We are very supportive of the proposals under Tranche 2 of the Delivering Better Financial Outcomes (DBFO) reforms regarding delivery of financial advice by superannuation funds. The reforms establish a foundation for provision of financial advice to members who would otherwise miss out.

The need to make affordable financial advice more widely available and accessible is well-recognised, and a key motivator behind the DBFO reform process. The Tranche 2 reforms, particularly the provisions around “advice through super”, are a significant step in this direction.

Trustee direction as the missing piece

A key theme of The Conexus Institute’s retirement research has been that a range of “delivery mechanisms” are required to assist members into retirement solutions on the basis that members engage with retirement decisions in a wide variety of ways. We have argued that “trustee direction” – or the capacity of super funds to collect personal information and recommend a retirement solution to members – is the main missing component.

Underpinning our stance is that many members would benefit from – and indeed prefer – being provided with clear direction from their super fund. In its absence, they are left to either seek and pay for personal financial advice (many won’t) or directly engage in decisions for themselves (which many are poorly placed to do).

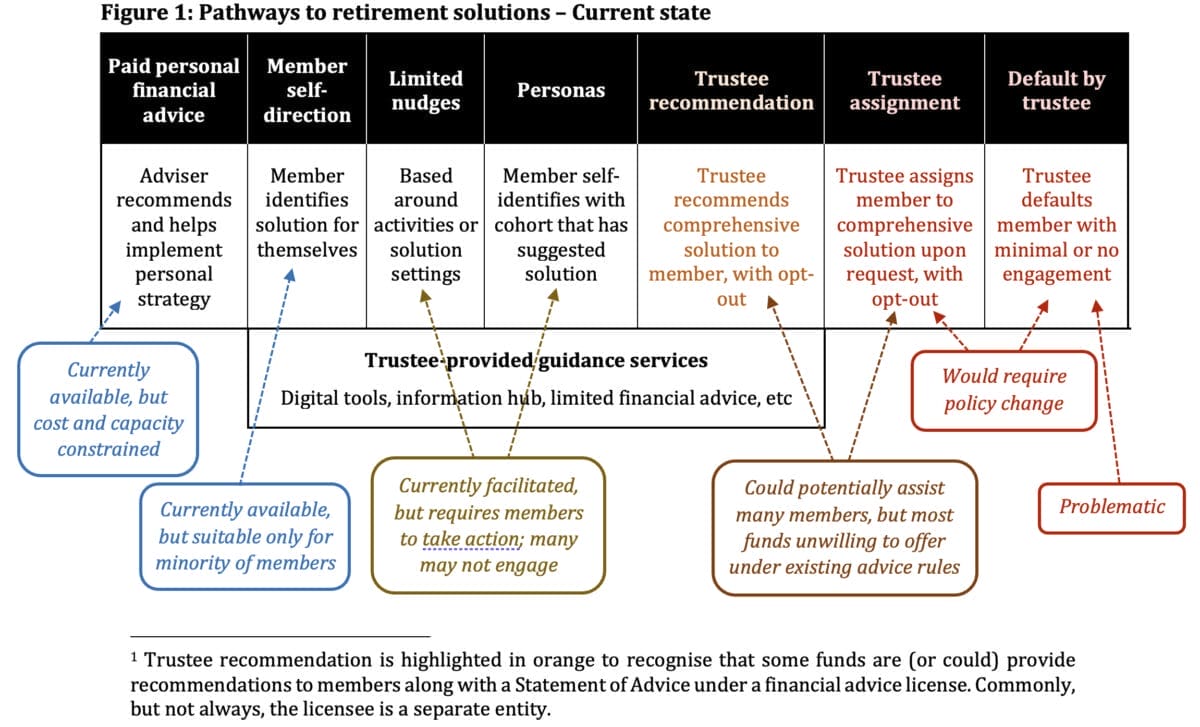

Figure 1 depicts the various pathways through which members could find their way to a suitable retirement solution, as viewed prior to the DBFO Tranche 2 reforms. The trustee direction pathways incorporating trustee recommendation, trustee assignment and default pathways sit towards the right. They appear in orange or red font (see note in Figure 1) to recognise a lack of availability.

In practice we view facilitating trustee recommendation in a scalable fashion as the most feasible way forward for getting a large number of retirees into appropriate retirement solutions, noting that trustee assignment and trustee default require adjustments to the regulatory and policy settings and default being problematic in any event for a range of reasons.

We envisage one way to make affordable financial advice around retirement widely available while removing the necessity for members to engage with complex decisions is through the following process:

- Member seeks a recommendation from their super fund.

- The trustee requests personal information from the member as required to identify a retirement solution that the fund offers which is most likely to be suitable for their needs.

- The trustee offers the retirement solution to the member, along with appropriate caveats (for example, what they assumed about the member) while providing an opt-out.

Our reading of the DBFO Tranche 2 reforms is that they set the foundations for super fund trustees to put the above three-step process into effect through two main mechanisms.

Mechanism 1: Defining the scope of financial advice that trustees may provide

The proposed provisions related to “advice through super” should provide clarity to trustees through setting clear boundaries around what advice topics may be addressed on a collectively-charged basis.

The provision that advice may only be given with respect to the member’s interest in the fund is generally a sensible and highly suitable reference point for defining the scope of trustee-provided financial advice. This establishes an interesting ‘one-way check valve’ boundary between trustees and advisers. Trustees cannot provide comprehensive financial advice (unless they establish a financial advice licensee) leaving this type of advice as the domain of financial planners. However financial planners can provide limited advice.

Establishing this boundary makes it clear to trustees that members with more complex advice needs beyond the scope of what trustees can provide should be triaged towards a financial adviser. We think there is greater scope for fund trustees to provide this sort of direction, even if it means the member leaves the fund. Given that triaging is not a product, it doesn’t sit naturally in the DBFO reforms. However it is an important area that warrants focus from policymakers and regulators.

Consolidation of multiple super fund accounts remains a difficult advice topic in the context of collectively charged advice. But account consolidation carries greater importance in the retirement phase given the process frictions around consolidating once a member has moved some assets into retirement phase. We think a mature solution needs to be identified.

Mechanism 2: Enabling trustees to collect and use certain personal information

Members cannot be safely provided with suitable recommendations without some knowledge of their personal circumstances. This is especially the case in retirement where differences across members can be fundamental to the retirement solution they require. In the absence of knowledge of the member characteristics that are critical to the decision, the risk of recommending an unsuitable solution can be significant.

By clearly establishing an appropriate list of what personal information may be considered by trustees in providing advice through super, the proposed reforms should provide trustees with assurance to collect and use certain personal information.

Guidance and advice after DBFO Tranche 2

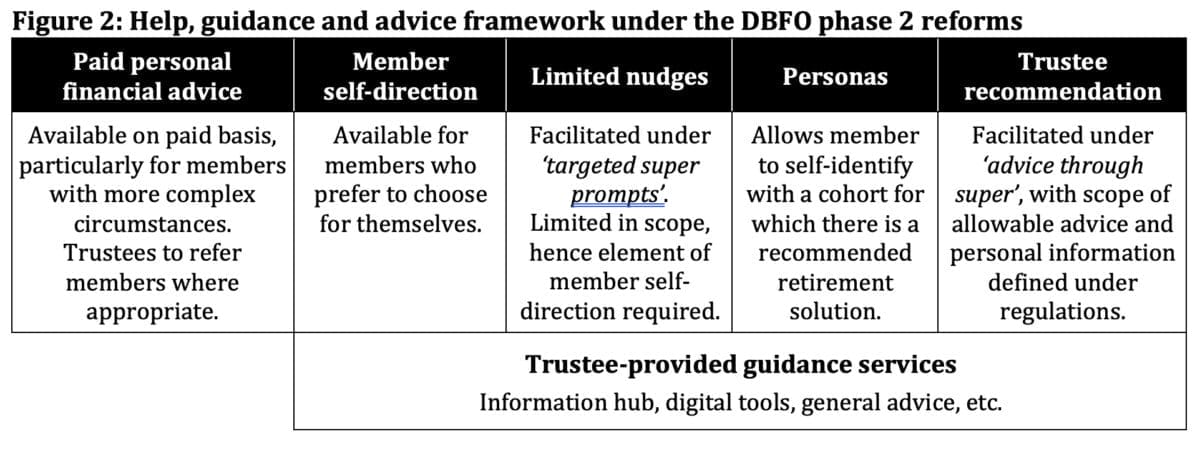

Figure 2 is our take on what the guidance and advice framework around retirement would look like under the DBFO Tranche 2 reforms. We believe this framework caters for the vast majority of retirees, with the notable exception of the totally disengaged who take no action upon retiring.

Scope to be defined under regulations

Another feature of the DBFO Tranche 2 reforms is that the scope of what trustees are permitted to do will be defined under regulations rather than by legislation. Regulation will define: allowable topics; persons to whom the advice may be given; and personal circumstances that may be taken into account. The regulation-based approach affords an element of flexibility.

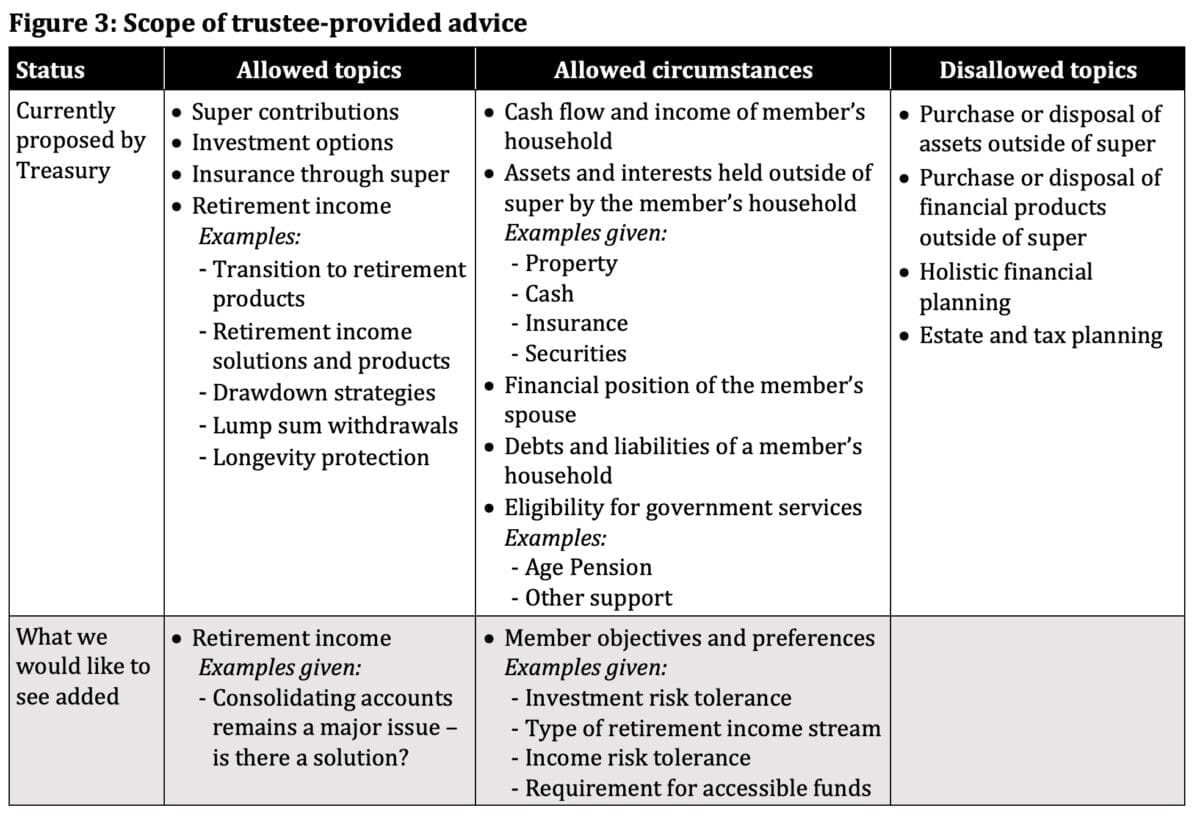

Treasury has released an Advice through Superannuation consultation paper that provides proposed lists of “allowed topics”, “allowed circumstances” and “disallowed topics”. These lists are summarised in Figure 3, focusing in on the parts most relevant for retirement.

We are quite supportive of Treasury’s proposed lists. The allowed topics include retirement and cover off on the key components of integrated retirement solutions (consideration of different products, drawdown strategy and investment strategy). The allowed circumstances account for key member attributes according to our analysis.

Two main things are missing, as noted in the last row. First, it would help if the allowable topics list facilitated a mature, practical solution for account consolidation. Second, trustees should be able to seek information on member objectives and preferences, otherwise trustees are left to make difficult assumptions.

Funds still need to rise to the challenge

The DBFO Tranche 2 reforms will pave the way for super funds to provide advice to members who may have otherwise received none. Incorporating member objectives and preferences into “allowed circumstances” would be a further improvement. Nevertheless, it is worth sounding some notes of caution.

Collectively-charged advice inevitably entails cross-subsidisation. We view this as a necessary cost for moving forward. The reforms won’t work well for all fund types, such as platform funds designed to support financial advisers. Super funds also need to rise to the challenge, operationally and from a governance perspective to ensure member outcomes are prioritised.

We hope that funds will make good use of an expanded capacity to better assist their members.

David Bell is executive director of The Conexus Institute.

Geoff Warren is research fellow of The Conexus Institute.

The Conexus Institute is a not-for-profit think-tank philanthropically funded by Conexus Financial, publisher of Retirement Magazine.

Leave a Comment

You must be logged in to post a comment.