Australia rightly prides itself on having one of the best superannuation systems in the world. But new research shows our global standing is slipping, and calls for bold policy changes to ensure an adequate and sustainable framework for future generations.

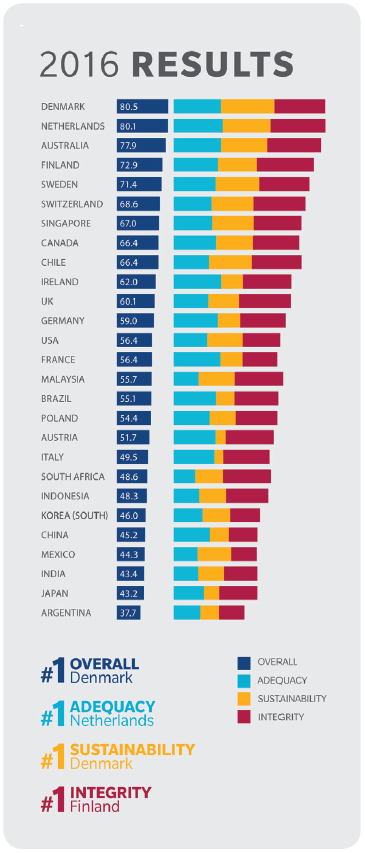

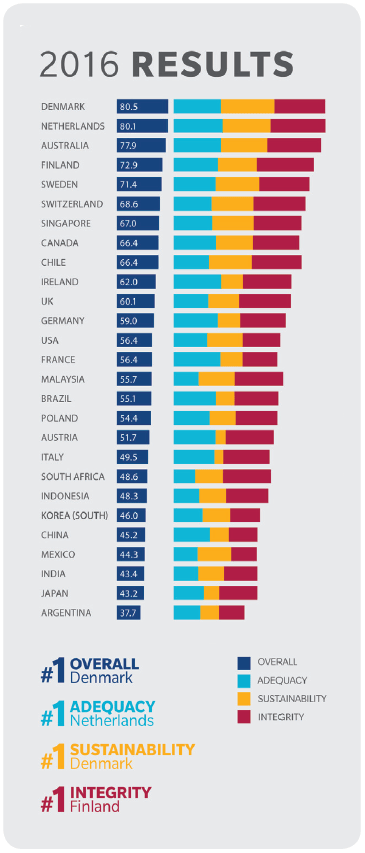

The 2016 Melbourne Mercer Global Pension Index, released in October, ranked Australia as having the third best retirement income system in the world.

Denmark was lauded as having the best retirement income system in the world, for the fifth consecutive year, followed by The Netherlands in second place. Denmark and the Netherlands were the only two countries to receive an A rating, with index scores of 80.5 and 80.1 respectively.

Australia received a B+ rating, but a slippage in our overall index value from 79.6 in 2015 to 77.9 hints at some worrying trends.

The Melbourne Mercer Global Pensions Index (MMGPI) is produced annually by international consulting firm Mercer, in partnership with The Australian Centre for Financial Studies (ACFS), which is a not-for-profit research centre of Monash University in Melbourne. In 2016 the MMGPI ranked the retirement income systems of 27 countries covering close to 60 per cent of the world’s population.

The MMGPI considers more than 40 indicators to compare the retirement income systems of different nations. The calculation of the index is split across its three sub-indices for adequacy, sustainability, and integrity.

Adequacy is afforded the highest index weighting at 40 per cent, followed by sustainability at 35 per cent, and integrity at 25 per cent.

Deferred rise in super guarantee

Professor Rodney Maddock of the ACFS, one of the authors, said the decline in Australia’s rating was largely due to a reduction in the nation’s “net replacement rate”.

For this the report pointed the blame at last year’s federal budget decision to defer a planned rise in the superannuation guarantee contribution rate.

Australia’s compulsory employer contribution rate is currently frozen at 9.5 per cent until 2021, after which it is scheduled to rise 0.5 per each year until it reaches 12 per cent in 2025.

The report made four key recommendations on how Australia could improve its retirement income system:

- Introducing a requirement that part of the retirement benefit must be taken as an income stream

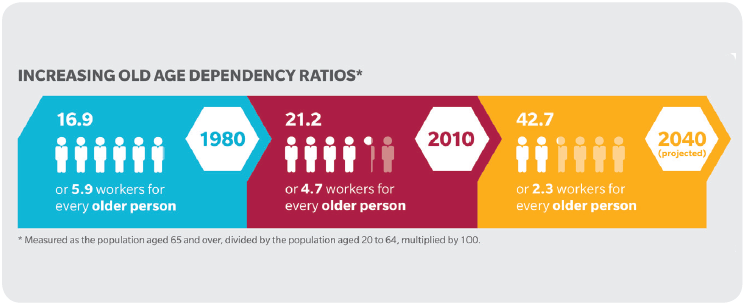

- Increasing labour force participation rate at older ages as life expectancies rise

- Introducing a mechanism to increase the pension age as life expectancy continues to increase

- Increasing the minimum access age to receive benefits from private pension plans so that access to retirement benefits is restricted to no more than five years before the age pension eligibility age.

These are all initiatives the Turnbull government has already shown varying levels of appetite for.

A plan to force all super funds to default retiring members into an opt-out account-based pension is well advanced. But moves to keep people working and restricted from drawing on their super for longer continue, unsurprisingly, to prove politically unpopular.

Mercer senior actuarial partner David Knox, lead author of the MMGPI, acknowledged that attempts to raise the pension eligibility and super preservation ages would always be political dynamite.

To combat this, he supports a push to have both linked to the five-yearly intergenerational report.

“It would be so valuable to have a proper mechanism in place to review the pension and preservation ages in line with real economic and demographic data, rather than trying to tackle it on an ad-hoc basis,” Knox said.

He told Investment Magazine that, in addition to the four areas for improvement highlighted in the report, another positive feature of the Danish and Dutch systems Australia should try to emulate was its very high “coverage rates”. This is a measure of the proportion of the adult population participating in the superannuation system.

Self-employed Australians not obligated

Self-employed Australians not obligated

The main reason Denmark and The Netherlands have higher coverage rates than Australia is because they capture the self-employed in their mandatory retirement savings schemes.

In Australia it is compulsory for employers to contribute to super on behalf of their employees, but self-employed people are not compelled to contribute to their own super.

“Too many contractors and self-employed Australians are slipping through the net,” Knox said. “Bringing these people into the compulsory super system would be a difficult political exercise, but it may well be one we need to tackle.”

Most self-employed people prefer to invest any excess earnings into growing their business, rather than locking it away in a retirement account.

A trend towards more workers being employed on a casual or contract basis means the government must also reconsider the thresholds that exclude them from compulsory super entitlements, he said.

Another way to improve the adequacy of Australia’s retirement income system, and catch up with Denmark and The Netherlands in the MMGPI rankings, would be to apply the super guarantee to income support payments.

“Whenever someone is on any form of income support – be that disability, parental, or carer’s leave – they should be eligible for super guarantee payments,” Knox said.

Financial System Inquiry chairman David Murray said that in an “ideal world” Australia would go beyond plans to raise the super guarantee to 12 per cent and lift it to 15 per cent, the level he calculates would be required to ensure most workers could save enough for an adequate retirement income.

However he does not expect that to happen any time soon.

“Australia is facing fiscal constraints. The ability of the government to continue throwing more money at the super system is going to be limited.”

Need to get young people interested in super

KPMG demographer and social commentator Bernard Salt said government and the super industry faced a huge challenge to get younger workers engaged with the debate around super and pensions.

“Young people are grappling with more immediate financial issue like trying to buy a home and are not particularly interested in debates about superannuation rules and taxes,” Salt said.

“But they should be. Laying the groundwork now for a fairer and more efficient super and pension system when they retire is in their best interests.”

Industry Super Australia chief executive David Whiteley said the big lesson for Australian policymakers from the 2016 MMGPI findings should be the dominance of countries where unions play a strong role in negotiating workers’ super arrangements.

Both Denmark and The Netherlands have an “industrial model” whereby collective agreements between employers and unions decide what the default funds for workers’ compulsory payments are.

Australia has historically had a similar system, but the government has tasked the Productivity Commission with conducting a review of this with a view to moving to a more “competitive, efficient, and transparent” model.

“If our system made sure people were connected with the best performing funds, then making people work longer would not be necessary,” Whiteley said.

Knox disagreed.

“What matters most in defining a good system is adequacy, and that’s why lifting the super guarantee, extending working years, and improving coverage are such important reforms.”

This article first appeared in the November print edition of Investment Magazine. To subscribe and have the magazine delivered CLICK HERE. To sign-up for our free regular email newsletters CLICK HERE.

Leave a Comment

You must be logged in to post a comment.