While there has been much ongoing talk about the many challenges, difficulties and strange quirks associated with corporate reporting of scope 3 greenhouse gas (GHG) emissions, there have also been some timely reminders about why it is so important.

The International Investor Group on Climate Change’s (IIGCC) new discussion paper Investor approaches to scope 3: its importance, challenges and implications for decarbonising portfolios says that without access to scope 3 data for a company, it is not possible for asset owners to fully understand and assess an investee company’s contribution to climate change.

“Without looking at scope 3 emissions, many of the key drivers of global climate change might not be captured, nor attributed to companies who can influence these activities,” IIGCC says.

FTSE Russell’s fresh report, Scope for improvement: Solving the Scope 3 conundrum, says while scope 3 emissions is one of the most vexing problems in climate finance, “there is broad agreement that consideration of scope 3 emissions is indispensable to a clear-eyed assessment of climate risks for companies”.

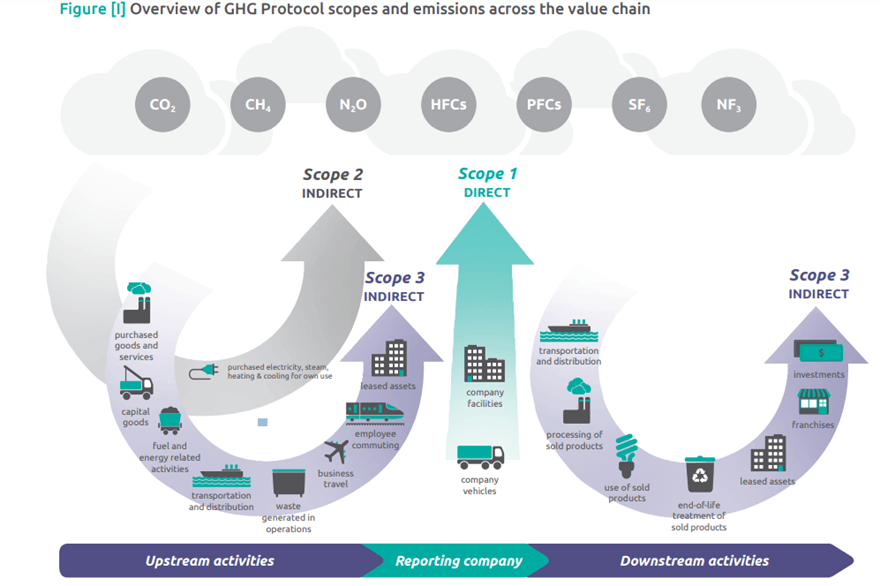

Scope 3 emissions – i.e. those that a company is indirectly responsible for up and down its value chain – on average account for over 80 per cent of corporate carbon footprints and so “accounting for these emissions is critical for investors to analyse transition risks associated with their investments and comply with net zero commitments and evolving regulatory standards,” FTSE Russell says.

However, FTSE Russell research suggests that less than half of the companies in a universe of more than 4,000 report on scope 3 emissions – and that less than half of those actually report on their most relevant or material scope 3 emissions (see diagram for scope categories).

In her What’s scope 3 good for? research paper Madison Condon, Associate Professor, Boston University School of Law, says scope 3 helps investors assess “how exposed an asset may be to changes in global or local climate policy, energy prices, or shifts in consumer and investor sentiments”.

Madison says “without (granular) Scope 3 data, investors might miss some of the easiest-to-decarbonize parts of a company’s supply chain, or some of its riskiest regulatory exposure”.

Scope 3 benefits

IIGCC says with material scope 3 emissions data, asset owners can:

- Clearly identify the emissions ‘hotspots’ within portfolios and understand the complete emissions profile of a portfolio or fund

- Focus asset-level engagement on the greatest opportunities to influence real economy decarbonisation

- Identify and capitalise on opportunities to influence decarbonisation across the wider value chain of a specific sector

- Better understand the transition risk and opportunity exposure of their portfolios and where it is concentrated in investments and/or segments.

IIGCC fears that when companies don’t have to include scope 3 in their reporting, they may be incentivised to lower their reported emissions footprints by simply outsourcing manufacturing activities or leasing assets instead of owning them outright.

“This would shift emissions out of their direct emissions (scope 1 and 2) into their value chain (scope 3) emissions. Including scope 3 enables a lifecycle emissions approach that allows for a complete and fairer comparison of value chains,” IIGCC says.

Condon is similarly concerned about excluding scope 3. She notes that a snapshot comparison of Apple and Samsung’s Scope 1 and 2 emissions would suggest that Samsung’s emissions intensity (by revenue) was dramatically higher than Apple’s, despite operating in similar product markets.

“This discrepancy is traced to Apple’s outsourcing of nearly all of its manufacturing, including partially to Samsung. Given the various ways scope emissions are used by the financial sector, excluding Scope 3 from oversight would likely induce firms to boundary shift and outsource many of the ways they traditionally use legal tools to escape legal and financial risk,” Condon says.

Outsourcing

FTSE Russell points out that it is left to the companies themselves to identify and categorise their sources of scope 3 emissions; to determine which sources to focus on; and then decide the degree of granularity with which to evaluate them.

“This results in heterogenous reporting practices, with companies rarely reporting against all 15 Scope 3 categories. Significant discrepancies also exist in how companies choose to classify emissions, leading to large inter-company variations.

“This makes it difficult to compare data across reporters despite efforts to gradually standardise accounting methodologies through increasingly granular sector guidance.”

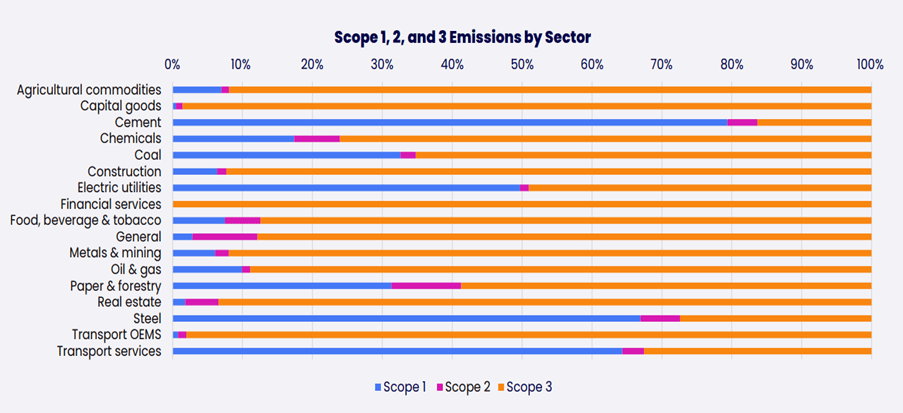

FTSE Russell says this also means scope 3 emissions face “significantly higher greenwashing risk” than scope 1 or 2 emissions. Reporters frequently omit the most material sources of Scope 3 emissions; and focus on reporting easier-to-measure but less material sources.

An example is ‘Category 6: Business Travel’ – 87 per cent of companies that disclose Scope 3 data disclose data for this category, though it represents less than 1 per cent of total emissions disclosed by all companies,’ according to FTSE Russell.

Condon says companies “bristle” at the idea of being held “responsible” for emissions over which they claim they have no control. However, she believes such claims, especially for large companies, should be met with scepticism.

“Those who argue against scope 3 say Apple, for instance, cannot demand that its consumers limit iPhone and iPad usage. But the point is Apple can in fact influence consumer emissions. It could design features limiting what the iPhone can do if it’s been charged off a dirty grid.

More impactfully, it could decide that perhaps all consumer handheld phones don’t need to be able to carry out machine learning using the most advanced chip. Or that it was going to embrace the ‘right to repair’ — and prioritize making equipment that easily disassembled for fixing and recycling”.

Investors are failing

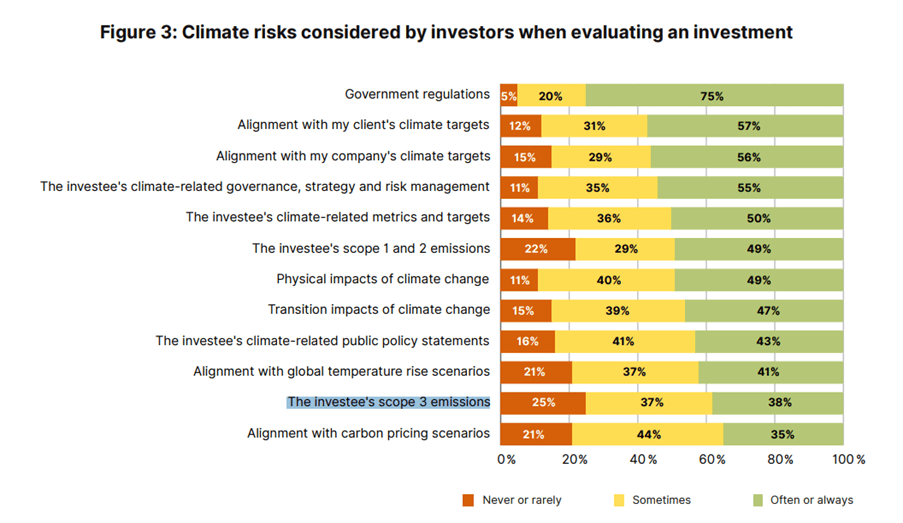

But companies are not the only culprits. Australian advocacy group Market Forces recently surveyed major asset managers and banks from the world, including in Australia, and found that investors are disregarding scope 3 emissions as a key indicator of regulatory and reputational risk.

Market Forces’ Investor Disconnect on Climate Risk report concluded that most investors don’t consider scope 3 emissions when evaluating investments – one-quarter of respondents reported they ‘never’ or ‘rarely’ look at scope 3 emissions when evaluating an investment, while 37 per cent said they only sometimes did this.

Similarly, when asked what factors indicate a high level of climate risk to an investment, ‘insufficient plans to reduce scope 3 emissions’ was reported by just 27 per cent of respondents.

Market Forces says given Scope 3 emissions are a key indicator of regulatory, market, reputational and thus material financial risk investors “are failing to fully consider exposure to risks they are most concerned about”.

Last month Treasury released its proposed legislation for Australia’s mandatory climate-related financial disclosures regime that will commence on 1 July 2024.

Scope 1 and 2 disclosure will be required in large company sustainability reports from the first year with scope 3 disclosure mandatory from the second year.

However, the government has shown little enthusiasm for promoting the scope 3 case. Scope 3 disclosures “would represent information that is available at the reporting date without undue cost or effort,” it says.

Treasury says entities will not be required to disclose against well-established and understood industry-based metrics until after 1 July 2030.

While scope 3 reporting progress is important it also important not be get bogged in discussions about data and accounting.

“We know where the worst emissions are, we just need to stop consuming, selling, investing in, and insuring them. This seems more like a governance problem than one for index tilting,” Condon says.

At the end of the day, the quality and integrity of a company’s scope 3 data is a less important investment signal than the quality and integrity of its senior management.

Leave a Comment

You must be logged in to post a comment.