Challenger’s annuity products are to form part of three super fund’s strategies to achieve a comprehensive income products for retirement (CIPR) through an income layering model.

CareSuper, legalsuper and LGS Super have all announced they intend to offer annuities to their members, backed by Challenger, by mid-2016, pre-empting proposed changes to the superannuation system flagged by the Government in its response to the Financial Services Inquiry.

Julie Lander, chief executive of CareSuper, said a key criteria for going ahead had been ease of administration. CareSuper is bringing in the annuity options for members as part of a project to upgrade its offer for retirees, which until now had been a fund that largely replicated its accumulation default.

“After the GFC it has been clearer they are after certainty, key goals in retirement,” said Lander.

Andrew Proebstl, chief executive of legalsuper, said the partnership with Challenger would provide the fund with insights, knowledge and expertise which it could leverage off to make sure the products it rolled out were aligned with its particular members.

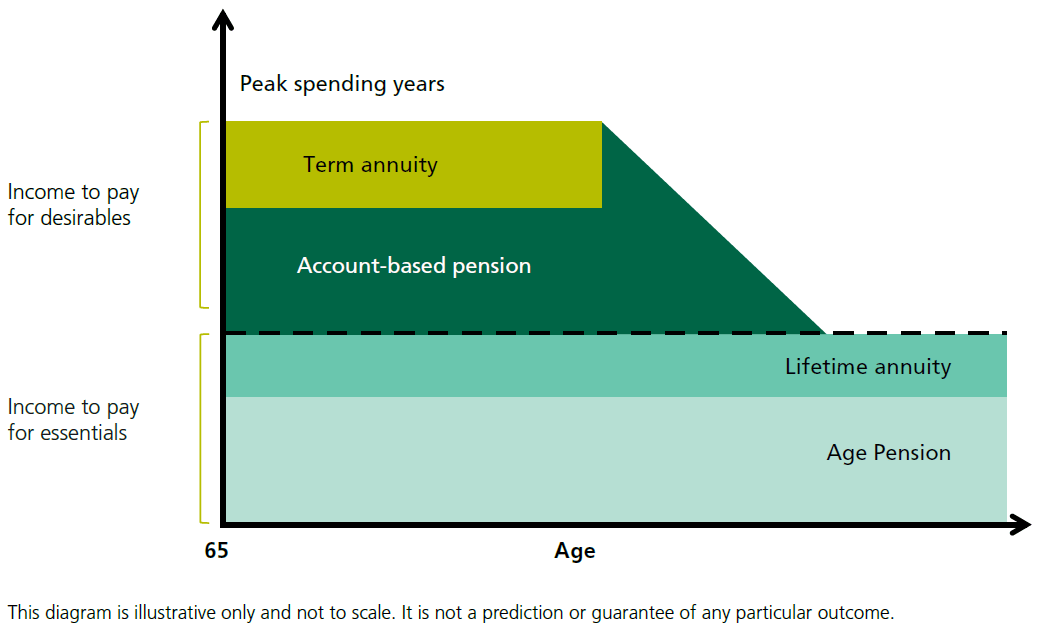

The annuity products are currently being designed by Challenger, in consultation with the super funds, and are to form part of an income layering strategy (see Figure 1, click to enlarge) in a member’s retirement.

The strategy splits income into two section; essential and desirable.

The income to pay for essentials is formed of the Age Pension supplemented or replaced by a lifetime annuity, ensuring that the base levels costs are covered for the member’s life.

The income to pay for desirables is made up of a fixed term annuity (ranging from 1 to 40 years) and account based pension, giving higher levels of income near the start of retirement as spending is typically greater in the early stages and lower in the latter stages.

With an increasing amount of members living more than 30 years past the date of retirement, the layering model allows for some assets to remain in growth options – a strategy considered prudent by many in the industry – while meeting current income needs.

As the needs of members are much more individualised in retirement, as opposed to accumulation where people can be more easily grouped, the exact levels of annuities and how they combine with other products needs be decided in consultation with a financial planner.

While Challenger will have designed the annuities, and will continue to back them, the super funds remains legal responsible for the products provided to members.

Paul Rogan, chief executive of distribution, marketing and research at Challenger, said: “Legally this product is issued by the fund and fully integrates in to the fund’s systems. The product has the same entitlements as if you were to buy a challenger annuity directly. Importantly for the member it allows them to get this regular and stable income stream and longevity risk integrated in with their account based pension.”

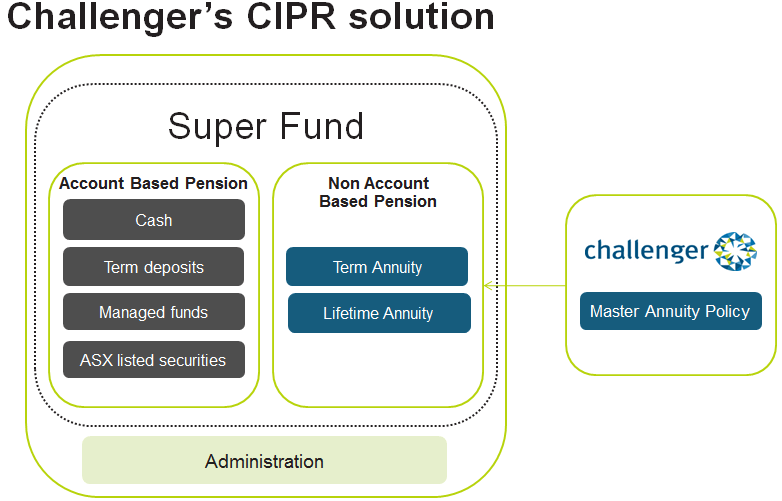

Challenger’s alliance with the Australian Administration Service (AAS) was another important factor in the super funds taking on the products.

AAS, a leading administrative platform serving the industry fund sector, will handle the implementation on behalf of the super funds ensuring that payments from the account-based pension and the annuity products are processed into the member’s bank account (see Figure 2).

The three super funds approached Challenger separately with no mention of using their purchasing power to secure a deal.

Leave a Comment

You must be logged in to post a comment.