In a speech last month US Securities and Exchange Commission (SEC) chairman Gary Gensler said the “basic bargain” that President Franklin Roosevelt and Congress laid out 90 years ago was that “investors get to decide which risks to take so long as those companies raising money from the public make what Roosevelt called, ‘complete and truthful disclosure’”.

Gensler was explaining how Roosevelt’s bargain with investors was being honoured by the SEC’s adoption of new rules to enhance and standardise climate-related disclosures by public companies.

However, less than two weeks later – in the face of multiple legal challenges to its “final rules” – the SEC announced it was staying their adoption, pending judicial review.

One of the groups taking legal action, the US Chamber of Commerce, claims the rules “undermine investor confidence in our public company system”.

Attorneys general from several Republican-led states also challenged the rules and earlier this month House Republicans used a House Financial Services Committee hearing to continue attacking them (see below).

For its part, the SEC says it will vigorously defend the validity of its final rules and looks forward to expeditious resolution of the litigation.

The avalanche of legal action comes despite the SEC having already caved into pressure by significantly watering down its rules. The biggest backflip was eliminating the proposed requirement for Scope 3 emissions disclosure.

That decision had already put the SEC out of line with other reporting directives and regulations like Europe’s Corporate Sustainability Reporting Directive (CSRD); the IFRS disclosure taxonomy, which Australia’s new climate-related disclosure regulations are based on; and the State of California, which all require Scope 3 reporting.

The SEC had also acquiesced by deciding only large (instead of all) companies had to disclose Scope 1 and Scope 2 emissions. And this would only now be “on a phased-in basis, and only when those emissions are material and with the option to provide the disclosure on a delayed basis”.

Intense lobbying

After intense lobbying from the Business Council of Australia (BCA) and others, the recently released legislative amendments for Australia’s climate-related disclosure regulations give Group One reporters an additional six months to get ready, with large corporations now required to start reporting from the first financial year commencing on or after 1 January 2025.

Australian asset owners (who are Group 2 reporters) will still need to start reporting from the first financial year commencing on or after 1 July 2026.

The BCA lobbied for the extension based on the arguably embarrassing admission that their members needed more time to get their climate “training wheels” on. One could ask why the wheels weren’t affixed some time ago.

Entities will only be required to disclose Scope 3 emissions from their second reporting year and will not have to disclose “exact data or detailed information that their customers or suppliers cannot provide easily”.

Continued uncertainty

How long the US judicial review will take is anyone’s guess but there is unlikely to be any judicial decision until late 2025. And even if the SEC wins there will almost certainly be appeals.

Under the climate reporting rules initially proposed, large listed companies needed to start reporting Scope 1 and 2 emissions from the financial year beginning (FYB) 2024. In its “final rules” this was pushed out by two years until FYB 2026.

Given a likely lengthy period of legal uncertainty, one wonders how much time and effort many US companies will be putting in now to prepare for compliance with rules that may never be enacted.

So if the SEC prevails there is a good chance it will decide it needs to further extend its reporting timeline because companies will argue they are not ready.

On top of this is the likelihood that if a Republican administration comes to power after the US elections in November this year there will be further efforts and calls to scrap the SEC rules.

This also flags an issue for Australia. If the Coalition were to win the next Federal election, which has to be held by May 2025, it is possible it may seek to wind back or amend the proposed regulations (which have been referred to a Senate committee that will report by 30 April 2024).

Commercially-sensitive opportunities

Whether it be in the US, the European Union or Australia, a big selling point of climate-related disclosure has been that it will provide asset owners and other investors with information and insights on climate-related business opportunities they are pursuing.

The explanatory memorandum for Australia’s legislative amendments says they will offer “clear visibility of the steps entities are taking to reduce their exposure to climate-related risks and embrace relevant opportunities”. Climate-related opportunities include things like the adoption of low-emission energy sources, the development of new products and services and access to new markets.

However, Australia’s disclosure regime will not require entities to disclose information relating to climate-related opportunities that are “commercially sensitive”.

According to the Australian Accounting Standards Board (AASB) – which is rafting a new Australian Sustainability Reporting Standard – an entity qualifies for the disclosure exemption if the information “could reasonably be expected to prejudice seriously the economic benefits the entity would otherwise be able to realise in pursuing the opportunity”.

According to the AASB omission will be permitted even if information is “material”.

An International Sustainability Standards Board (ISSB) staff paper on this question noted that “by definition, an exemption will result in circumstances when information about opportunities that is material for investors will not be disclosed resulting in incomplete information about an entity’s sustainability-related risks and opportunities”.

ISSB staff were also concerned the exemption “may be overused”.

It will be interesting to see what happens when/if a company notes in its climate statement (that will form part of the new annual sustainability report it will to have to produce) that it is pursuing, say, a potentially transformative climate-related opportunity but has decided not to provide any details of it to the ASX and investors.

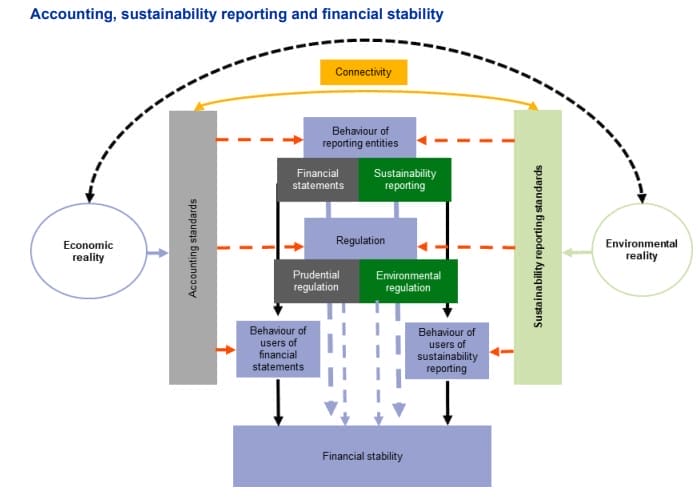

The same reality

With Australian companies soon to be publishing a sustainability report that will sit alongside the financial report, the question of how the two connect and complement each other is important.

This is a global issue and the European Systemic Risk Board (ESRB) has been examining it from a financial stability perspective.

“Connectivity between accounting and sustainability reporting standards is of paramount importance, as users of financial information and sustainability reports may otherwise receive contradicting information on the same reality,” according to the ESRB.

The ESRB recommends that when sustainability reporting explains the physical or transition risks arising from an entity’s activities and its assets and liabilities, such disclosures should be linked to the corresponding provisions that would be required in the financial statements.

“Sustainability disclosures may also provide early indications of matters that could subsequently be reflected in the financial statements (for instance, a commitment to net zero emissions could, over time, result in liabilities being reported in the financial statements),” it said.

The ESRB warns that delayed recognition of climate-related risks in the financial statements could contribute to “information shocks”, potentially affecting financial stability.

Interoperability

With the US, Canada, European Union, Japan, China, Singapore, Hong Kong, the Philippines, South Africa, Brazil, Australia and others recently adopting – or proposing to adopt – climate/sustainability reporting standards and with so many companies operating across country borders, the interoperability of the plethora of standards and regulations is a major issue.

These include the IFRS disclosure taxonomy (which Australia’s new climate-related disclosure regulations are based on), the European Sustainability Reporting Standards (ESRS), the Global Reporting Initiative (GRI), the Science-Based Targets initiative (SBTi) and the Partnership for Carbon Accounting Financials (PCAF).

Last month the Greenhouse Gas (GHG) Protocol secretariat released a report Detailed Summary of Scope 3 Stakeholder Survey Responses that noted respondents expressed being overwhelmed by the number of external standards and programs that have been launched in recent years.

Many respondents asked the GHG Protocol to “prioritize interoperability with third-party standards and clarify its compatibility with other frameworks and standards bodies”.

The matrix

Survey respondents recommended developing a “Framework Alignment Matrix” showing which external standards, guidance, frameworks, and programs aligned with the GHG Protocol standards and guidance.

Let’s hope this will not be a matrix where climate-conscious investors discover they are still trapped within a simulated reality.

The 25th anniversary of the first Matrix movie has just passed. In the movie, Keanu Reeves’ character Neo is offered a choice between taking the blue pill or the red pill.

Today, the scene may be asking us to whether we need to make a choice between hiding in the artificial world (of financial and climate accounting), or taking on the real world (where it is only real action that actually reduces emissions).

Leave a Comment

You must be logged in to post a comment.