OPINION | In the current housing market, allowing young people to tap their compulsory superannuation balances early to buy their first home would aggravate lack of affordability. But that doesn’t mean there might not be merit to the idea further down the track.

I am working on an academic research project, through the School of Risk & Actuarial Studies at the University of New South Wales, regarding how to engage people in developing and using a sensible financial plan.

By sensible, we mean that it would take all important financial choices into account. What to earn? What to spend? How to invest – including for housing?

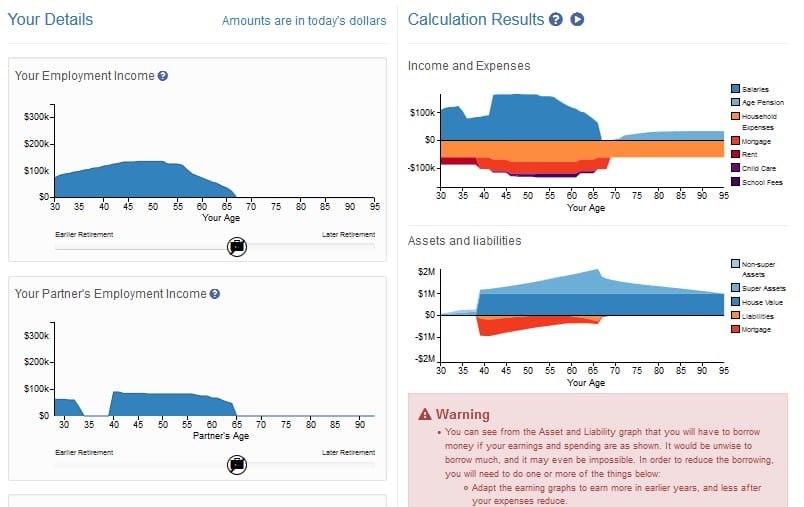

The objective is to calculate a plan that will provide a standard of living that is more less level throughout life. We have developed a prototype planning calculator that can be found at draftfinplancalc.com.

Of the 891 respondents whose visits to the site have been analysed, 361 said they were homeowners and 421 added a home to their financial plan. Sixty-eight of them experimented with different dates of home purchase. The sample is not necessarily representative, but the results are hardly surprising; many people would like to include a home purchase in their financial planning.

When mortgages and superannuation are included in a financial plan, however, one finds people are likely to have significant superannuation balances at the same time that they have large mortgages and are subject to onerous mortgage repayments. This provides the argument for allowing those aged under 45 to use their superannuation to reduce their mortgages. But with house prices high at the moment, it would probably be counterproductive, driving them even higher.

Consequences of compulsory super

In the longer term, however, it is worth considering the consequences of making superannuation compulsory at the same time as people are wanting to buy a house and have children. Our calculator shows a red warning when these objectives clash, because it creates an unsustainable debt. For couples who want children, something must give:

- They can have their children later, but that can become difficult.

- They can delay buying a home, but they may really want it for the extra space when the children are young.

- They can earn more, but longer hours create more stress when children are at home.

The solution most people adopt – and have always adopted – is to spend less when the children are at home. The consequence is that spending can increase when the children leave home. Alternatively, if people have become accustomed to the lower standard of living, they can retire early.

Data from the Australian Bureau of Statistics does suggest that people retire when they are financially secure. ABS figures show that 30 per cent of those who retired before 60 had a household income of more than $1000 a week, against 26 per cent of those who retired later.

It is, therefore, not surprising that people are generally not interested in saving for retirement until the children have left home. They have more important financial priorities.

But failing to plan financially has its costs. Many people never engage and make critical life decisions with inadequate consideration of the financial and long-term consequences.

Developing an overall financial plan does not have to be a huge exercise. It would be best if super funds could encourage their members to begin planning when they first start work – certainly before they have children – and to nudge workers to continue to update their plan as they get older. The incentive to do so would be much higher if people had more power over how their superannuation was used.

Benefits of using super for first homes

Apart from the pressure it would place on current housing prices, the advantages of allowing superannuation balances to assist with home ownership are considerable:

- People would have a strong incentive to develop their own financial plans.

- They could have children earlier and in their own homes.

- They could spend more throughout their lives, by saving more after children and retiring later.

If and when the housing bubble bursts, this would be a great policy to have ready in the back pocket.

Anthony Asher is an associate professor in the School of Risk & Actuarial Studies at the University of New South Wales Business School.

Leave a Comment

You must be logged in to post a comment.