New legislation mandating comprehensive income products for retirement is still probably more than a year away but it’s already making waves. Australia’s biggest superannuation funds are grappling with creating this new breed of sophisticated products, and those who get it right first will have the edge.

Looming regulatory change meets business pressure from an ageing population. That’s what superannuation funds are facing as their product innovation skills are put to the test working to develop more sophisticated retirement income accounts.

The government, following the recommendation of the 2014 Financial System Inquiry, plans to require the introduction of comprehensive income products for retirement (CIPRs) as a standard alternative to lump-sum payouts at retirement.

Those funds that succeed at cracking the retirement income challenge will be best placed to thrive over the coming decade, a period when the number of funds able to retain their status as a MySuper provider is tipped to dwindle. MySuper is the licensing regime for the no-frills class of products that are eligible to be nominated in industrial awards and workplace agreements as default superannuation funds.

Historically, regulation of the $474 billion default super sector has focused almost exclusively on the accumulation phase: how funds manage members’ money and build their balances during people’s working lives. Now, as the baby boomer generation is retiring and 25 years after the introduction of the superannuation guarantee, there is an intensifying focus on the obligations incumbent on default funds to help members manage the drawdown of their accumulated savings.

In December 2016, Minister for Financial Services Kelly O’Dwyer launched a major discussion paper, titled Development for the framework of comprehensive income products for retirement (CIPRs), outlining the government’s plans and seeking feedback from the industry. The consultation closes on April 28, 2017.

Two of the key areas of regulatory uncertainty that funds complain are holding up their ability to develop their own CIPRs are the question of what safe harbours will be in place to protect trustees from legal action, and debate over the role of income guarantees.

Meanwhile, funds are also facing the challenge of creating CIPRs that are simple enough for members to understand. Yet another obstacle is member concerns about pooled arrangements, and the resulting loss of balances at death.

“At the end of the day, there are product providers willing to manufacture CIPRs, or component products that can be used to build a CIPR,” says Willis Towers Watson head of retirement solutions, Nick Callil. “But ultimately, it will have to be the super funds that put them all together. Funds themselves have got to be able to implement whatever is decided is a CIPR.”

The introduction of CIPRs was a recommendation of the 2014 Financial System Inquiry, led by David Murray. Boosting average retirement incomes to improve living standards for the ageing population is the goal. The report states that incomes from CIPRs could be up to 15 per cent to 30 per cent higher than those from the current popular strategy of drawing the minimum amount from account-based pensions.

In the recently released discussion paper, the government suggests rebadging the clumsy acronym CIPR as the more consumer friendly MyRetirement, reflecting the relationship to the MySuper licensing regime.

Guaranteed income puzzle

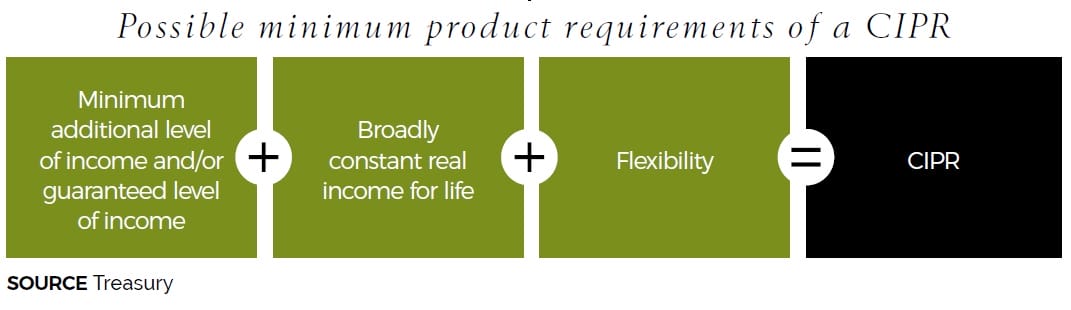

The government’s discussion paper is consistent with Murray’s vision that a CIPR provide flexibility, manage longevity risk through a stream of broadly constant real income for life, and provide a minimum level of additional income and/or guaranteed income.

This requirement for CIPRs to provide a certain level of guaranteed income is expected to be one of the most contentious issues in developing legislation to govern the development of these new products. The discussion paper states that to enable CIPRs to deliver on the goal of better outcomes than the status quo, a minimum income efficiency could be prescribed.

Callil says promising a guaranteed income presents two key challenges. The first is establishing the value for retirees.

“Members need to be convinced that the price of certainty – as represented by the difference between a guaranteed income and what they can expect to receive (though not with certainty) from a market-based product, like an account-based pension – is worth the additional cost,” he says.

The second is implementation.

Unlike banks, super funds generally do not have a balance sheet, hence any guarantee or promise must be implemented via a third party. “This represents a step up from the simple product design most funds are used to,” Callil says.

Many funds will need more sophisticated governance to understand the inherent risk and establish the necessary oversights to implement these more complex products.

Challenger Life chief executive Richard Howes says the devil will be in the legislative detail.

“It does depend on how much of the income is guaranteed and it can be difficult to be absolute on what minimum income should be,” Howes says. “The levels of income that a CIPR would be able to achieve would be a function of market variables, such as prevailing interest rates and prospective returns from asset classes.”

Challenger is the country’s biggest annuity maker and is at the forefront of developing products that the super funds will use in producing CIPRs. The ASX-listed company’s share price has added about 35 per cent since the government announced plans in the May 2016 federal budget to legislate a CIPR framework and remove impediments to the development of other innovative pooled-risk and longevity products, such as deferred annuities.

Calls for a safe harbour

Another issue that could present a major sticking point is exactly what legal protection funds would have if they direct members into a CIPR that underperforms.

The discussion paper raises the possibility of a legal safe harbour.

“Without [legal protection], issuing a CIPR could potentially put super fund trustees at risk,” Callil says. “If they’re exposed to action from retirees, trustees could shy away from offering CIPRs in the first place, which would affect the success of the whole initiative.”

The issue is that nudging retirees towards a product could be seen as some sort of endorsement from the fund, Callil notes, adding that there is a chance trustees will shy away from longevity guarantees because, for some members, they may not make much sense.

It is indicated in the discussion paper that a safe harbour is likely to be provided, but that this would not provide a defence or carve-out from financial advice law.

Australian Catholic and UniSuper at the forefront

Callil says developing CIPR-style products is a “business issue forward-thinking funds need to address, whether or not the government is prodding them in that direction”.

Few smaller funds have started developing CIPR-like products. One notable exception is Australian Catholic Superannuation and Retirement Fund, a $7.5 billion faith-based fund that was one of the earliest out of the blocks, launching its RetireSmart product in October 2015.

While all of the major funds are already devoting resources to coming up with their own CIPR designs, most are keeping hush-hush about their plans until the legislation is announced.

UniSuper, the $55 billion default fund for university staff, has positioned itself as a market leader by announcing it is in the advanced stages of developing a CIPR-style product, despite the regulatory uncertainty.

Its new default retirement income product, FlexiChoice is due to launch in the 2017-18 financial year

The product, which has been under development for three years, spans both accumulation and retirement phases. At retirement, its default benefit, a lifetime income stream, can be combined with an account-based pension component to achieve the CIPR objectives of efficient longevity protection and flexibility to access a lump sum.

UniSuper head of product Ian Lorimer says FlexiChoice was developed within the existing law, but he is confident it will fit comfortably into any new framework required for CIPRs.

“Our FlexiChoice product will have exposure to growth assets, which [means it will meet such objectives more easily than traditional lifetime income products], which typically have a greater exposure to fixed interest securities,” Lorimer explains.

Sunsuper and QSuper also on the move

Sunsuper is another fund already developing its own CIPR solution. Shane Mather, who is head of product for the $30 billion Queensland-based industry fund, says the process has been filled with challenges.

“Absolutely it’s a challenge [creating a CIPRs-style product],” Mather says. “We’re not going to run away from that at all. But we will overcome it. We have got a good record to date.”

The first phase of development has involved member testing. Mather says feedback has indicated that what members want is compatible with what the recent discussion paper proposes.

“They want a product that offers everything: longevity, good investment returns and flexibility,” he says. “That’s the aim of the MyRetirement offer, those three things. Our members did support that.”

Sunsuper is about to move on to the next phase: taking a prototype product for members to get feedback on crucial things such as what modelling and pricing will look like. Mather says it’s too early to provide details.

The biggest obstacle, he says, is creating a simple product that members can understand. “I don’t think anyone has done a good job in this space,” he says. “They’re too complicated. They’re so complicated that not even the advisers understand them.”

An even bigger challenge will be educating members. Funds will battle members’ mindsets on paying into risk-pooling arrangements and the fact that if they die they forfeit the balance and the kids’ inheritance will be lost. Mather says there is an attitude among members that they shouldn’t be forfeiting money.

More funds to follow

QSuper, the $65 billion default fund for Queensland public servants, is also moving out in front of the CIPR legislation by developing a new smart default option for retired members who select an income account allocated pension.

“At the moment, pension members who select an income account are asked to select their preferred investment strategy option,” QSuper chief executive Michael Pennisi says.

“They will still be able to [do this], but the new default will be a mix of cash (set aside to make regular payments) with the rest invested in a balanced investment strategy.

“We thought it was the right move to put a default investment strategy in place for the retirement income account. Many of our retiring members get financial advice through QInvest, but [quite a few] just want us, as a trustee, to make it as simple as possible for them with an appropriate default.”

Willis Towers Watson’s Callil tips that even though it is likely to be another year at least before CIPR legislation is finalised and passed, more funds will make announcements about new retirement income accounts in the coming months. The leadership by early adopters is giving them too much of a competitive advantage for others not to follow.

This article first appeared in the March print edition of Investment Magazine. To subscribe and have the magazine delivered CLICK HERE. To sign-up for our free regular email newsletters CLICK HERE.

Leave a Comment

You must be logged in to post a comment.