In the past 15 years the gap between retail and profit-to-member fund fees has closed considerably, according to new research from Super Ratings.

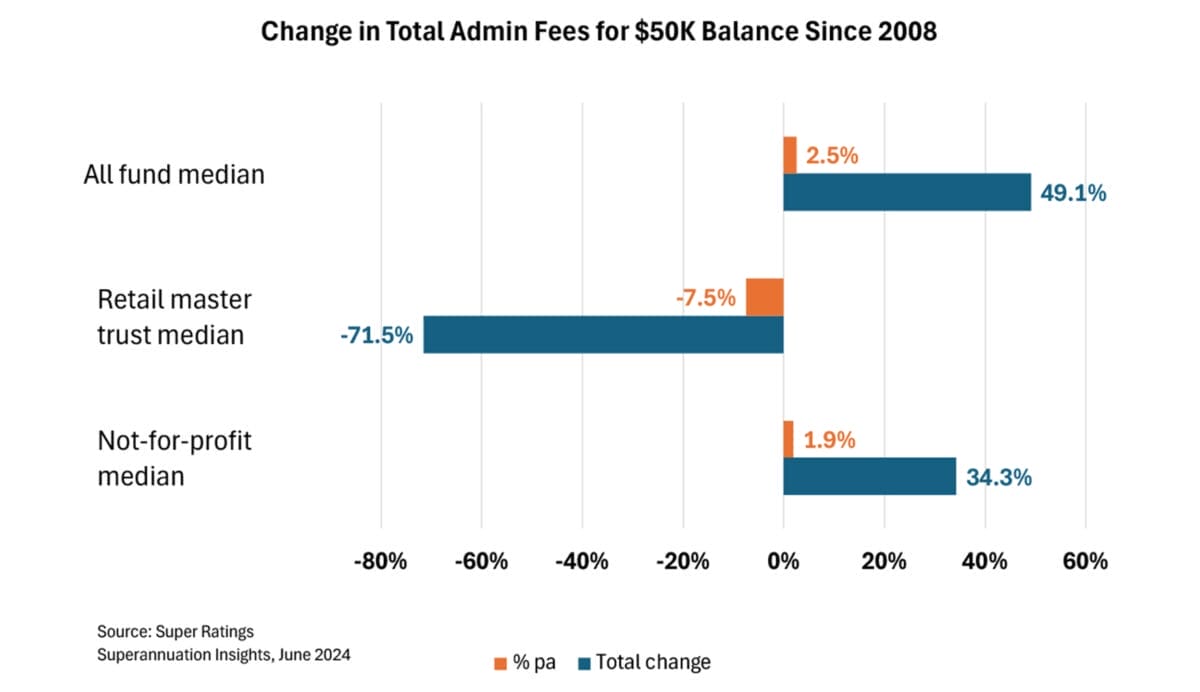

In its annual ‘superannuation insights’ released this week, the researcher found that since 2008 the median profit-to-member funds fee on a $50,000 account balance increased by $114 to $170, while the median retail master trust fee decreased from $730 to $208 over the same time period on the same balance.

Super Ratings executive director Kirby Rappell said funds used to be able to differentiate themselves on fees, but now it’s “fiendishly difficult” to do so.

“It’s a tale of two journeys through super,” Rapell said.

“What you’ve seen is through regulatory action [and the] removal of older, less competitive products from market, the admin fees for those retail funds is actually down 72 per cent now since 2008 on $50,000 balance. Conversely, not-for-profits – which will include corporate funds – are increasingly leading the market.”

Rappell said this is because profit-to-member funds have been trying to do “more things for people” which has a cost to it.

“Administration fees for that group is actually up 49 per cent since 2008,” Rappell said.

“What used to be a really big difference each year on admin fees is now about five or six basis points. It’s a completely different landscape funds are competing in and it means that there’s actually a big reset going on in the market, not just in retirement.”

The research found that two thirds of members eligible for pension products are retaining an accumulation account, which is worse than findings from SMSF administration provider Class that only one-in-two members in APRA-regulated funds are in a tax-exempt retirement stream.

Additionally, almost half (47 per cent) of members that are making retirement decisions chose to change their fund.

Rappell said pensions aren’t a product problem, but a service and guidance problem.

“There will be a small proportion doing a [transition to retirement] strategy but they’re actually a lot less common than they used to be,” Rappell said.

“There’s still a lot of people sitting in accumulation even though they’re over aged 65. It’s highlighting the challenges and the settings for how we transition more people to retirement.”

Dazed and confused

Super Ratings’ review of themes from annual member meetings found the most commonly asked questions centred around investment, with 83 per cent of funds being asked, followed by advice, with 76 per cent of funds asked questions by members.

Super Ratings research analyst Joshua Lowen said these questions were often personal in nature and not about the fund’s overall advice strategy.

“Investment strategy you’d expect members to be interested in, but we did find it interesting that the members still asked about it even though funds were talking about it in the presentation,” Lowen said.

“Three quarters of funds had some kind of question form members asking for advice. Funds can’t actually answer advice question in public forums but members wanted advice and it was pretty interesting that in the minutes reviewed there were funds that then sent financial planners to these members.

“It really highlights that for an engaged member, advice is really important and probably for a disengaged member advice is important, they just don’t know it.”

Rappell said members are genuinely confused about whether they want help or advice, and a lot of members don’t need full-scale holistic advice.

“They’re probably more looking for help, they just don’t know specifically how to ask for it, which is pretty reasonable,” Rappell said.

Advice in decline

Super fund members are resorting to asking for advice during annual member meetings amid a decline in funds’ advice offerings over the past four years.

The researcher noted the proportion of funds offering comprehensive advice has decreased from 71 per cent in 2019 to 59 per cent in the 2023 survey. For scaled advice that number has decreased from 76 per cent to 62 per cent.

The proportion of members receiving a Statements of Advice for scaled advice has increased slightly from 0.28 per cent in 2019 to 0.31 per cent in 2023, but for comprehensive advice it has decreased from 0.29 per cent in 2019 to 0.20 per cent.

Rappell said funds have improved on fees and performance but are finding it unsustainable to be able to offer comprehensive advice internally.

“There’s less super funds offering internal comprehensive advice, but I don’t think the demand for advice is necessarily going down,” Rappell said.

“It’s probably the places that the end super fund member needs to go to get that advice is shifting. It’s less likely that the super fund itself is going to be giving that comprehensive advice.”

Rappell said while comprehensive advice from funds might be in decline, intrafund or scaled advice centred around contribution levels, investment choice, insurance and some basic preparation for retirement is still utilised by members.

The cost of the advice varies, from being included in member fees to $500, Rappell said.

“That’s holding up and that seems to be the domain of where super funds are going to give you the simpler sort of advice but they’re playing less and less in that comprehensive financial planning space,” Rappell said.

A year ago, ASIC and APRA took super funds to task over their inability to fulfill their regulatory requirements under the Retirement Income Covenant to deliver a retirement income strategy for members.

The call for funds to improve their member engagement capabilities came amid the government’s Quality of Advice Review response which would allow super funds to hire “qualified advisers” to give scoped advice.

Leave a Comment

You must be logged in to post a comment.