Of all the issues Australian Institute of Superannuation Trustees (AIST) chief executive Tom Garcia could have addressed in his opening speech to the Australian Superannuation Investment Conference last month, he chose to focus on advice.

Garcia didn’t speak about the challenges of a low-interest rate environment, nor on lacklustre returns from equities. He didn’t address the geopolitical concerns that could affect investments – such as the Chinese economic slowdown or the upcoming US election.

Rather, he spoke about the challenges and opportunities that major superannuation funds face delivering high-quality advice to members and helping them achieve their goals and objectives in retirement.

Garcia told the conference that the superannuation industry as a whole has “done an extraordinarily bad job of communicating the investment expertise filled within each fund.”

But that is changing as major funds, driven by legal and fiduciary responsibilities and by unstoppable demographic forces, find increasingly innovative and cost-effective ways of helping members negotiate the transition to retirement with dignity and financial security.

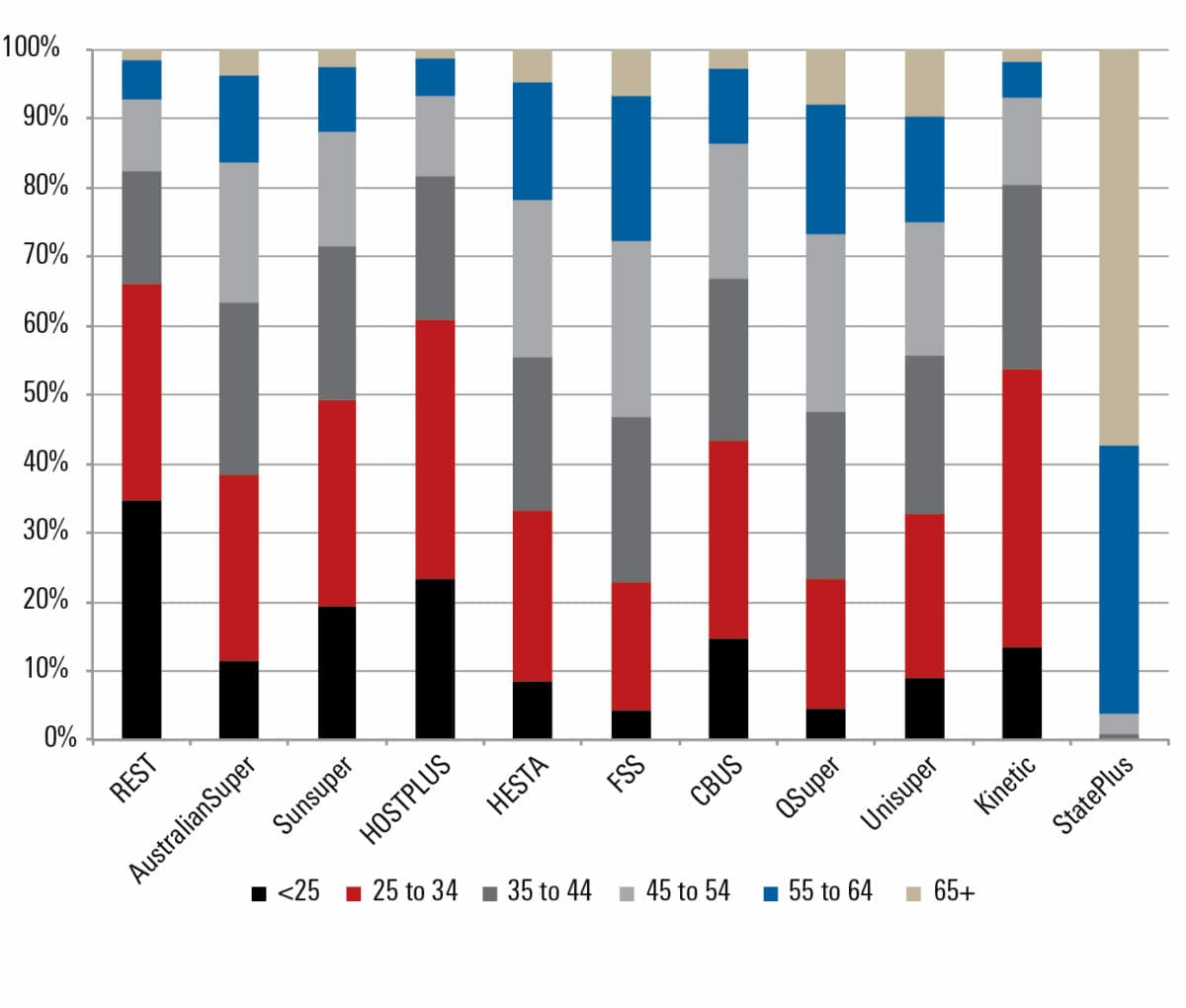

All funds are facing pressure to develop advice offerings, though for some the need is perhaps more clear and present than for others. For example, more than 80 per cent of members of REST are aged under 35 (see graph) – firmly in the accumulation phase and therefore likely to have relatively simple advice needs.

All funds are facing pressure to develop advice offerings, though for some the need is perhaps more clear and present than for others. For example, more than 80 per cent of members of REST are aged under 35 (see graph) – firmly in the accumulation phase and therefore likely to have relatively simple advice needs.

But in the case of StatePlus, which provides advice to members of the NSW’s State Super, more than 90 per cent of members are aged over 55 and moving towards retirement or already in it, with the consequent advice needs and demands.

As funds develop advice offerings, they have found themselves in a position that puts them at a distinct advantage to other advice providers outside the superannuation sphere. Each of the 10 largest funds has more than 300,000 members; REST and AustralianSuper each have more than two million; and Sunsuper has more than a million. Large membership numbers allow them to create significant economies of scale and fund sophisticated advice businesses. Even relatively small providers, such as StatePlus, have invested heavily in technology to improve the efficiency of front- middle- and back-office functions and improve the quality of advice.

Funds are then able to carefully and smartly segment their members and develop advice offerings with precise relevance to each segment. And spurred on by legal and fiduciary factors, they are creating advice offerings that largely bypass the broader financial planning industry.

Those initial advantages are overlaid with some striking structural differences: fielding employed or salaried advisers; charging fees for service unconnected to product or to aggregating funds; and setting management benchmarks and key performance indicators on things like quality of advice, and Net Promoter Scores (NPS).

That stands in contrast with advice entities where significant time and energy is spent on marketing and finding new clients, where more activities are directed towards aggregating funds (in product or on platform) to generate a margin and drive revenue, and where, to a greater or lesser degree, product and product-related considerations impinge on advice conversations.

Jack McCartney, executive manager of advice and employer relationships at UniSuper, says the different starting point puts superannuation funds at an advantage to the wider advice industry, and the funds are keen to drive that advantage home.

“We have an amazing advantage,” he says. “But we knew with choice of fund coming on stream, where there’s going to be more competition, we’ve got to get leaner and probably more commercial.”

Understanding members’ needs and wants

Defining a relevant advice offering requires a deep understanding of members’ needs and preferences. For StatePlus it involved doing detailed research involving more than 2500 members. Jason Andriessen, general manager of marketing and financial planning, says the aim was to understand members’ “needs, wants and channel preferences.”

“And an objective was to produce a segmentation model that allowed us to see how these people, this market, clusters into smaller groups with like characteristics,” he says.

Andriessen says that in addition to traditional segmentation involving account balances, age and attitudes towards risk, StatePlus went “one step deeper … and we looked at attitudes and behaviours when it comes to making decisions around money and how, by extension, they would like consumer advice, and we saw that they clustered into four groups.”

StatePlus focused on two of those groups – so-called “outsourcers” and “coach-seekers” – and in addition “worked out six questions that we could ask every one of our clients and prospective clients to better segment where they cluster into that group”.

“We’ve rolled that out across the entire business and our digital framework as well,” Andriessen says.

“It’s produced a common language where we seek to better understand what [our clients’] decision making framework is. It allows us to better shape our messaging when we reach out to them, but it also enables us to better shape our advice offers. And on the basis of that research we did introduce a whole new category of advice, what we call ‘event advice’.”

Insights led to education hub

The country’s largest fund, REST, has likewise built its advice offering on deep insights into member needs and preferences.

“We do a lot of member research and a couple of things gave rise to us implementing [an] education hub on our website,” says Andrew Howard, chief operating officer at REST.

“One of those is that people have differing levels of confidence in their own financial literacy, and the other was that depending on what stage of life people are at, they are going to ask different types of questions.”

When a member visits the REST education hub they are asked how confident they are with their own understanding of financial concepts relating to super.

This allows REST to present the videos and articles in almost a Facebook-type timeline tailored to the individual, depending on whether they are at a basic, intermediate or advanced level of financial literacy.

“Members found that really engaging because it was a bit more personalised and gives them almost a first consultation on what things they should be thinking about, and makes what can be a very broad array of information quickly digestible,” Howard says.

“Some of our research tells us that our members don’t necessarily perceive that advice is for them because they have a different view of what advice actually is, whereas when we make it digestible and presentable through education and over the phone consultation, they find themselves on a good path,” Howard says.

“We are trying to develop our advice and education offer around those principles of easy access, self-serve and then get them access to professionals when they are ready for something that is more complicated.”

Access to financial planners

He adds the superannuation fund has a partnership with a group called Link Advice that gives them access to financial planners if needed.

“That happens most often after somebody had a chance to explore general advice questions or intra-fund advice questions over the phone, but if they need to go ahead and have a sit-down financial planning appointment we can organise that through Link Advice.

“If they do take advice that is more complicated, the first piece of advice request[ed] is at no cost.”

Hostplus has pursued a similar strategy. Paul Watson, group executive of business growth, product and advice at Hostplus, says they use digital advice to achieve small and early wins, which in turn builds trust. This increase in trust facilitated a feed-through into phone advice, which tackled intra-fund advice through to comprehensive advice, thanks to the embedded financial planner model it used.

The embedded model worked by having financial planners from Industry Funds Service (IFS) work alongside Hostplus call centre staff in the same centre.

“For all intents and purposes they are part of our family in providing advice to members,” Watson says.

“That model served us well for quite some time, but with the increase in engagement and the increase in complexity around both product and advice and strategy, we’ve moved to the next iteration where we insource our own financial planners and they are operating under an authorised representative model, with IFS taking on more of a dealer group approach.

AustralianSuper has 20 financial planners that are employees of the trustee, but licensed through IFS. They are salaried and do not receive any commission.

“A member traditionally would receive that face-to-face pre-retirement advice though that channel,” says Shane Hancock, head of advice and education at AustralianSuper.

“We also have an accredited advice channel. So currently we have 660 financial planners that are accredited with AustralianSuper, from a range of different licensees from across the country.”

Hancock says there is no way the internal advice team can service more than two million members, and the accreditation approach allows wider geographical coverage and more members to access the service.

Specialised advice

AustralianSuper also wants to make it easier for members to maintain and continue any relationships they may already have with external advisers.

And finally, AustralianSuper refers out to this channel in the cases where a member requires specialised or expert advice in a given area.

While superannuation funds only have a very loose appreciation of the details about their individual members, aside from age and account balance, there are some that buck the trend. Sunsuper has a membership of more than one million and a dedicated data science team to develop better products and advice through deeper understanding of who the members are, and what their needs are.

The insights from the team have already been used to redesign insurance products, following its discovery that one-third of people who claimed total and permanent disability were back at work within three years.

Now its team is focused on advice, following the board’s approval of a three-year strategic plan to improve the super fund’s capabilities.

“You don’t build an end-to-end advice platform overnight,” says Anne Fuchs, manager of retail distribution and advice at Sunsuper.

“We have a really very impressive team of data scientists that allow us to know our clients deeply – to use data in a way so that we are speaking to them as an individual and not speaking to them en masse.

“As we establish our advice strategy in 2017 and beyond, the behavioural finance and phenology will be integral – so, actually understanding what money means to somebody and their relationship with it. Is it for enjoyment? Is it for security? What does it actually represent to them? Because it is that which will actually form their view of how that money is invested, and on how much extra they are actually prepared to put away in super.”

Fuchs adds another advantage of using the data scientist team, is they know which moment to approach a member, with which component of advice, to make a material difference to their position.

However, the super fund is agnostic about from where its members get advice.

Similar to AustralianSuper, if one of their Sunsuper’s members wants to get financial advice from an adviser that is in their community the super fund is happy to partner with that adviser, as long as they are acting in the best interests of the client.

“That generally hasn’t been the status quo and position of an industry super fund,” Fuchs says.

More and more financial advisers

Currently, Sunsuper has a national advice panel consisting of 66 advisers that are spread across the country, to whom the super fund can refer its members.

“As demand grows we also want more firms. We’ve only scraped the surface in terms of promoting advisers and it is early days for us. Because this is so central to our mission and our purpose it’s going to be [the] focus of intent of everything that Sunsuper does over the next few years,” Fuchs says.

“What we need to do is actually integrate these advisers into our business, introducing them to our employee teams that are on-site, building trust and relationships so that they can seamlessly refer when the time arises.”

“Our CEO, Scott Hartley, often says that fees are important, investment performance is important, but that the one biggest thing that will determine the balance someone will retire with is their engagement as early as possible in getting the financial advice.”

The chief executive of Cbus, David Atkin, says it is “essential that members can access professional financial advice to ensure they get the best possible retirement outcomes.

“It’s important that funds have thought out how to proceed in this area to provide great service to the members and to minimise cross-subsidies,” Atkin says.

The head of advice and retirement at Cbus, Greg Harper, says the fund has done “a lot of work developing an integrated advice service model that includes advice over the phone and a landmark referral program with the Financial Planning Association [FPA] with 53 participating FPA Professional Practices and nationwide service coverage”.

Harper says getting the right performance planning measures in place is central to providing advice that is always in the best interests of members.

“We hear about commissions all the time and rightly so, where product incentivisation drives the wrong behaviour, and advice isn’t strictly in the best interest of the member,” Harper says.

“If you’ve got performance planning measures in place that drive the wrong behaviours, they are equally as bad – because essentially it drives product incentivisation. It influences a bias towards your own product, which may not provide advice in the best interests of the member.

“It’s lazy performance planning measurement as well.”

Harper says performance measurements such as the number of SoAs written in a month and additional contributions to a fund are just as likely to bias behaviour as straight cash incentives.

“The fundamental thing is that best interest test, and our service model that aligns with it: our performance planning measures on professional engagement, technical competence, follow-though and closure of actions – without a bias and without pressure,” he says.

“Great service, professional engagement, technical competence, having the right conversations and imparting your considered knowledge so the member can make more informed decisions are all critical ingredients for providing advice in our member’s best interest.

“Whatever the advice requirement is, we do – strictly in the best interests of the member. It’s unbridled, and not compromised.”

Removing ‘product incentivisation’

Harper says KPIs that may seem to be in the best interests of the member sometimes unintentionally are not. Others, however, obviously distort advice.

Removing all forms of product incentivisation and conflicted performance planning measures are critical in developing a holistic and integrated advice model for members. But the advice process needs to be untainted from start to finish.

“If you’ve got KPI on FUM and additional contributions and those dollar figures, how bad do you think that’s going to be in driving advice that’s compromised?” he says.

Harper says “we know that Cbus is a high performing fund, with all profits to members, strong returns over the past 32 years (since inception) and great services for members nationwide, but we are all obligated legally and ethically to give advice strictly in the members’ best interests.

“If that means taking money out of the fund…to eliminate debt, or to satisfy other personal requirements, or we don’t give advice to make additional contributions because the member doesn’t have surplus income or there are adverse impacts due to preservation issues…then that’s the advice we will give, because that’s in the best interest of our members.”

Serving members’ best interest is at the core of super funds’ advice offerings, but a clear benefit of sound advice is “definitely increased retention,” Unisuper’s McCartney says.

McCartney says the advice provided does not need to be particularly complex for the member/fund relationship to be cemented.

“Just having that relationship, so people know where to go when the time is right, is part of it as well – just educating them and letting them know we do have this wonderful service here that’s in their interests,” he says.

He says Unisuper tracks the quality of advice it provides by calculating a Net Promoter Score for each of its advisers, and this approach springs from a philosophy of “giving great service that is genuinely in the members’ best interest”.

“Probably what we do sell is our service. People know when they’re being sold something and can smell it a mile away and they’re over it.”

McCartney says a focus on quality frees up its advisers to focus on service.

“Advisers, if they want to spend two hours with somebody, they do,” he says. “They have enough time and if they want to go overboard they can, because it is always about the member – they know they have got to get a great NPS score.

“If you’re doing that and you’re doing it in an ethical way, then you’re going to run a great business.”

Leave a Comment

You must be logged in to post a comment.