Australian superannuation fund members are billions of dollars a year better off than members of the average global pension fund, thanks to the Australian funds’ success in driving down investment costs, new research has revealed.

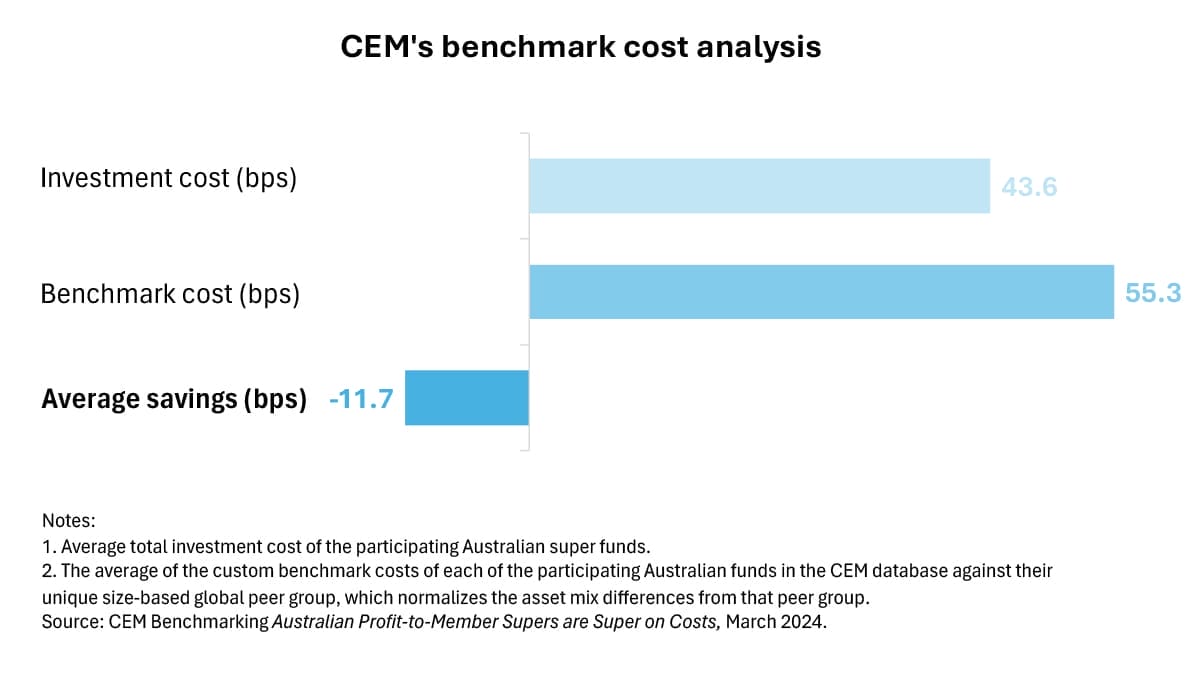

CEM Benchmarking’s Australian Profit-to-Member Supers are Super on Costs report covers 11 super funds that account collectively for about $917 billion of members’ savings. It has found that the funds are on average 11.7 basis points a year lower-cost than the global pension fund average.

That translates into more than $1 billion accumulating in members’ accounts every year, just for the 11 funds covered.

The report says the calculation of investments costs excludes transaction costs, but includes base manager fees, performance fees for public and private market asset classes, internal investment management costs, investment governance, operations, and support costs.

The report says the calculation of investments costs excludes transaction costs, but includes base manager fees, performance fees for public and private market asset classes, internal investment management costs, investment governance, operations, and support costs.

Australian superannuation funds are using their clout and negotiating power to drive down costs, with CEM saying savings are “partly due to using lower cost evergreen/core fund structures in real assets, and more prominently, due to lower external manager fees in public and private market asset classes”.

CEM’s Toronto-based head of business development Mike Heale says the impact of a regulatory focus on costs, initially through the Your Future Your Super performance test, is now beginning to propagate across the industry and across all funds and asset classes. Heale says the CEM analysis was conducted on the super funds’ entire portfolios, not just MySuper options.

“Several of the supers have just said this to me directly: that the regulatory focus on cost has had an impact,” Heale says.

“I would say it’s now having an impact more generally across the market. That’s where…the focus probably started to be really more cost-conscious.”

But Heale warns that continuing to just drive down costs may not be in members’ longer-term interests if it means funds avoid relatively costly, though potentially rewarding, opportunities.

“There’s a point to be made that you can focus too much on driving costs down,” he says.

“I’m not sure where that point exists. If you’re not able to access some opportunities that might reward your members more, then there’s a disadvantage, perhaps.”

CEM Benchmarking product manager Palwasha Saaim says the cost analysis of funds takes size into account.

“For each one of these supers we identified a peer group that was similar to them in size, and then we assessed their costs against that peer group,” Saaim says.

“For each one, we’re looking at their cost and cost efficiencies against a peer group that’s relevant to them in size. So small supers are not being assessed against large, or large versus small. In that manner we are taking the any economies of scale, or diseconomies of scale into account.”

Heale says some Australian superfunds are renowned as tough negotiators when it comes to hiring external active managers, and that’s producing benefits across the sector.

“It creates a culture where even…the non-tough negotiators get some reward, because managers just have to offer lower rates to make sure that they’re competitive in the Australian landscape,” Heale says.

Saaim says members of Australian super funds are reaping the benefits of their funds not only being good negotiators, but also choosing relatively lower-cost implementation options to begin with.

“There’s an implementation approach they have taken on top of what they’re paying to their managers,” Saaim says.

“Within real assets, we see that instead of going with fund-of-fund type structures, or committing to general partners, they’re invested more in open-ended, core real-asset funds, which tend to be generally lower-cost than, for instance, direct GP funds or fund-of-funds.

“Not only are they paying lower fees, but they’ve also consciously made a choice to pick an implementation approach that is generally lower cost.”

The CEM report says that in addition to cost savings passed on to members, the funds analysed also generated positive net value added (NVA) over the 12 months to June 30, 2023.

The research firm defines NVA as the difference between a fund’s benchmark return and the actual return realised, net of all investment costs.

“NVA is the sum of both manager value added within asset classes, and tactical portfolio decisions across asset classes,” it says.

“It has the advantage of being relatively agnostic to asset mix, enabling comparisons across funds.”

CEM says the median NAV for the funds covered in the report was “close to the short-term global median”, but Saaim says CEM had access to only one year of performance data.

“It is safe to say that they have added value,” Saaim says.

“But generally, when you’re looking at net value added, you’d rather look at the long term.”

Heale says there is long-term empirical evidence in its global pension fund database that shows there is net value added by active management.

“But it’s important that you control costs,” Heale says.

“High-cost active management is not rewarded, but cost-effective active management is rewarded.”

Leave a Comment

You must be logged in to post a comment.