Asset owners with a net zero goal in mind should not be so quick to dismiss investing in high-emitting companies, said Robeco’s director of sustainable index solutions, Frank Wirds, as he highlighted that these companies are a “part of the solution, not only the problem”.

During a keynote speech at Investment Magazine’s Fiduciary Investors Symposium this month, Wirds, who has been with the $297 billion international asset manager for 17 years, said while companies’ carbon emission data is important, it “doesn’t tell the full story” for climate-conscious investors.

“A lot of the green innovation needs to come from companies that are now in sectors that need to transition and have the innovation to do that, like material, energy and utility sectors,” he told the conference in Healesville, Victoria.

Citing Goodhart’s Law – an adage stating that “when a measure becomes a target, it ceases to be a good measure” – Wirds said carbon emissions data obeys the same principle. If an investor sets out to reduce a certain percentage of carbon footprint in their climate strategy or in a low-carbon index, they might be unintentionally allocating capital away from companies that are essential for achieving that goal.

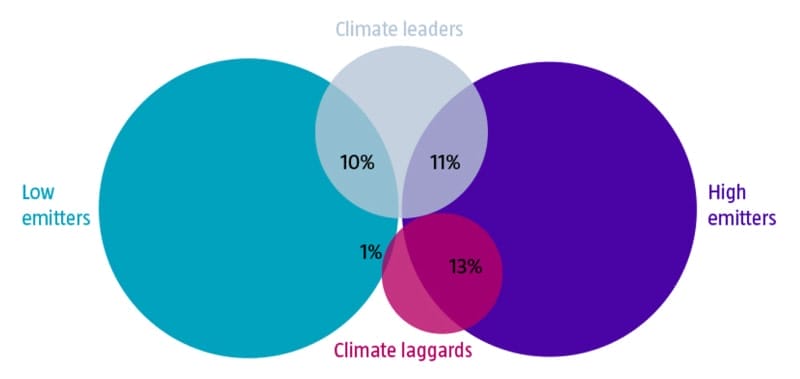

This is backed by Robeco’s research last year using the asset manager’s own UN Sustainable Development Goals (SDGs) framework, which identified the “climate leaders” and “laggards” in 73 per cent of the stocks covered in the MSCI World Investable Market Index. The research found that while 13 per cent of the climate laggards are, unsurprisingly, high emitters, 11 per cent of the climate leaders also fall into that group.

“If you follow a, let’s say, more generic approach for a climate strategy or a low-carbon index, you might actually exclude underweight companies that are going to contribute to a low-carbon economy,” Wirds said.

“So what we say is that you need to have more of a granular analysis, instead of just focusing on an X per cent of carbon footprint reduction, because you are going to miss out on climate leaders [in that process] as well.”

Wirds also encouraged institutional investors to approach ESG ratings with an extra layer of consideration, because the metrics may not effectively capture a company’s impact on society.

In other Robeco research, the company gathered the investment exclusion lists published by large institutional investors around the globe and evaluated the criteria against 293 firms in the MSCI ACWI Investable Market Index. It found that more than half of tobacco producers, one of the most commonly excluded sectors, are considered as having an average ESG rating by MSCI and Sustainalytics standards, with some even considered as ESG leaders.

“A lot of members are becoming more and more vocal about the type of investments in their retirement strategy they’d like to be associated with, or not – at least in Europe and in particular…with Dutch pension funds,” Wirds said.

“Of all the trillions and trillions of sustainable assets out there, 70 per cent is classified like that because it has ESG integration.

“Many, many investors in sustainable investment strategies or sustainable indices are investing based on an ESG metric, whereas this can clearly lead to positions in companies that might not really align with what you, or your investor clients, or the members of your super funds perceived to be sustainable.”

Leave a Comment

You must be logged in to post a comment.