I was once interviewed by a personal finance press magazine on retirement planning, and was asked the following question: “What is the biggest mistake that people make when planning their retirement?”

My concise answer: “Trying to calculate their life expectancy and base their plan on that.”

That reply surprised the editor, because it was at odds with traditional thinking.

But later I elaborated that no matter how many factors you may take into account, like whether you exercise regularly, your family history and so on, it amounts to a gamble to attempt to guess your date of death and such a gamble can have dire consequences if you guess wrong.

Exceeding life expectancy

We all know people whose lifestyle and health are such that they were not expected to live very long, yet some of them continue to live on well past life expectancy.

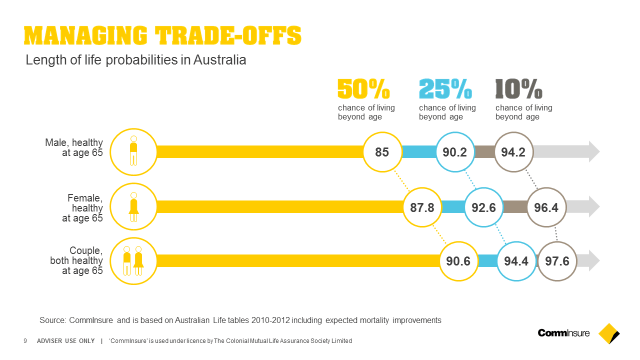

A more prudent approach is to prepare for maximum probable lifespan (i.e., the age where there is a one in 10 chance that you exceed), not merely prepare for your life expectancy. An even safer approach is to ensure you have enough money saved to fund your maximum possible lifespan, because otherwise, you’re still taking a gamble.

Addressing the uncertainty of our lifetimes is the most important challenge of retirement planning. If you use the standard population mortality tables to estimate life expectancy, you will have underestimated your lifetime, on average, about half of the time.

That’s because roughly half of all people die before reaching life expectancy, and half live beyond it, often far beyond it. To base a retirement plan on average life expectancy would be foolhardy because everyone is an individual, not a population. It would be sort of like playing Russian roulette with a two-shooter. Not too many people play that game.[1] Unlike an insurer, individuals don’t have the luxury of ’diversifying’ the timing of their death across a large number of people of similar age and of relying on the Law of Large Numbers to reduce the variation around their own timing.

Speaking of insurance, when one purchases life insurance to provide an inheritance in case they die prematurely, through pooling large numbers of people, an insurer can offer a policy that costs much, much less than if you were trying to accumulate such a financial legacy without insurance, especially during the years prior to reaching life expectancy. That’s because through risk pooling, an insurer can price policies based on averages. For example, a 25-year-old has about a 1 in 1000 chance of dying during the year. By pooling numerous 25-year-olds, an insurer can charge them, for example $100 each plus administrative expenses and margins, for $100,000 of coverage. It would require much more saving to amass such a legacy without insurance.

Managing the risk of uncertain lifetimes

Another financial contract is available in Australia that is designed specifically to handle the risk of uncertain lifetimes. It’s called a lifetime income annuity, and is most often sought by people preparing for, or already in, retirement. The contracts are priced as if you were an average healthy person at the time of purchase with a life expectancy typical of those who buy annuities.

Through pooling large numbers of people, a provider can charge merely what it would require to cover the investor through to that average life expectancy, plus a margin, yet generate enough contributions to provide an income throughout the remaining lifetime, regardless of how long it takes before passing away.

Helping to secure your retirement with annuities

Here’s the bottom line – for a 65-year-old person in decent health to have enough retirement money to securely last throughout their remaining life, they need to start thinking about providing for adequate retirement income to at least age 95 and a couple to age 98 and beyond[2] . Planning for retirement needs to last the distance.

Extract from David Babbel and CommInsure whitepaper, Retire stronger – new strategies towards a comfortable retirement, 2017. You can access the paper via www.comminsureadviser.com.au/retirement

[1] Attempting to project one’s own lifespan, if you correctly evaluate enough factors, may reduce the odds to those of a three-shooter, or perhaps even a four-shooter, but basing a retirement plan on that is still unwise.

[2] Source: CommInsure and is based on Australian Life tables 2010 – 2012, including expected mortality improvements.

Disclaimer:

This is general information only and does not take into account your individual objectives, financial situation or needs. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision.

‘CommInsure’ is used under licence by The Colonial Mutual Life Assurance Society Limited ABN 12 004 021 809 AFSL 235035.

Leave a Comment

You must be logged in to post a comment.