Asset owners and managers may not always agree on fees, but one thing both parties are thinking a lot more about these days is creating innovative structures which – if done right – could provide rewards for the former and value for the latter.

Albourne Partners head of fintech and implementation Gaurav Amin said fees shape what a manager or an investor does from both an economic and behavioural standpoint. Albourne is a non-discretionary alternatives investment consultant.

Amin told the Fiduciary Investors Symposium at Oxford, hosted by Investment Magazine sister publication Top1000funds.com, that one economic impact of fees is on investment strategy.

“One of the big things which is going on right now is multi strategy managers who are using pass-through fee structures, effectively charging 7, 8, 9, or 10 per cent management fees,” Amin said.

“For them to earn that level of fee, or to justify that level of fee, what we have calculated is they need to be a third more levered than any other multi-strategy manager delivering the same level of return.

“Your investment strategy is being directly driven by the fee structure that you have.”

Behaviorally, fees influence how much risk managers take, and also impact the team-building and the culture of a manager organisation, which asset owners should consider when they are looking for long-term investment partners.

Amin said one of the common reasons why managers ask for high fees is to attract talent, but asset owners need to consider how the fee is distributed within the organisation.

“[Managers say] ‘talent is very expensive nowadays, and that’s why we want to create the higher fees.’ However, a team is more important than the collection of stars,” he said.

“How the bonuses are given out is quite important and drives the culture of the company. So, if you’re looking for a sustainable investment…that you are willing to live with for a long period of time, then having the right fee structure within the company itself can be quite important.”

Amin urged asset owners to consider the “three gripes” of fees when negotiating the next mandate with managers. The first one is the level of fees.

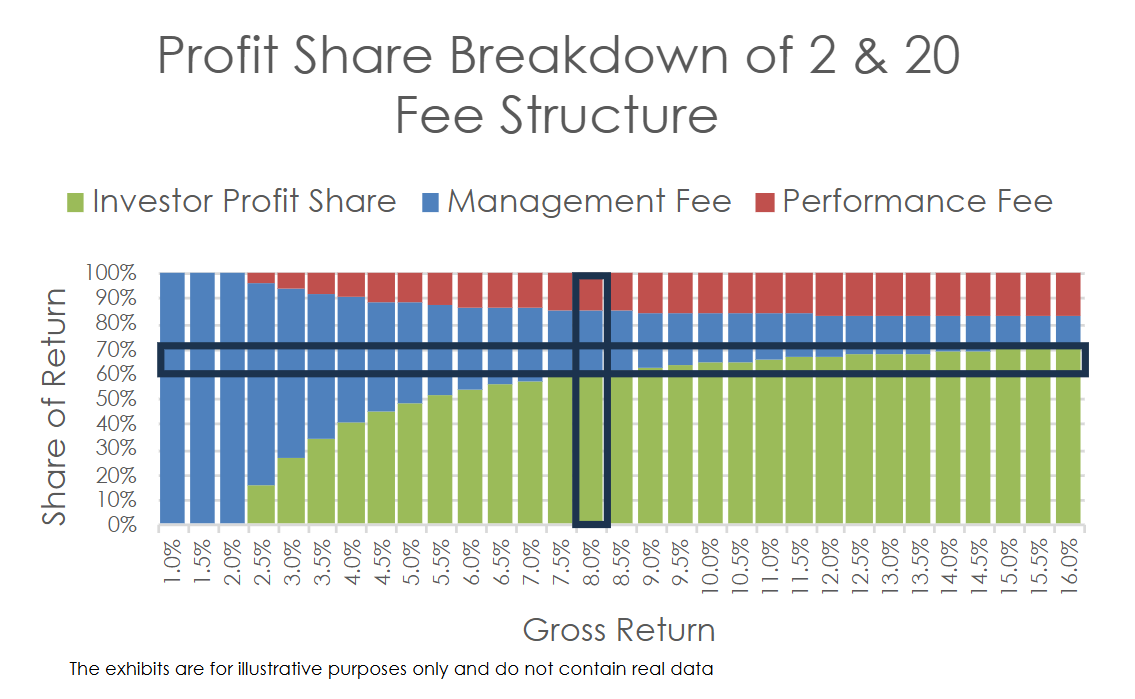

The problem with traditional fee models, such as a 2-and-20 structure, is that there is an imbalanced investor profit share. Albourne’s analysis shows there is likely to be an equilibrium of fees when investors’ share of profit reaches 60 to 70 per cent – below that range, investors may deem investment in a fund unworthy; higher than that range, managers may not be sufficiently incentivised. The level of fees is hence critical, because there is always the likelihood that investors will lose patience before it reaches equilibrium, Amin said.

The second gripe is the shape of the fee structure, where there are more nuanced opportunities for asset owners and managers to align their goals, Amin said.

For example, if asset owners are investing in a fund to provide a hedge, then there should be higher management fees and lower performance fees. If it’s a pure alpha fund, then asset owners should seek a higher performance fee and lower management fees.

The shape of the fee structure is also where investors can get creative with incentives for different types of managers. With hedge funds, there are levers such as high watermarks, crystallisation periods, and hurdles; for private market funds there are things such as carried interest, catch ups, and monitoring fees.

Amin reminded managers that “one fee structure is not going to solve all your problems”.

“Each investment – each investor – in the same fund could have a different objective, and therefore they have a different fee structure. So, it is up to the manager to offer those,” he said.

“That will help align the interest of that particular investor.”

With that said, however, no fee solution should come at the expense of the last gripe of fees, which is transparency. It is notable that different variables and structures often make fees difficult to measure and benchmark.

Amin said there might be a bigger role for consolidated metrics such as investor profit share (IPS) to play in fee measurement. He defined IPS as share of gross returns that the investor earns or is expected to earn for a given fee structure.

“This is where transparency comes in: how is the manager managing the money? And how much transparency are they giving you? Are they making those decisions for the fee structure or for the performance?” he said.

“That’s the collaboration that you need to have with your manager, to have that constant dialog saying, ‘you are doing these things for the right reason or the wrong reason’.”

Leave a Comment

You must be logged in to post a comment.