Jo Townsend, the chief investment officer at REST Industry Super, says the fund tries not to get caught up in the day-today noise of investment markets. REST is not only investing according to a long-term horizon, it’s willing to depart from the pack when making investment decisions.

“Our fundamental investment belief is that it is possible to add value through active investment management, and we do that through both the use of active investment managers and changes to asset allocation.”

According to Townsend, the widely stated belief that you can’t add value through active management, and moreover, that they are waste of fees, is contestable. “…We can actually demonstrate that the use of active investment managers has added real value for our members over long-term time horizons after the payment of active investment fees,” she says.

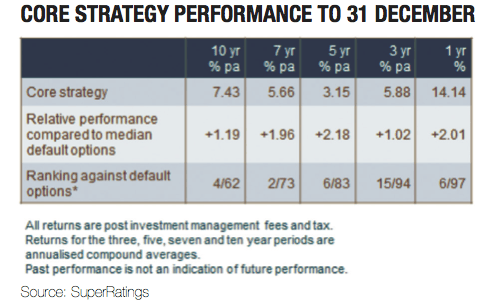

REST has internal reporting that shows they have been able to add value over asset class benchmarks consistently, by using active investment managers. For example, Australian shares are plus 3 per cent per annum over 10 years, and the overseas shares asset class is plus 2 per cent per annum over 10 years, both after all fees.

The core strategy is the only investment option to which REST applied its active approach to asset allocation. “These outcomes reflect both the use of active investment managers and our active approach to asset allocation,” Townsend says.

REST will also make changes to asset allocation that, at times, can be quite different to the activities of other funds in the industry, she says. “We will do that because we can see that risks exist in parts of the market where we’re not comfortable taking a certain level of exposure.” An example is the tech bubble of the late 1990s-early 2000s, when REST had a substantially underweight position in overseas equities – around 8 per cent compared to about 20 per cent in the industry.

A whole other class

In 2008, this led to the establishment of a new asset class to place the structured securities – the “credit opportunities” sector, which sits in the growth alternatives asset class. Townsend says the call has paid off for REST members. “Our initial allocation was 4 per cent of total FUM and today the allocation is 6.5 per cent,” she says.

“…Those assets have been some of our best performing over the past four years or so. So that’s been an example of where we’ve been prepared to be opportunistic and an early mover, and actually take advantage of fear that’s evident in markets at a point in time.”

It all relates to a longer term focus that Townsend identifies as a true differentiator for the fund, which is one of the largest super funds by membership – more than 1.9 million members – and funds under management just about eclipsing $23 billion.

While Townsend has been in the super funds space since 2002, she’s had experience as a boutique fixed-interest funds manager and started her career at Rothschild in the 1990s. Townsend was given the opportunity to take on a fixed interest portfolio management role at Rothschild, and she says the terminology of time frames for returns has changed since her investment management days. “When I used to manage bonds, short term was generally considered two or three years; medium term was five to seven years; and long term was 10 years.” Today, she says, trustee boards can often be very focused on short-term competitor considerations.

“The danger is that you can think that you’re not doing a good job on a three-year time horizon if you’re below median, which to me, is at odds with the whole purpose of superannuation, which is a 35-to-40-year investment.” The focus on competitive, relative, short-term returns doesn’t necessarily deliver good outcomes to members when they get to retirement, Townsend adds. “And we’re prepared to be different.”

Allocating assets

REST believes bond prices are stretched, and that there’s potential for an interest-rate rise to lead to capital losses in those markets. It’s a view that shapes the fund’s investment philosophy. “REST has viewed bonds as being an expensive asset class for quite some time and is defensively positioned,” says Townsend. “Further down the track, we see that there is the potential for inflation to return in view of the extraordinary extent of expansionary monetary policy being practiced right around the globe – which is effectively helping to keep bond yields so low.”

A prime focus for the fund, meanwhile, is real assets, which Townsend says REST is in constant search of, namely direct property and infrastructure investments. More specifically, it is looking for core properties with high levels of income and relatively stable income profiles with moderate levels of capital gains. “So, real assets, strong cash-flow generating; they’re the types of investments we’d love to get more into the fund. These types of assets generally have some form of inflation indexation or protection built into the income stream, which is valuable. However, Townsend says the fund doesn’t target a certain number of assets or certain dollars invested on an annual basis because it also comes down to cost.

“…While it’s always possible to buy good assets, it’s not always possible to buy them at the right price. And the longest term determinant of performance on any asset is generally the actual purchase price that you pay.”

Approximately 90 per cent of assets and 98 per cent of REST’s membership base are in a 25-per-cent defensive and 75-per-cent growth mix. Additional funds, meanwhile, are being driven into overseas equities. The fund also has one dedicated emerging markets manager, and many of its overseas broad-cap managers can invest quite extensively into emerging markets.

“When you look at our overseas equity – our total allocation – we will be overweight emerging markets compared to the MSCI All Countries Index.” Townsend acknowledges Asia’s growth, saying many of the fund’s managers see what’s occurring in Asia as the “real engine of global growth” at the moment. She believes the traditional way of looking at emerging market exposure through geographic exposure – such as through a custody report – is becoming less meaningful.

“Probably an improved way of looking at what your true exposure is to Asia and emerging markets in general is to talk to your managers about where the actual revenues within the portfolio are coming from,” she says. “Because you can have a US-based goods provider who’s actually getting 30 per cent of their revenue from China. But if you just look at geographic exposures, it’ll tell you that the company’s 100-per-cent domiciled in the US.”

Performance issues

Townsend says there are always trade-offs in terms of asset types. A mature asset with a high level of cash flow, which is CPI-linked, might have a lower return profile, but there is also development risk in infrastructure. This may involve the risk of approval and construction for a new asset, says Townsend, and would necessarily require a higher potential rate of return than if you buy an asset that is already built and producing income.

The fund reviews each asset class on an annual basis, which also entails a look at its manager line-up. Currently, the fund employs 42 external investment managers across 11 different asset classes.

REST will not terminate a manager because of short-term underperformance. “We will always look to make sure that we understand what is going on with a manager’s performance. There might be very good reasons that a manager is underperforming. “An absolute reason to terminate a manager would be if they’re not investing in accordance with their philosophy and the reasons they were put into the portfolio.”

As for how the fund is responding to industry change, Townsend says REST will be offering a My Super product, but the challenges will be around differentiation. She warns that people may think that the only really important consideration is low fees.

Townsend believes numerous providers will develop very low-cost passive investment products and will market on the basis of fees being all-important. Yet members in those products will not be getting better investment outcomes on a long-term time horizon, she says. “At the end of the day, the actual real consideration should be the returns that members end up with after fees.”

Leave a Comment

You must be logged in to post a comment.