Large industry funds are most prone to member exodus if they do not lift their service standards soon, as researchers warn consumers now have lower tolerance for engagement failure in a choice-based environment.

Speaking at the Investment Magazine Chair Forum earlier this month, founder of research house CoreData, Andrew Inwood, said service quality has become increasingly crucial because funds have been less and less able to differentiate purely from a performance perspective in the past five years.

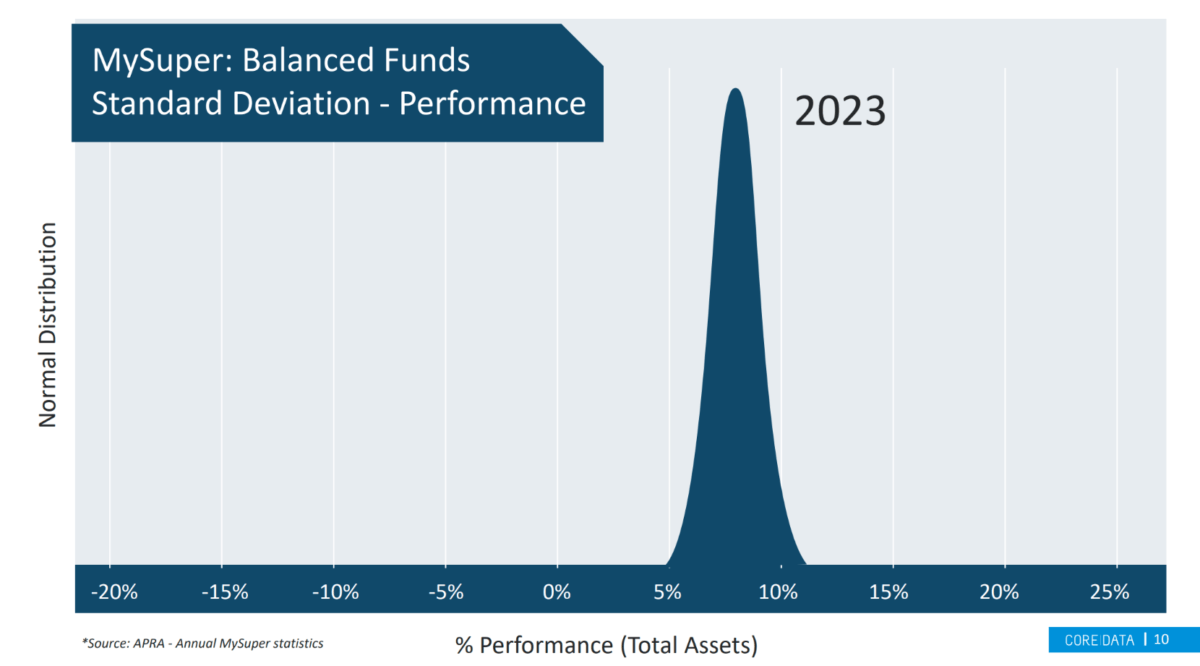

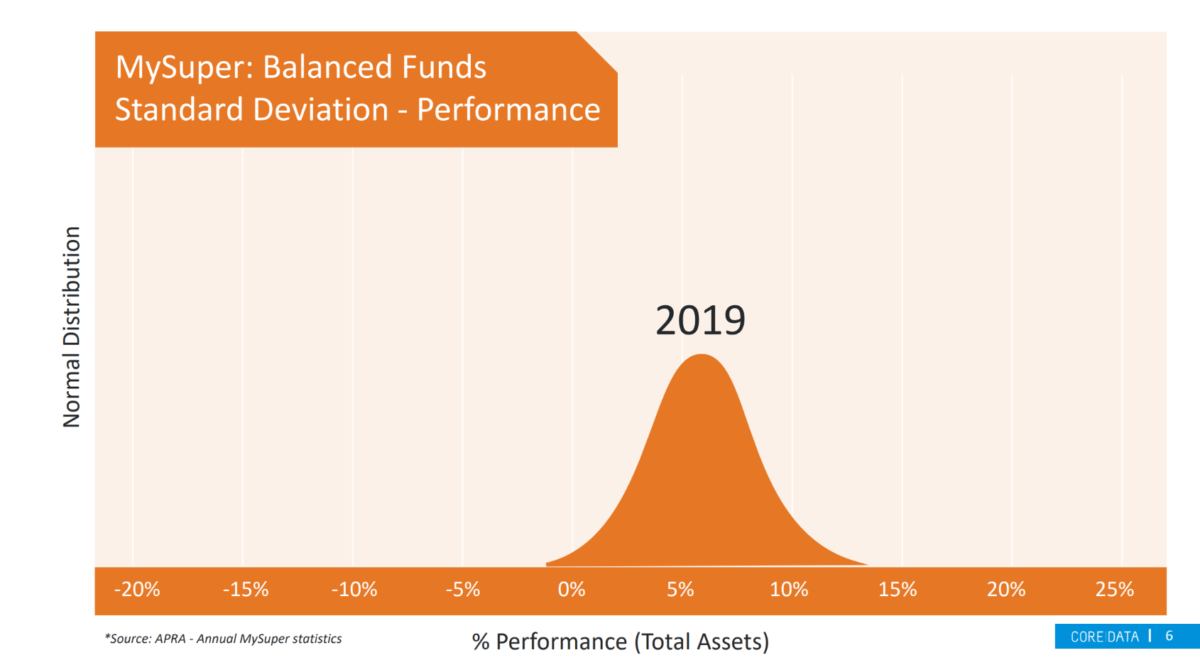

The company’s research found there was a 15 percentage points of difference in return between the best and worst performing MySuper products in 2019. But in 2023, that difference was only around 5 percentage points and significantly compressed the spread of returns.

“The effects of legislation and impact and homogenisation in the market has absolutely narrowed the outcome,” Inwood told the crowd in Sorrento, Victoria.

“The differentiation between the offers has become really complex, because they’re not priced particularly differently, the performances aren’t particularly different anymore, and the options aren’t particularly different anymore.”

This has resulted in members shifting their focus from performance to other areas of offering, which is exacerbated by the fact that many accounts are moving from the accumulation phase to the decumulation phase, leading to higher service expectations and more personalisation.

If these expectations were not met, members will be quick to make the switch, he said.

“[Members think the retirement phase] is all about me. And as soon as it becomes about people, then service starts to become important,” Inwood said.

“The Irish goodbye is a phrase we use when someone leaves a party without saying goodbye… and that’s starting to happen in superannuation.”

The comments follow research conducted CoreData and Conexus Financial (publisher of Investment Magazine) last year, which showed there are very different stories with member retention even within the industry fund space. Among respondents who said they are thinking about switching super funds, 12 per cent were with large industry funds and 8 per cent were with small industry funds. This is higher than retail and corporate funds, which each accounted for around 6 per cent.

But micro industry funds were the outliers as they only claimed 4 per cent of respondents who are flight risks. Their members are “unbelievably sticky”, Inwood said, and it is likely because micro funds can afford the time and resources to service their members on a more intimate level.

“That’s a function of scale, and solving that [service need] at scale is going to be something really interesting in the future.”

Looking ahead, Inwood cautioned trustee boards against underestimating the level of engagement from members, as significant in the past few years like COVID-19 has given many people a chance to re-evaluate how super can be a part of their financial plan.

“I’m sure that you’ve all seen the AFCA numbers where the complaints are going up and up and up and up – that’s not a function of the funds doing something bad. That’s just means engagements going up,” he said.

“The funds people have been complained about aren’t particularly bad funds. They’ve just got a lot of members.

“That’s going to be a function of fund size… and it’s going to be something really problematic.”

For more information about the Conexus/CoreData research, including fund-specific findings, please contact commercial director Ben Thomas at ben.thomas@conexusfinancial.com.au

Leave a Comment

You must be logged in to post a comment.