Does ASIC’s MoneySmart website retirement income calculator produce estimates that contravene the Corporations Act?

Consider the following BBQ conversation:

Bill: “I’m retiring next month and was just using ASIC’s MoneySmart calculator to see how much income my superannuation will provide me”

Bob: “That is really of interest to me as I won’t be far behind you. What did you find?”

Bill: “Well, my $510,000 super balance will be my main source of retirement income and MoneySmart initially said I would get $49,000 each year.

Bob: “Is that enough for Jill and you?”

Bill: “Well not really, but MoneySmart has some levers I can play with to improve my retirement income. So after some trial and error, I found that if I changed my investment strategy to High Growth, my retirement income went up by 10 per cent to almost $54,000. Jill was happy with that as the extra makes it easier to visit her grandchildren in the UK.”

Bob: “Wait on, my fund’s High Growth strategy has more risky investments? Can you take that risk?”

Bill: “That’s what I thought, but I feel comfortable since ASIC is our regulator and they wouldn’t show such an improvement if it was much riskier.”

Ignore investment risk at your peril

The superannuation industry understands that investment risk can have a material impact on retirement outcomes since so much of the industry’s time is spent trying to diversify and reduce investment risk. Retirement income estimates that ignore investment risk may well lead members to take inappropriate decisions. Not only is this morally wrong and bad business practice, but such estimates would seem to be false in a “material particular or misleading manner”, as prohibited by, e.g., Section 1041E of the Corporations Act:

“A person must not …. make a statement, or disseminate information, if:

(a) the statement or information is false in a material particular or is materially misleading; ….

(c)(ii) the person knows, or ought reasonably to have known, that the statement or information is false in a material particular or is materially misleading”

ASIC’s MoneySmart website is not the only instance of ASIC permitting (even encouraging) such one-dimensional retirement income estimates.

ASIC also do this in their Class Order 11/1227 ASIC, which specifies a highly constrained formula that superannuation funds can use to report retirement income estimates. This formula is simplistic as it, inter alia, completely ignores investment risk. We have legal advice that superannuation funds do not have to rely on the class order to provide more sophisticated retirement income estimates. But the existence of the class order, and ASIC’s verbal guidance that we understand has been provided, have inhibited superannuation funds from providing their members with retirement income estimates that properly incorporate investment risk. This is a great example of “garbage in, garbage out”.

This means that the class order fails to promote sensible policy objectives; a point that we have made to ASIC in our submission to their consultation on this matter. (Available at http://ccfs.net.au/cvs/content/Submission-to-ASIC-CP203.pdf.)

Why include investment risk?

An individual’s financial tolerance to investment risk is highly idiosyncratic. And it changes over time. For many, the financial tolerance to investment uncertainty shrinks as they move towards and into retirement. This is the simple reason behind the commonly held view that many members should wind back investment risk as they age.

This common sense is violated by one-dimensional retirement income estimates that ignore investment risk. Regardless of age, such estimates show better outcomes for riskier strategies as illustrated in the above BBQ conversation.

In other words, the MoneySmart calculator is simplistic; it oversimplifies a complex problem; making unrealistically simple judgments. As Einstein is believed to have said: “Everything must be made as simple as possible. But not simpler.”

Moreover, this oversimplification is unnecessary. For example, three US firms, each associated with a Nobel laureate, provide clients retirement income calculations that include the impact of investment risk. Readers may recall one of these three, Robert Merton, as he has delivered some seminars in Australia where he touches on these issues. We are also aware of an entity in the UK and another in Australia that provide clients retirement income estimates which include the impact of investment risk.

These approaches use brute force computing power to generate many thousands of random futures which take into account investment risk. This can be quite slow. However, an alternative model that uses statistical mathematics to model investment risk makes it possible to produce retirement income estimates in real-time.

While some will find the maths behind such a model daunting, the estimates themselves will readily accord with common sense.

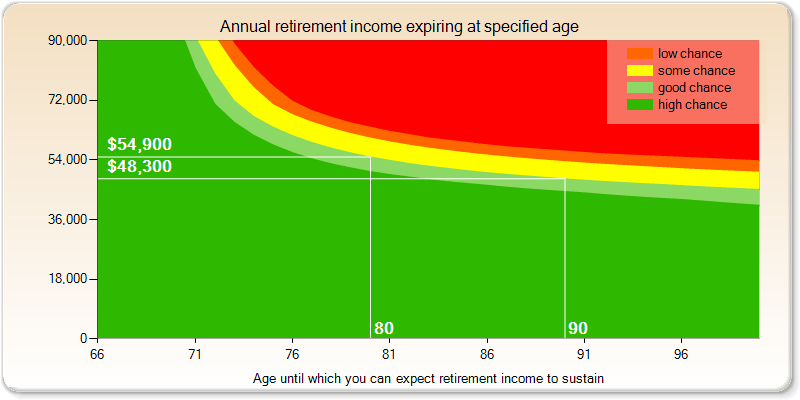

Indeed, a good model that incorporates investment risk will quantify and extend the member’s common sense. For example, we have devised the following diagram to assist members understand the three way trade-off between investment risk, longevity and a sustainable level of retirement income.

[Click on image to expand]

The different coloured regions reflect the likelihood of Bill (from the BBQ conversation) drawing a specified retirement income (shown on the vertical axes) to a specified aged (along the horizontal axes). In this case Bill has a good chance of drawing $48,300 to age 90. If Bill wanted to consider the income he has a good chance of drawing to age 80, the diagram shows it is $54,900. Essentially, the coloured regions demonstrate that future outcomes are uncertain. As Bill explores the impact of different investment strategies, he will observe that the width of the coloured regions will expand for strategies with higher investment risk and the “middle” yellow region generally moves up, and visa versa.

Such analysis provides members information to visualise the impact of the inevitable uncertain future. We believe that this is further assisting ASIC’s policy of increasing engagement with superannuation fund members.

We hope that ASIC (and some superannuation funds) stop providing simplistic retirement income estimates that ignore investment risk before too many members are misled. ASIC is right to encourage superannuation funds to provide more information about what a member’s superannuation will mean in retirement. But ASIC should also require this information to incorporate investment risk. It should lead the way with its MoneySmart calculator.

Leave a Comment

You must be logged in to post a comment.