OPINION | The global financial crisis (GFC) of 2007-08 fundamentally re-shaped the contours of the worldwide financial services landscape. It was a time of fear and recalibration, when investors and super fund members reset their expectations and understanding of investment markets. For super funds, what became integral was a holistic view of how members would respond to monumental market shocks and the role funds should play in giving both comfort and reassurance to members by helping them plan for the long term.

It’s important to remember superannuation is a long-term investment and members need to regard it as such. The perennial problem for funds is that their members often find themselves in one of two categories: the engaged and the ‘set and forget’ cohort. For those who are engaged, it can be difficult to keep an eye on the long term. It’s easy for members to forget occasional negative years in investment returns are accounted for in the usual performance objectives of balanced investment options, with funds typically aiming for no more than one negative year in every five.

The key lesson for us from the GFC is that human behaviour does not always change in response to shocks or upheavals and a short-term perspective on investments is hard to shift. Being wary of bumps and shocks is only human, but super funds need to be able to respond appropriately to ensure our members are heading in the right direction and can avoid any adverse consequences arising from rash decisions. We must realise that we have a role to play in educating these same members so they can ride out any volatility without panicking.

High performers

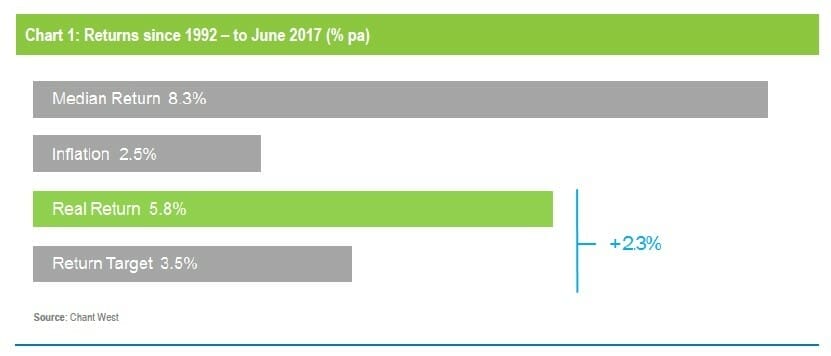

Volatility is not just normal, it is expected. At REI Super, we plan for it accordingly in the asset allocation and design of our investment options. Despite the onset of the GFC, the performance figures of industry funds over the last few years speak for themselves. In fact, data released by Chant West last month found that the investments of super funds between 1992 and 2017 generated 5.8 per cent above the rate of inflation in real returns, which is the annual percentage return realised on investment and adjusted for inflation. This was a boost to the retirement savings of their members (See Chart 1).

REI Super’s balanced MySuper and default option is a growth-oriented diversified investment that has a 20 per cent allocation to Australian shares and a 33 per cent allocation to international shares, and aims to exceed inflation by at least 3 per cent a year over rolling 10-year periods. It is designed for members who want higher potential returns and who are willing to accept a reasonably high level of fluctuations in returns. Chart 1 also shows the median return on a balanced fund like this easily surpassed the return target of exceeding inflation by at least 3 per cent a year, over an extended period that included a crippling event such as the GFC.

Reassurance for members

At REI Super, we are continuing to remind members of the messages we reassured them with 10 years ago. Our superior long-term investment performance highlights the benefits of maintaining a long-term view, combined with expert management and low fees. Last year, SuperRatings found REI Super was one of just eight funds that has doubled their members’ money in the 10 years since the GFC. This is why we can speak with conviction when we encourage our members not to crystallise short-term losses when markets are volatile, but to stay the course instead, and remember to keep sight of the long-term investment strategy.

In the aftermath of the GFC, looking back, our response was almost entirely focused on providing information and reassurance to members. Our approach to managing investments did not change significantly, although we made further refinements to our downside risk protection signals. We did then, and still do, manage the portfolio dynamically. In fact, each REI Super investment option invests in a combination of asset classes with each option maintaining different performance objectives, risks and investment timeframes, so members can choose what’s right for them. Unlike retail or bank-owned superannuation funds, all our profits are reinvested, to build on the growth we’ve made in our members’ super.

In this environment, it’s important for funds to remain cautious and protect our portfolios from market shocks where we can. But financial literacy is equally important, both in terms of raising the confidence of super fund members and providing the impetus for industry funds to realise their role as advocates for change, empowering members to become more engaged with their retirement savings.

Keeping our members informed and up to date is at the heart of everything we do. Our quarterly newsletter, regular promotional campaigns and social media outreach are all part of a concerted effort to build member awareness. We think this is a role all industry super funds must take when it comes to maintaining a regular touchpoint with their members and having an open dialogue about how volatility is normal.

Super funds must be focused on helping educate members about the long-term nature of their superannuation, so that when there is a downturn, these same members don’t react overly emotionally and put their retirement futures at risk.

Mal Smith is the chief executive of Australian real-estate industry fund REI Super.

Leave a Comment

You must be logged in to post a comment.