One option raised in Treasury’s YFYS consultation involves replacing the existing test with a simple reference portfolio (SRP) approach. This might sound like progress for an industry jaded by the existing test. However, it creates hazards for funds, their members and the broader super system.

Reference portfolios are good for internal governance, but risky for formal assessment given the serious consequences of failure.

In considering how to improve the YFYS test we’ve explored a range of metrics, but generally on the premise that they form part of a multi-metric test. Any single metric test is deeply flawed. Do you know any investor who relies on a single metric to make an investment decision?

The SRP test would motivate benchmark herding at the asset allocation level, whereas the existing test encourages herding within asset classes. This would discourage a range of investment activities some of which the Government is trying to encourage such as nation-building investments in private markets. We are also concerned that this different type of herding behaviour may increase systemic risk.

SRP metric explained

A working understanding of the SRP test helps to comprehend the issues. We’ve published an explainer to assist industry with their deliberation and submissions and hit some highlights here.

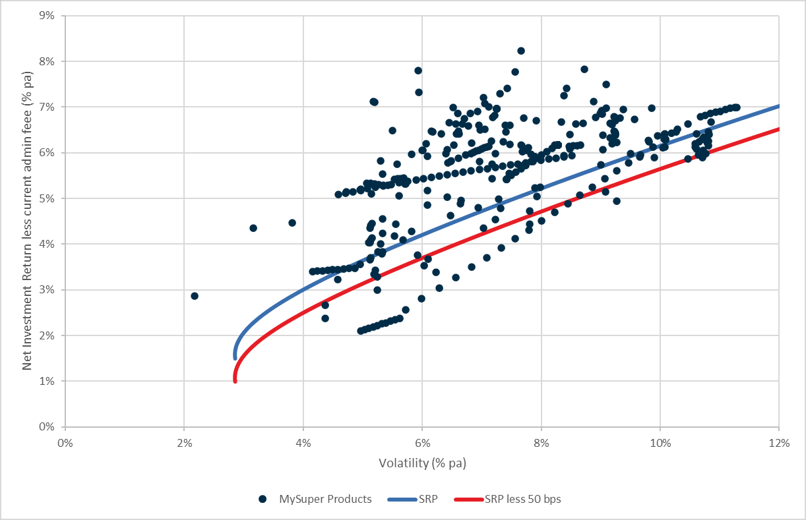

The SRP metric as envisaged would involve tracing out an SRP risk-return frontier of portfolios comprising various mixes of listed equities and fixed income with risk measured by standard deviation (SD). This is the blue line in the chart below. Total fund returns (the dots) are then compared against the returns for the portfolio on the SRP frontier of the same risk level. A fund fails if it falls below the nominated threshold below the frontier, i.e. the red line.

In concept the SRP approach has some attractive features. It assesses total portfolio returns, which is what really matters to members. And it adjusts for risk, the absence of which from the current test has been bemoaned by us and others.

Understanding super fund agencies

A primary source of unintended consequences arising from the YFYS test is the existential nature of failing the test for a super fund. Simply put, performance test risk equals business risk. Super funds treat the test as a hard constraint and will do whatever is necessary to minimise the risk of failure. Typically, this involves limiting performance test tracking error (TE).

(As an aside, we believe this partly explains why the industry dislikes multi-metrics: it becomes too difficult to measure and actively manage performance test risk.)

TE would reflect two components under an SRP test:

- Deviations in the asset class weights versus the SRP (reflecting strategic asset allocation, or SAA). Any asset classes outside of those in the SRP will tend to raise TE. This includes investments in nation-building activities in private markets that the government aims to better accommodate.

- Deviations from the indices within the SRP asset classes, i.e. equites and fixed income. This is a similar issue to that which exists under the current test but will be narrower in scope as the asset indices outside of equities and fixed income disappear from the mix.

Deviations associated with (1) are likely to swamp those from (2) in determining TE. Funds will be incentivised to pay closer attention to SAA weights relative to the SRP than the make-up of their equity and fixed income portfolios.

Funds could take the view that their existing investment strategies, most of which are far more diversified than the SRP, will outperform the test over the full period assisted by lower SD and not worry about TE. However, the risk of sizable underperformance remains real. This could encourage convergence towards the SRP.

APRA produces an SRP metric (although not perfectly comparable as it uses growth/defensive weights rather than SD as the risk proxy). Over three years the industry median underperformance is about 150bp per annum. This seems largely due to private market relative underperformance and difficult times for active management – trends that appear to be continuing.

To the extent that APRA’s estimates are indicative, many fund portfolios may be carrying 3-4 years of poor performance into future periods (i.e. tenuous future buffer) along with high TE to the SRP – a potentially dangerous combination. This may be moderated on a volatility-adjusted basis (an area we are investigating), but we suspect the point will stand.

Member impact

An SRP test will have detrimental impacts on members if it: (a) induces funds to move away from what are the best portfolios for members’ long-term outcomes, and (b) the changes prove costly. Obviously (b) is hypothetical, and we won’t know the answer for many years. We can consider (a), however.

The SRP test creates a motivation for funds to offer portfolios using fewer investment sectors outside of those which make up the SRP. By implication, trustees would be running these more concentrated portfolios now if they viewed them to be in members best interests. Yet most funds are choosing to run more diversified portfolios, with many allocating sizably to alternative assets.

Risk at the system level

We also hold system-level concerns. In State of Super 2026 we projected that the industry would double in size by 2035, meaning a much larger superannuation system footprint. It is important for individual funds to diversify the system rather than all look the same as super grows.

The current performance test (through its focus on benchmarks) combined with a strong peer group focus has acted to increase the similarity between fund portfolios, especially at the asset class level. Portfolios could become even more lookalike under an SRP approach if it motivates funds to focus their asset class mix on a smaller collection of assets. We are concerned by the potential for a sizable increase in systemic risk from further concentration under the SRP approach.

Lurking beneath something that looks like a small and somewhat refreshing change are potential risks for funds, their members and the system at large. We are not supportive of a switch to an SRP, or indeed any single metric. Unfortunately, we all find ourselves once again debating detail while bigger and bolder changes are required to make the YFYS performance test sustainable.

The Conexus Institute is a not-for-profit think-tank philanthropically funeded by Conexus Financial, the publisher of Investment Magazine.

Leave a Comment

You must be logged in to post a comment.