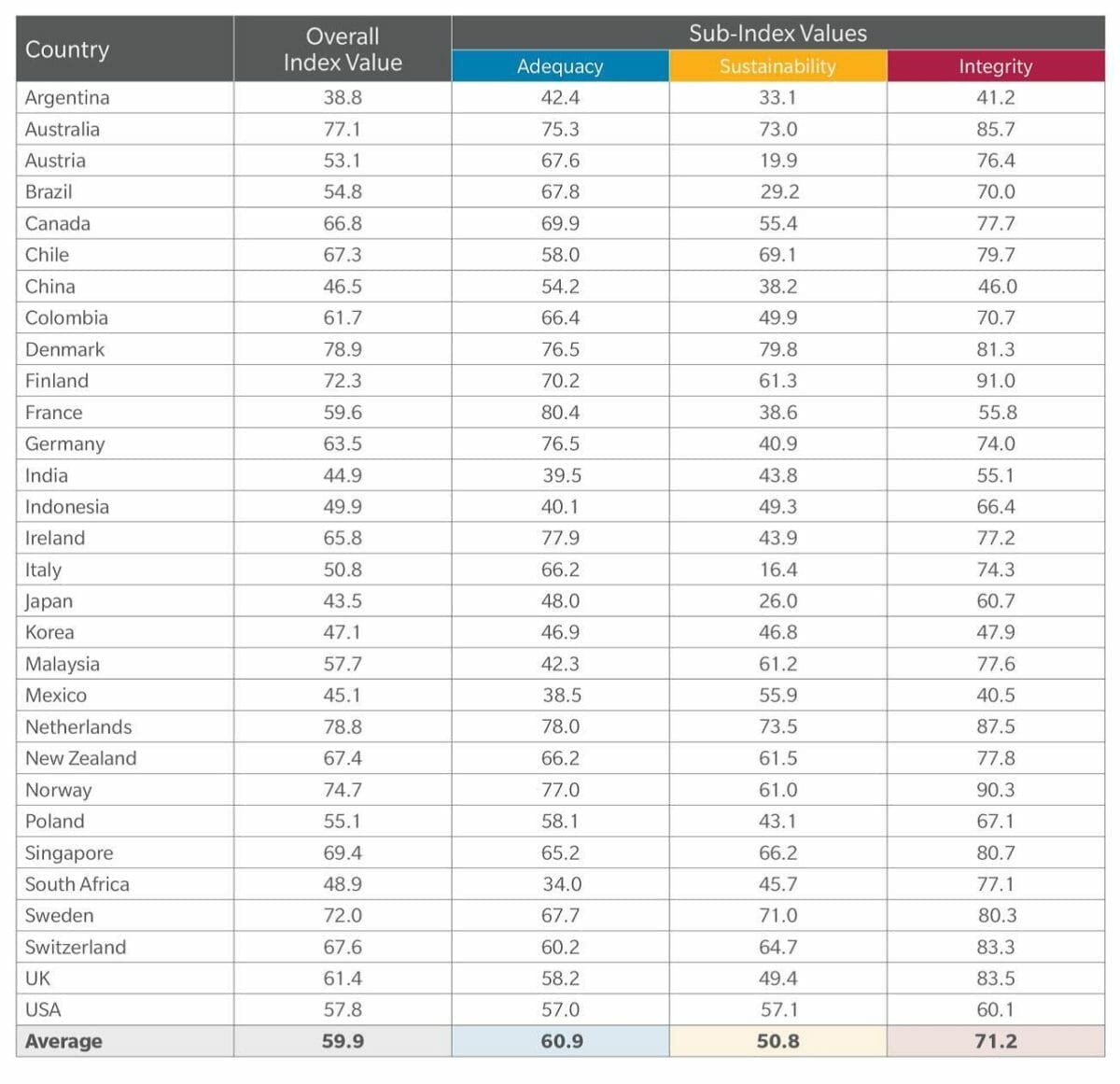

Australia’s retirement income system has retained its mantle as the world’s third best, but its sustainability is slipping in tandem with falling household savings, a respected global study has found.

Denmark claimed the top spot for the sixth consecutive year in the ninth-annual Melbourne Mercer Global Pension Index (MMGPI), released on Monday, October 23, 2017. The Netherlands ranked in second place, followed by Australia.

The index is based on research to assess the pension systems of 30 countries, collectively representing 60 per cent of the world’s population. It considers both public and private pension systems. In 2017, New Zealand, Colombia and Norway were included in the index for the first time.

Another change this year was the addition of a new economic growth question to judge a system’s sustainability, which resulted in Denmark and the Netherlands both losing their A-rating for the first time, dropping to a B+, in line with Australia.

The MMGPI is produced annually by international consulting firm Mercer in partnership with The Australian Centre for Financial Studies, which is based at Monash University.

Growth rates key

In 2017, Australia’s overall index value fell from 77.9 to 77.1, down from its peak score, in 2014, of 79.9.

Australia’s slip in the index was blamed on a reduction in the household savings rate and slower economic growth as the economy becomes more advanced and the population ages, the authors said.

“Household savings is outside the retirement saving system but we look at it because it’s part of the savings structure,” Mercer senior actuary David Knox said.

Countries with high real economic growth over the last three years, such as China, India, Indonesia, Ireland and Malaysia, all had increased index values as a result of economic growth information being included for the first time.

| MMGPI Historical Performance – Australia | ||||||||

| 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| 74.0 | 72.9 | 75.0 | 75.7 | 77.8 | 79.9 | 79.6 | 77.9 | 77.1 |

Higher-ranking countries with large pension assets and high mandatory contributions but lower real economic growth, such as Canada, Denmark and the Netherlands, suffered a drop in the index.

“Denmark and the Netherlands have very significant savings assets of about 170 per cent of GDP (gross domestic product) compared with Australia’s 130 per cent,’’ Knox said. “They’re still the best systems in the world but we just have to recognise that economic growth, particularly with an ageing population, is going to put pressures on government finances and government debt.”

Room for improvement

Australian Centre for Financial Studies interim director professor Edward Buckingham said there was room for improvement in Australia’s system.

“Without the immigration of young people from other countries, our ageing, locally born population would face significant challenges funding their retirement,” Buckingham said.

“The reason is, simply, as we live longer, healthcare and public service costs will escalate and our society, like others, will face pressure to fund the needs of the old at the expense of the young.”

Buckingham said all countries needed to remain alert to the implications of demographic and economic trends for the long-term sustainability of their pension systems.

“Optimising the use of savings set aside for retirement is a perennial responsibility that demands strategic improvement of pension systems worldwide,” he said.

Australia’s retirement income system could be improved by increasing the labour force participation rate at older ages, lifting the pension age and closing the gap between the minimum preservation age and pension eligibility, the report found.

Introducing a requirement that part of the retirement benefit be taken as an income stream would also strengthen the system.

“The preservation age should also be increased to no more than five years less than the pension age,” Knox said.

While government will defer the age for pension eligibility to 67 by 2023, there are no plans to defer the preservation age cap of 60 for people born after July 1, 1964. Knox warned the wider gap between the two would result in some people spending all their super savings in the interim before moving to the pension.

Incentives for self-employed

Encouraging more self-employed workers to contribute to their superannuation savings was also an important step to sustainability, he said.

“About 68 per cent of Australians of working age have some super but there are others, like the self-employed or gig workers, who aren’t covered and don’t need to be covered,” Knox said.

He suggested self-employed people could be encouraged to contribute to their super once their annual income rises above $50,000.

“Traditionally, government has been reluctant to impose this on the self-employed because they want to put money back into their business, but you’re not going to sell the local plumbing business for much,” Knox said. “We would certainly advise that these Australians should be increasing their contributions.”

Melbourne Mercer Global Pension Index – Overall results

Leave a Comment

You must be logged in to post a comment.