/outflow ratio, net benefit to member outcome, fees, and net operating expense ratios.

About 23 per cent of funds surveyed were found failing on most of those measures.

The bulk of funds, 68 per cent, were ahead on most metrics but behind on some. Only 9 per cent of the funds surveyed were found to be ahead in each of the five areas.

APRA deputy chair Helen Rowell has stated publicly, on numerous occasions, that the name scale test should not be misinterpreted as meaning that the regulator thinks bigger is necessarily better. However, she has also repeatedly voiced concerns about the “long tail of sub-scale funds” that continue to exist without any viable strategy to improve the value they can offer members.

The SuperRatings research shows that while bigger isn’t always better, it is certainly true that smaller funds are more likely to be struggling to pass the scale test.

SuperRatings chief executive Adam Gee tells Investment Magazine many of the products that lagged on all five key metrics of the scale assessment were small funds (defined as those with less than $2 billion in assets under management).

“The majority are industry-specific funds, many of which are still named in awards. Most are smaller not-for-profits, but there are also some reasonably sized funds”, he says.

One of the entities that lagged on all the metrics is a larger fund with about $15 billion in funds under management.

Gee warned that MySuper funds struggling to meet the scale test were in an even more precarious position than struggling Choice funds. This is because the loss of default status could “spell the death knell” for them. This is poignant amid the ongoing government ordered Productivity Commission review into alternative default fund selection models.

Gee also noted, however, that some diseconomies of scale do exist in funds with larger membership bases, particularly in terms of the ability to tailor an insurance design, provide financial advice and offer personalised servicing.

Higher costs

The SuperRatings’ Benchmark Report 2017 highlights some of the strongest headwinds to hit the industry in the financial year ended June 30, 2016.

Average fund member growth was down 1.3 per cent in 2016. Overall, the industry has endured an average decline in membership of 0.9 per cent, per year, for each of the past five years.

“Negative membership growth has become the new normal for superannuation funds as account rationalisation continues,” Gee says.

Over the same period, total contributions to the median fund fell 0.9 per cent. Employer contributions grew just 3.8 per cent in 2016, compared with 6.1 per cent a year earlier. Gee says this was due to the stagnant superannuation guarantee rate and benign wages growth. In addition, member contributions fell by nearly 10 per cent over the year, on the back of market and regulatory uncertainty.

“In particular, we noted a drop off in contributions post the 2016 budget, as concerns about the sustained generosity of super tax concessions were heightened,” Gee says.

“Transfer contribution growth is also becoming harder to come by, with the median fund recording a 1.7 per cent fall, driven by its non-recurring nature.”

This is because fewer members are consolidating their super into one fund, thanks to the success at getting so many of them to do this in the past.

Meanwhile, Australia’s ageing demographics contributed to a growth in benefit payments of 4.7 per cent, which easily outpaced inflow growth and resulted in a median net outflow ratio of 72.9 per cent. That means that, on average, the industry paid out 72.9 cents in benefit payments for every dollar of inflow funds received in 2016. Outflow ratios tended to be much higher at smaller funds, while many of the larger funds still attracting new members reported net inflows.

Another challenge for the industry last financial year was the 5.9 per cent growth in the median fund’s operating expenses – following a rise of 3.3 per cent the previous year.

In the recent past, rising operating expenses were masked by strong investment returns, but this was no longer the case in 2016, as the post-global financial crisis run of double-digit average returns came to an end.

“As we now live in a low-growth environment, where net asset growth is more uncertain, one must question how funds will continue to fund similar levels of increases in operating expenses going forward,” Gee says.

He explains that larger funds with access to economies of scale were typically spending more on their brands, advertising, analytics, member segmentation, compliance, risk management and new product development.

These initiatives all help them better attract and service members – but at a cost.

“Whether a for-profit or not-for-profit, the undeniable fact remains that superannuation funds operate like any other business, such that revenues must at least be sufficient to offset expenses, and where this does not occur, one has to question a fund’s sustainability.”

Consolidation inevitable

Gee says that, given the pressures facing so many funds, and the slow pace of industry consolidation, the regulator should take a more interventionist approach.

“Consolidation over the next few years is inevitable,” Gee says, “And rather than giving a bit of a push, APRA will need to come in with a bigger stick to force some funds to move down this path.”

He blames the “self-interest” of many directors for blocked mergers.

“We’ve worked on a couple of mergers over the past six to 12 months and they’ve come to nothing because boards don’t necessarily want to give up seats and executives don’t want to lose positions.”

APRA’s Rowell made a similar observation at the Conference of Major Superannuation Funds in March. “We continue to observe considerable reluctance by boards to acknowledge that it is in the best interests of their members to pursue a merger or wind up their fund,” Rowell said.

Amid the calls for more industry consolidation, a number of small funds have been vocal in defending their right to exist, and have cautioned that mergers do not always lead to better outcomes for members.

“Mergers are expensive to implement, do not always provide benefits to members and can be detrimental to the interests of existing members,” NESS Super chief executive Angie Mastrippolito says.

She says NESS – a micro industry fund that manages just $626 million – accesses benefits of scale through its outsourced providers and provides a valuable niche service.

“We can have more direct contact with members and thus provide a more personalised service delivery,” she says.

Gee agrees that scale can be imported by using third-party providers; however, the ability to differentiate a fund’s service offering is becoming more difficult, with funds spending significant amounts on data analytics and member segmentation in order to deliver a more tailored experience for members.

Others warn that without scale it will ultimately be too hard for tiny funds to stay afloat, putting their members’ retirement security at risk.

“The competitive advantage of knowing members better may be getting eroded through the strong investment by other funds in technology to create efficiencies and increase service capabilities,” REST Industry Super chief executive Damian Hill says.

REST is a $39 billion industry fund that, while not under pressure to merge, could accelerate its growth by convincing smaller funds to transfer their members into it.

Hill says if the government wants to encourage mergers, it should scrap plans to end the temporary capital gains tax relief on fund transfers from July 1, 2017.

The Productivity Commission’s recently released Draft Report Superannuation: Alternative Default Models suggests that the over-arching criteria for assessment and inclusion as a default fund should be net returns.

SuperRatings analysis shows which providers would be most likely to sit within the “List of 10” default funds if this approach were adopted. In alphabetical order, they are: AustralianSuper, BUSSQ, CareSuper, Catholic Super, Cbus Super, Hostplus, QSuper, Rest Industry Super, Telstra Super and UniSuper. All are medium to large funds.

Leave a Comment

You must be logged in to post a comment.